RBS 2008 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

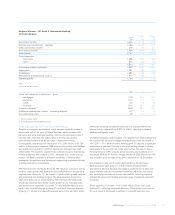

55RBS Group Annual Report and Accounts 2008

Regional Markets – UK Retail & Commercial Banking

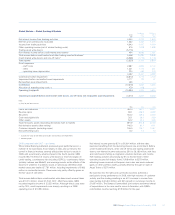

UK Retail Banking

Pro forma Statutory

2008 2007 2007

£m £m £m

Net interest income 4,390 4,172 4,172

Net fees and commissions – banking 2,186 2,351 2,351

Other non-interest income* 218 271 271

Non–interest income 2,404 2,622 2,622

Total income 6,794 6,794 6,794

Direct expenses

– staff costs 1,258 1,266 1,266

– other 574 545 545

1,832 1,811 1,811

Contribution before impairment 4,962 4,983 4,983

Impairment 1,281 1,184 1,184

Contribution 3,681 3,799 3,799

Allocation of manufacturing costs (1) 1,917 1,792 —

Operating profit 1,764 2,007 3,799

Note:

(1) Only for pro forma results.

£bn £bn £bn

Loans and advances to customers – gross

– mortgages 74.9 67.4 67.4

– personal 16.2 17.1 17.1

– cards 6.4 7.8 7.8

– business 20.0 18.7 18.7

Customer deposits** 95.9 96.1 96.1

Investment management assets – excluding deposits 5.7 7.0 7.0

Non-performing loans 4.8 4.3 4.3

* net of insurance claims

** customer deposits exclude bancassurance

2008 compared with 2007 – pro forma and statutory

Despite an economic environment which became markedly weaker in

the second half of the year, UK Retail Banking, which includes both

personal and small business banking, held income and direct costs in

line with 2007. However the deterioration in the macroeconomic

environment resulted in an 8% increase in impairment losses.

Consequently, operating profit decreased 12%, £243 million, to £1,764

million. In the personal segment, RBS retained top position and NatWest

was again joint second for customer satisfaction amongst main high

street banks. The business segment has continued to grow, maintaining

market leadership with a share of 26%, alongside 23% of the start-up

market. UK Retail continues to maintain availability of lending while

managing risk exposure and focusing on supporting customers through

a difficult economic environment.

Net interest income increased 5% to £4,390 million as a result of strong

balance sheet growth. Net interest income performance in the personal

segment was strong, up 7%, as a result of good volume growth coupled

with improving new lending margins. The small business sector has

seen more pressure on asset margins, from increased funding costs,

which has restricted net interest income growth to 4%. Average loans

and advances to customers increased 7% and average deposits were

up 6% with personal savings growing 9% and small business deposits

growing 3%. At year end deposit balances were in line with 2007 levels,

reflecting increasing competitive pressure in a slowing market. Net

interest margin reduced from 3.92% to 3.85%, reflecting increased

funding and liquidity costs.

UK Retail mortgage balances grew 11% despite more muted demand in

the second half, and net mortgage lending market share increased to

19% (2007 – 2%). Small business lending grew 7% despite a significant

contraction in demand. Personal unsecured lending slowed, however,

particularly in the second half of the year. Further, the sale of Tesco

Personal Finance (TPF) reduced personal unsecured balances at 31

December 2008 by £1.9 billion, though income of £285 million from TPF

was included up to the date of the sale completion on 19 December.

Non-interest income net of claims declined 8% to £2,404 million.

Bancassurance sales grew 3% to £353 million annual premium

equivalent in the year however the negative performance of debt and

equity markets reduced investment income by £48 million. Excluding

this, underlying non-interest income declined 6% reflecting reduced

demand for unsecured lending and lower sales of payment protection

insurance.

Direct expenses increased 1% to £1,832 million. Direct staff costs

reduced 1% reflecting increased efficiency. Other direct costs rose by

5% as a result of increased investment in selected business lines.