RBS 2008 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

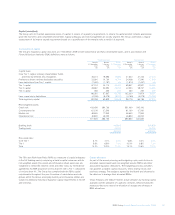

84

Business review continued

RBS Group Annual Report and Accounts 2008

Credit risk

Principles for credit risk management (audited)

The key principles for credit risk management in the Group are as

follows:

•A credit risk assessment of the customer and credit facilities is

undertaken prior to approval of credit exposure. Typically, this

includes both quantitative and qualitative elements including, the

purpose of the credit and sources of repayment; compliance with

affordability tests; repayment history; ability to repay; sensitivity to

economic and market developments; and risk-adjusted return based

on credit risk measures appropriate to the customer and facility type.

•Credit risk authority is specifically granted in writing to individuals

involved in the granting of credit approval, whether this is individually

or collectively as part of a credit committee. In exercising credit

authority, individuals are required to act independently of business

considerations and must declare any conflicts of interest.

•Credit exposures, once approved, are monitored, managed and

reviewed periodically against approved limits. Lower quality

exposures are subject to more frequent analysis and assessment.

•Credit risk management works with business functions on the ongoing

management of the credit portfolio, including decisions on mitigating

actions taken against individual exposures or broader portfolios.

•Customers with emerging credit problems are identified early and

classified accordingly. Remedial actions are implemented promptly

and are intended to restore the customer to a satisfactory status and

minimise any potential loss to the Group.

•Stress testing of portfolios is undertaken to assess the potential credit

impact of non-systemic scenarios and wider macroeconomic events

on the Group’s income and capital.

Specialist credit risk teams oversee the credit process independently,

making credit decisions within their discretion, or recommending

decisions to the appropriate credit committee.

Assessments of corporate borrower and transaction risk are undertaken

using fundamental credit analysis and the application of general

corporate and certain specialist counterparty credit risk models.

Financial markets counterparties are approved by a dedicated credit

function which specialises in traded market product risk. Specialist

credit grading models exist for certain bank and non-bank financial

institutions.

Different approaches are used for the management of wholesale and

retail businesses:

•Wholesale businesses: exposures are aggregated to determine the

appropriate level of credit approval required and to facilitate

consolidated credit risk management. Credit applications for

corporate customers are prepared by relationship managers (RMs) in

the units originating the credit exposures, or by the RM team with

lead responsibility for a counterparty where a customer has

relationships with different divisions and business units across the

Group. This includes the assignment of counterparty credit grades

and LGD estimates using approved models, which are also

independently checked by the credit team.

•Retail businesses: the retail business makes a large volume of small

value credit decisions. Credit decisions will typically involve an

application for a new or additional product or a change in facilities on

an existing product. The majority of these decisions are based upon

automated strategies utilising industry standard credit and behaviour

scoring techniques.