RBS 2008 Annual Report Download - page 204

Download and view the complete annual report

Please find page 204 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

203RBS Group Annual Report and Accounts 2008

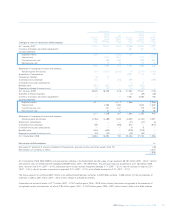

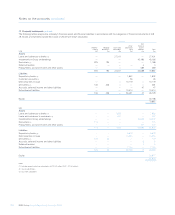

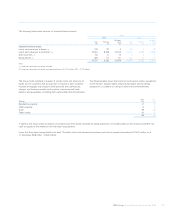

Reasonably possible

alternative assumptions

Carrying Increase Decrease

Valuation basis/ Main amount fair value fair value

Liabilities technique assumptions £bn £m £m

Debt securities in issue Proprietary model Credit spreads 4.4 170 190

Derivatives

Credit derivatives Proprietary CVA model, Counterparty credit risk,

industry option models, correlation model correlation, volatility 2.6 160 180

Other derivatives Proprietary model Volatility, correlation 1.4 120 120

Other portfolios Proprietary model Credit spreads, correlation 0.6 40 60

31 December 2008 9.0 490 550

31 December 2007 15.3 120 120

For each of the portfolio categories shown in the above table, set out

below is a description of the types of products that comprise the portfolio

and the valuation techniques that are applied in determining fair value,

including a description of valuation techniques used, including for those

in level 2, and inputs to those models and techniques. Where reasonably

possible alternative assumptions of unobservable inputs used in models

would change the fair value of the portfolio significantly, the alternative

inputs are indicated along with the impact this would have on the fair value.

Where there have been significant changes to valuation techniques

during the year a discussion of the reasons for this are also included.

Loans and advances to customers

Loans in level 3 primarily comprise US commercial mortgages and

syndicated loans.

Commercial mortgages

These senior and mezzanine commercial mortgages are loans secured

on commercial land and buildings that were originated or acquired by

GBM for securitisation. Senior commercial mortgages carry a variable

interest rate and mezzanine or more junior commercial mortgages may

carry a fixed or variable interest rate. Factors affecting the value of these

loans may include, but are not limited to, loan type, underlying property

type and geographic location, loan interest rate, loan to value ratios,

debt service coverage ratios, prepayment rates, cumulative loan loss

information, yields, investor demand, market volatility since the last

securitisation, and credit enhancement. Where observable market

prices for a particular loan are not available, the fair value will typically

be determined with reference to observable market transactions in other

loans or credit related products including debt securities and credit

derivatives. Assumptions are made about the relationship between the

loan and the available benchmark data. Using reasonably possible

alternative assumptions for credit spreads (taking into account all other

applicable factors) would reduce the fair value of these mortgages

of £1.1 billion by up to £18 million or increase the fair value by up to

£25 million.

Syndicated lending

The Group’s syndicated lending activities are conducted by the

syndicate business in conjunction with the various product lines

covering corporate, leveraged, real estate and project finance activities.

When a commitment to lend is entered into, the Group estimates the

proportion of the loan that is intended to be held for trading on draw

down, and the proportion it anticipates to retain on its balance sheet as

a loan and receivable. Where the commitment is intended to be

syndicated, the commitment to lend is fair valued through profit or loss.

On drawdown, the portion of the loan expected to be syndicated is

recorded at fair value as a held-for-trading asset, and the expected

hold portion is measured at amortised cost less, where appropriate,

impairment.

The Group values the portion of the loan expected to be syndicated

held at fair value by using market observable syndication prices in the

same or similar assets. Where these prices are not available, a

discounted cash flow model is used. The model incorporates

observable assumptions such as current interest rates and yield curves,

the notional and tender amount of the loan, and counterparty credit

quality where it is derived from credit default swap spreads using

market indices. The model also incorporates unobservable assumptions,

including expected refinancing periods, and counterparty credit quality

where it is derived from the Group’s internal risk assessments.

Derivatives arising from commitments to lend are measured using the

same model, based on proxy notional amounts.

Using reasonably possible alternative assumptions for expected cash

flows to value these assets of £2.0 billion would reduce the fair value by

up to £32 million or increase the fair value by up to £45 million. The

assumptions to determine these amounts were based on restructuring

scenarios and expected margins.

Debt securities

Residential mortgage backed securities (RMBS)

RMBS where the underlying assets are US agency-backed mortgages

and there is regular trading are generally classified as level 2 in the fair

value hierarchy. RMBS are also classified as level 2 when regular

trading is not prevalent in the market, but similar executed trades or

third-party data including indices, broker quotes and pricing services

can be used to substantiate the fair value. RMBS are classified as level

3 when trading activity is not available and a model is utilised which

uses significant unobservable data.

In determining whether an instrument is similar to that being valued, the

Group considers a range of factors, principally: the lending standards

of the brokers and underwriters that originated the mortgages, the lead

manager of the security, the issue date of the respective securities, the

underlying asset composition (including origination date, loan to value

ratios, historic loss information and geographic location of the

mortgages), the credit rating of the instrument, and any credit

protection that the instrument may benefit from, such as insurance

wraps or subordinated tranches. Where there are instances of market

observable data for several similar RMBS tranches, the Group considers

the extent of similar characteristics shared with the instrument being

valued, together with the frequency,