Regions Bank 2011 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

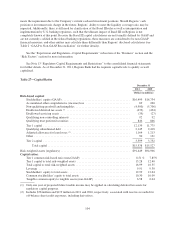

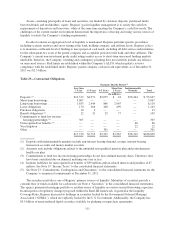

The minimum standard for the ratio of total capital to risk-weighted assets is 8 percent. At least 50 percent

of that capital level must consist of common equity, undivided profits and non-cumulative perpetual preferred

stock, senior perpetual preferred stock issued to the U.S. Treasury under the Capital Purchase Program, minority

interests relating to qualifying common or noncumulative perpetual preferred stock issued by a consolidated U.S.

depository institution or foreign bank subsidiary, less goodwill, disallowed deferred tax assets and certain other

intangibles (“Tier 1 capital”). The remainder (“Tier 2 capital”) may consist of a limited amount of other preferred

stock, mandatorily convertible securities, subordinated debt, and a limited amount of the allowance for loan

losses. The sum of Tier 1 capital and Tier 2 capital is “total risk-based capital” or total capital. However, under

the Collins Amendment, which was passed as a section of the Dodd-Frank Act, trust preferred securities will be

eliminated as an element of Tier 1 capital. This disallowance of trust preferred securities will be phased in from

January 1, 2013 to January 1, 2016. Debt or equity instruments issued to the Federal government as part of the

CPP are exempt from the Collins Amendment. As of December 31, 2011, Regions had $846 million of trust

preferred securities that are subject to the Collins Amendment and $3.5 billion of preferred equity that is exempt

from the Collins Amendment.

The banking regulatory agencies also have adopted regulations that supplement the risk-based guidelines to

include a minimum ratio of 3 percent of Tier 1 capital to average assets less goodwill and disallowed deferred tax

assets (the “Leverage ratio”). Depending upon the risk profile of the institution and other factors, the regulatory

agencies may require a Leverage ratio of 1 percent to 2 percent above the minimum 3 percent level.

In recent years, the Federal Reserve and banking regulators began supplementing their assessment of the

capital adequacy of a bank based on a variation of Tier 1 capital, known as Tier 1 common equity. This measure

has been a key component of assessments of capital adequacy under the Comprehensive Capital Analysis and

Review (“CCAR”) process. While not currently codified 1, analysts and banking regulators have assessed

Regions’ capital adequacy using the Tier 1 common and/or the tangible common stockholders’ equity measure.

Because tangible common stockholders’ equity and Tier 1 common equity are not formally defined by GAAP or

codified in the federal banking regulations, these measures are considered to be non-GAAP financial measures

and other entities may calculate them differently than Regions’ disclosed calculations (see Table 2 “GAAP to

Non-GAAP Reconciliation” for further details).

The Dodd-Frank Act requires the Federal Reserve to impose more stringent capital requirements on bank

holding companies with assets of $50 billion or more. Consequently, as part of Regions’ annual CCAR, Regions

must submit its annual capital plans to the Federal Reserve. As part of the CCAR, Regions is required to submit

four scenarios including the company’s baseline forecast, the Federal Reserve’s baseline outlook, the Company’s

stress case and the Federal Reserve’s stress case. Regions is required to maintain its capital levels above each

minimum regulatory capital ratio and above a Tier 1 common ratio of 5 percent on a pro forma basis under

expected and stressful conditions throughout a certain time period horizon. Any capital actions requested by

Regions must be submitted to the Federal Reserve for approval. The Federal Reserve has committed to

responding to Regions capital plans by mid-March 2012. The Federal Reserve intends to publish the results of

the supervisory stress test component of CCAR for Regions and all companies that are participating.

Regions is evaluating the anticipated impact of Basel III based on the proposal by the Basel Committee on

Banking Supervision, which will begin in 2013 and is expected to be fully phased-in on January 1, 2019. The

Company’s estimated Tier 1 capital and Tier 1 common ratios as of December 31, 2011, based on Regions’

current understanding of the guidelines, were approximately 11.39 and 7.70 percent, respectively, which are

above the Basel III minimums of 8.5 percent for Tier 1 capital and 7 percent for Tier 1 common. Based on

Regions’ understanding of the calculation for the liquidity coverage ratio under Basel III, Regions currently

1On December 20, 2011 the Board of Governors of the Federal Reserve released a Notice of Proposed

Rulemaking on enhanced capital standards and early remediation requirements mandated by sections 165

and 166 of the Dodd-Frank Act. If enacted as proposed this would codify the calculation of Tier 1 Common

Capital.

103