Regions Bank 2011 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

unpaid at the conversion date were settled through issuance of common shares in accordance with the original

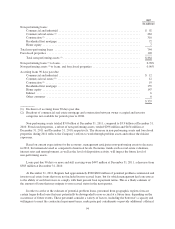

document. Approximately 63 million common shares were issued in 2010 in the conversion and dividend

settlement. No Series B shares were outstanding at December 31, 2011 or 2010.

In addition to the offerings mentioned above, in 2009 the Company also issued approximately 33 million

common shares in exchange for $202 million of outstanding 6.625 percent trust preferred securities issued by

Regions Financing Trust II (“the Trust”). The trust preferred securities were exchanged for junior subordinated

notes issued by the Company to the Trust. The Company recognized a pre-tax gain of approximately $61 million

on the extinguishment of the junior subordinated notes. The increase in shareholders’ equity related to the debt

for common share exchange was approximately $135 million, net of issuance costs.

These public offerings along with other capital raising efforts resulted in Regions fully meeting the Tier 1

common equity capital requirement and exceeding the Tier 1 capital requirements prescribed by the SCAP (see

Table 2 “GAAP to Non-GAAP Reconciliation” for further discussion).

At December 31, 2011, Regions had 23 million common shares available for repurchase through open

market transactions under an existing share repurchase authorization. There were no treasury stock purchases

through open market transactions during 2011 or 2010. The Company’s ability to repurchase its common stock is

limited by the terms of the Purchase Agreement between Regions and the U.S. Treasury entered into on

November 14, 2008, pursuant to the U.S. Treasury’s Capital Purchase Program (“CPP”). See Part II, Item 5

(“Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity

Securities”) for more information.

Regions’ ratio of stockholders’ equity to total assets was 12.99 percent at December 31, 2011 and 12.64

percent December 31, 2010. Regions’ ratio of tangible common stockholders’ equity (stockholders’ equity less

preferred stock, goodwill and other identifiable intangibles and the related deferred tax liability) to total tangible

assets was 6.58 percent at December 31, 2011 compared to 6.04 percent at December 31, 2010 (see Table 2

“GAAP to Non-GAAP Reconciliation” for further discussion). The increase between years was a result of the

change in accumulated other comprehensive income and the reduction in tangible assets.

In 2011 and 2010, Regions’ annual dividend was $0.04 per common share compared to $0.13 in 2009.

Regions does not expect to increase its quarterly dividend above $0.01 per common share for the foreseeable

future.

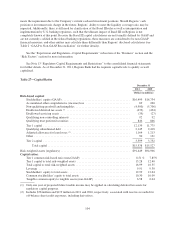

BANK REGULATORY CAPITAL REQUIREMENTS

Regions and Regions Bank are required to comply with regulatory capital requirements established by

Federal and State banking agencies. These regulatory capital requirements involve quantitative measures of the

Company’s assets, liabilities and certain off-balance sheet items, and also qualitative judgments by the

regulators. Failure to meet minimum capital requirements can subject the Company to a series of increasingly

restrictive regulatory actions. Currently, there are two basic measures of capital adequacy: a risk-based measure

and a leverage measure.

The risk-based capital requirements are designed to make regulatory capital requirements more sensitive to

differences in credit and market risk profiles among banks and bank holding companies, to account for

off-balance sheet exposure and interest rate risk, and to minimize disincentives for holding liquid assets. Assets

and off-balance sheet items are assigned to broad risk categories, each with specified risk-weighting factors. The

resulting capital ratios represent capital as a percentage of total risk-weighted assets, inclusive of off-balance

sheet items. Banking organizations that are considered to have excessive interest rate risk exposure are required

to maintain higher levels of capital.

102