Regions Bank 2011 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

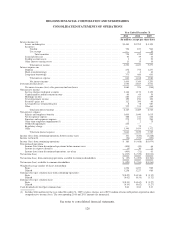

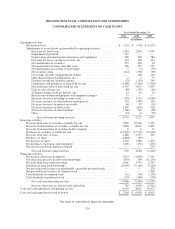

Non-interest expense from continuing operations in 2010 included a $75 million regulatory charge.

Non-interest expense, excluding the regulatory charge (non-GAAP), decreased $1 million to $3.8 billion in 2010.

See Table 6 “Non-Interest Expense from Continuing Operations (including Non-GAAP reconciliation)” and the

text preceding Table 2 “GAAP to Non-GAAP Reconciliation”. Salaries and employee benefits remained

relatively stable at $1.6 billion in 2010. At December 31, 2010, Regions had 27,829 employees compared to

28,509 at December 31, 2009.

Net occupancy expense decreased 3 percent to $411 million in 2010, due primarily to charges associated

with the 2009 decision to consolidate 121 branches. Furniture and equipment expense decreased $4 million to

$277 million in 2010. This decrease was primarily due to branch consolidation charges of $7 million incurred in

2009.

Professional and legal fees are comprised of amounts related to legal, consulting and other professional fees.

These fees increased $3 million to $170 million in 2010, reflecting an increase in the level of credit-related legal

expenses in 2010.

OREO expenses include the cost of adjusting foreclosed properties to fair value after these assets have been

classified as OREO and net gains and losses on sales of properties, as well as other costs to maintain the property

such as property taxes, security and grounds maintenance. Through Regions’ efforts to sell foreclosed properties,

OREO balances decreased $153 million to $454 million in 2010 compared to $607 million in 2009. OREO

expense increased $34 million to $209 million in 2010 compared to $175 million in 2009, primarily driven by

valuation declines resulting from further deterioration of the housing and real estate markets.

FDIC premiums decreased $7 million to $220 million in 2010. The decrease resulted from a $64 million

special assessment in 2009. The FDIC made a number of changes to its assessment rate schedule, which drove an

offsetting increase in premium rates. The bank regulatory agencies’ ratings, comprised of Regions Bank’s

capital, asset quality, management, earnings, liquidity and sensitivity to risk, along with its long-term debt issuer

ratings and financial ratios, were the primary factors in determining FDIC insurance premiums.

Other miscellaneous expenses include communications, postage, supplies, credit-related costs and business

development services. Other miscellaneous expenses decreased $43 million to $640 million in 2010.

The Company’s income tax benefit for 2010 was $376 million compared to a tax benefit of $194 million in

2009, resulting in an effective tax rate of 44.5 percent and 15.3 percent, respectively. The increase in income tax

benefit reflects the impact of the decline in the number and amount of leveraged lease terminations offset by the

recognition of the regulatory charge and the decrease in the consolidated pre-tax loss.

Net charge-offs totaled $2.8 billion, or 3.22 percent of average loans in 2010 compared to $2.3 billion, or

2.38 percent of average loans in 2009. The increased loss rate reflected seasoning of losses as the Company

moved through the credit cycle as well as the impact of asset dispositions which increased charge-offs and

decreased average loan balances. Charge-off ratios were higher across most major classes, with investor real

estate experiencing the largest increase. Non-performing assets decreased from $4.4 billion at December 31,

2009 to $3.9 billion at December 31, 2010, reflecting management’s efforts to work through problem assets and

reduce the riskiest exposures.

The provision for loan losses is used to maintain the allowance for loan losses at a level that in

management’s judgment is appropriate to cover losses inherent in the portfolio at the balance sheet date. During

2010 the provision for loan losses was $2.9 billion. This compares to a provision for loan losses of $3.5 billion in

2009.

120