Regions Bank 2011 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

REGIONS 2011 ANNUAL REPORT4

Each of these priorities includes a plan to mea-

sure performance – this is an integral part of our

corporate culture and key to our future growth.

We believe teams perform best when all players

understand their roles and have accountabil-

ity for what they accomplish both individually

and collectively.

Strengthen Financial Performance

Our 2011 results refl ected our priority of strength-

ening fi nancial performance. Adjusted pre-tax

pre-provision income2, or PPI, totaled $1.9 bil-

lion, excluding securities transactions, leveraged

lease terminations, branch consolidation costs

and other property charges and goodwill impair-

ment. This is an increase of 11% compared to

the prior year. Our associates delivered these

results and many more during a year where

headwinds challenged the way we operate and

the banking environment continued to evolve.

Strong Low Cost Deposit Growth. Our strategy

to lower deposit costs while remaining competi-

tive and improve funding mix produced solid

results for the year, as deposit costs declined

29 basis points relative to our peers, which on

average declined only 21 basis points. Average

low cost deposits grew 6% for the year, refl ect-

ing our ability to signifi cantly re-price maturing

certifi cates of deposits. As a result, funding

costs were further reduced by a favorable shift

in our deposit mix. Given the signifi cant amount

of certifi cates of deposit maturing in 2012,

we see additional opportunities next year.

We were pleased to see our deposit strategy was

validated by the FDIC’s annual market share

report, which showed that even as we reduced

interest rates on deposits, Regions maintained

a No. 1 market share position in Alabama, Ten-

nessee and Mississippi and also maintained a

position of fourth or better in Florida, Arkansas

and Louisiana.

Improved Credit Quality. Our provision for credit

losses was 47% lower in 2011 than 2010, and

we saw continued improvement in our credit

quality trends. Although our non-performing

assets remain high at $3 billion, they did de-

cline 24% in 2011. Other credit metrics also

showed improvement during the year as our

business services criticized loans, which are

our earliest indicators of problem loans, de-

clined 35%, early and late stage delinquen-

cies declined 24%, and net loan charge-offs

decreased 29%. Furthermore, our allowance

for loan losses remains strong at $2.7 billion, or

3.54% of total loans. While our improvement in

credit quality will generally track the economic

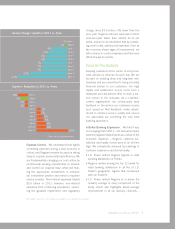

Low Cost Deposits / Deposit Costs*

67,125 71,813 76,244

2008 2009 2010 2011

1.91%

1.35%

0.78%

0.49%

58,425

*From continuing operations

Focus on

the Customer

Manage Performance

Build the

Best Team

Strengthen

Financial

Performance

Enhance

Risk

Management

2 Non-GAAP, see Form 8-K Exhibit 99.2 page 10 for GAAP to non-GAAP reconciliation