RBS 2008 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

100

Business review continued

RBS Group Annual Report and Accounts 2008

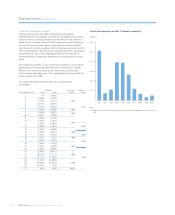

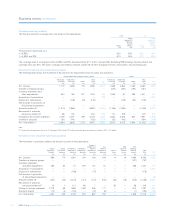

The table below sets out the Group’s loans that are classified as REIL and PPL.

2008 2007

Group Group

before RFS before RFS

Holdings Holdings

minority minority

Group interest Group interest

£m £m £m £m

Non-accrual loans (1) 19,479 17,082 10,362 7,949

Accrual loans past due 90 days (2) 1,782 1,709 369 302

Total REIL 21,261 18,791 10,731 8,251

PPL (3) 226 226 671 131

Total REIL and PPL 21,487 19,017 11,402 8,382

REIL and PPL as % of customer loans and advances – gross (4) 2.52% 2.69% 1.64% 1.49%

The sub-categories of REIL and PPL are calculated as described in notes 1 to 4 below.

Notes:

(1) All loans against which an impairment provision is held are reported in the non-accrual category.

(2) Loans where an impairment event has taken place but no impairment recognised. This category is used for fully collateralised non-revolving credit facilities.

(3) Loans for which an impairment event has occurred but no impairment provision is necessary. This category is used for fully collateralised advances and revolving credit facilities where

identification as 90 days overdue is not feasible.

(4) Gross of provisions and excluding reverse repurchase agreements.

REIL as at 31 December 2008 was £21,261 million (2007 – £10,731

million). Excluding RFS Holdings minority interest, REIL was £18,791

million, an increase of £10,540 million during the year. As a percentage

of customer lending, REIL and PPL in aggregate, excluding RFS

Holdings minority interest was 2.69% of customer loans and advances

at 31 December 2008 (2007 – 1.49%).

Impairment loss provision methodology (audited)

Provisions for impairment losses are assessed under three categories:

•Individually assessed provisions: provisions required for individually

significant impaired assets which are assessed on a case by case

basis, taking into account the financial condition of the counterparty

and any guarantor and collateral held after being stressed for

downside risk. This incorporates an estimate of the discounted value

of any recoveries and realisation of security or collateral. The asset

continues to be assessed on an individual basis until it is repaid in

full, transferred to the performing portfolio or written-off.

•Collectively assessed provisions: provisions on impaired credits

below an agreed threshold which are assessed on a portfolio basis,

to reflect the homogeneous nature of the assets, such as credit cards

or personal loans. The provision is determined from a quantitative

review of the relevant portfolio, taking account of the level of arrears,

security and average loss experience over the recovery period.

•Latent loss provisions: provisions held against the estimated

impairment in the performing portfolio which have yet to be identified

as at the balance sheet date. To assess the latent loss within the

portfolios, the Group has developed methodologies to estimate the

time that an asset can remain impaired within a performing portfolio

before it is identified and reported as such.

Provision analysis (audited)

The Group’s consumer portfolios, which consist of high volume, small

value credits, have highly efficient largely automated processes for

identifying problem credits and very short timescales, typically three

months, before resolution or adoption of various recovery methods.

Corporate portfolios consist of higher value, lower volume credits, which

tend to be structured to meet individual customer requirements.

Provisions are assessed on a case by case basis by experienced

specialists with input from professional valuers and accountants. The

Group operates a clear provisions governance framework which sets

thresholds whereby suitable oversight and challenge is undertaken and

significant cases will be presented to a committee chaired by the Group

Chief Executive or the Group Finance Director.