RBS 2008 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

82

Business review continued

RBS Group Annual Report and Accounts 2008

Basel II

The Group adopted Basel II on 1 January 2008. Pillar 1 focuses on the

calculation of minimum capital required to support the credit, market

and operational risks in the business. For credit risk, the majority of the

Group uses the Advanced Internal Ratings Based Approach (AIRB) for

calculating RWAs, making the Group one of a small number of banks

whose risk systems and approaches have reached the regulatory

standards.

For operational risk, the Group uses The Standardised Approach (TSA),

which calculates operational risk-weighted assets based on gross

income. In line with other banks, the Group is considering adopting the

Advanced Measurement Approach (AMA) for all or part of the business.

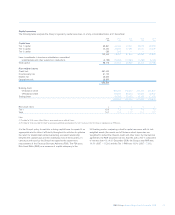

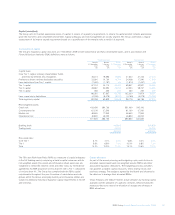

Using these approaches, the RWA requirements, by division, are as follows:

Basel II Basel II Basel I

31 December 1 January 31 December

2008 2008 2007

£bn £bn £bn

Global Markets

– Global Banking & Markets 278.5 211.9 188.7

– Global Transaction Services 19.6 16.8 15.4

Regional Markets

– UK Retail & Commercial Banking 152.5 153.1 179.0

– US Retail & Commercial Banking 78.0 53.8 57.1

– Europe & Middle East Retail & Commercial Banking 30.9 30.3 36.7

– Asia Retail & Commercial Banking 6.4 4.9 3.3

Other 11.9 15.3 9.8

Group before RFS Holdings minority interest 577.8 486.1 490.0

RFS Holdings minority interest 118.0 147.4 119.0

Group 695.8 633.5 609.0

Basel II is cyclical, unlike Basel I where RWAs are stable through the

cycle. Changes in RWA totals are driven by external economic factors

and their impact on the risk profile of the underlying portfolio of assets,

rather than changes in the asset mix. Whilst Basel II tries to reduce this

variation by incorporating measures correlated to downturn conditions,

it remains sensitive to cyclical variations.

The AIRB approach to Basel II is based on the following metrics.

•Probability of default (PD) models estimate the likelihood that a

customer will fail to make full and timely repayment of credit

obligations over a one year time horizon. Customers are assigned an

internal credit grade which corresponds to PD. Every customer credit

grade across all grading scales in the Group can be mapped to a

Group level credit grade.

•Exposure at default (EAD) models estimate the expected level of

utilisation of a credit facility at the time of a borrower’s default.

The EAD may be assumed to be higher than the current utilisation

(e.g. in the case where further drawings may be made on a revolving

credit facility prior to default) but will not typically exceed the total

facility limit.

•Loss given default (LGD) models estimate the economic loss that

may occur in the event of default and represent the debt that cannot

be recovered. The Group’s LGD models take into account the type of

borrower, facility and any risk mitigation such as security or collateral

held.

In addition to minimum capital calculated, for credit, market and

operational risk, banks are required to undertake an Individual Capital

Adequacy Assessment Process (ICAAP) for other risks. The Group’s

ICAAP, in particular, focuses on pension fund, interest rate risk in the

banking book together with stress tests to assess the adequacy of

capital over one year and the economic cycle.

The Group will publish its Pillar 3 (Market disclosures) on the external

website, providing a range of additional information relating to Basel II

and risk and capital management across the Group. The disclosures

focus on Group level capital resources and adequacy, discuss a range

of credit risk approaches and their associated risk weighted assets

(under various Basel II approaches) such as credit risk mitigation,

counterparty credit risk and provisions. Detailed disclosures are also

made on equity, securitisation, operational and market risk, as well as

providing Interest Rate Risk in the Banking Book disclosures.

Stress and scenario testing

Stress testing is central to the Group’s risk and capital framework and

integral to Basel II. Stress testing is used at divisional and Group level to

assess risk concentrations, estimate the impact of earnings on capital,

determine the overall capital adequacy under stress conditions and

identify mitigating actions. The principal business benefits of the stress

testing framework are: understanding the impact of recessionary

scenarios; assessing material risk concentrations; and forecasting the

impact of market stress scenarios on the Group’s balance sheet

liquidity.