RBS 2008 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

92

Business review continued

RBS Group Annual Report and Accounts 2008

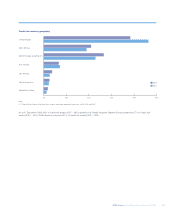

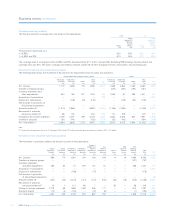

UK residential mortgages

The UK mortgage portfolio totalled £74.4 billion (as at 31 December

2008) an increase of 11% during the year due to strong sales growth

and lower redemption rates. The main brands are the Royal Bank,

NatWest, the One Account, First Active and Direct Line. The assets

comprise prime mortgage lending and include 7.0% (£5.2 billion) of

exposure to residential buy-to-let. There is a very small legacy self-

certification book (0.5% of total assets) which was withdrawn from sale

in 2004.

The Group exited the 100% LTV market in the first quarter of 2008,

further restricted the proportion of highest LTV loans and reviewed

affordability criteria during the year. The average LTV for new business

increased from 62% to 67% in 2008 mainly due to a reduction in the

proportion of business within the lowest LTV bands.

The arrears rate (three or more payments missed) on the combined

Royal Bank and NatWest brands was 1.5% (31 December 2008) up

from 1.0% (31 December 2007). The mortgage impairment charge was

£33 million for 2008 (2007 – £19 million) and in current economic

conditions is expected to increase further. Anticipated losses from

impaired mortgages are covered by a combination of impairment

provisions and post default suspended interest. The combined provision

cover is currently 0.18% of balances.

Repossessions totalled 1,141 in 2008 (compared with 758 in 2007) with

similar volumes in each half of the year.

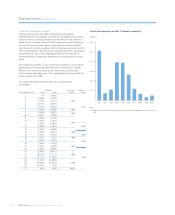

US real estate

Citizens Financial Group’s (CFG) residential real estate portfolio totalled

$50.1 billion at 31 December 2008 (2007 – $53.1 billion) comprising

$13.8 billion of first mortgages and $36.3 billion of Home Equity loans

and lines. This reduction includes the sale of $1.4 billion of real estate

assets to the Federal National Mortgage Association in December 2008.

CFG has historically adopted conservative risk policies in comparison to

the general market. Small exposures to sub-prime (FICO <=620,

approximately 0.6%) and Alt-A / other non-conforming (4.5%) from past

bank acquisitions are in run-off. The average indexed LTV was 69% as at

31 December 2008 (2007 – 62%). Loan acceptance criteria were further

tightened during 2008 to address deteriorating economic conditions.

The Serviced By Others (SBO) portfolio consists of purchased pools of

home equity loans and lines whose LTV and geographic profiles have in

the current economic conditions resulted in a higher write-off rate of

4.8% in 2008 than core portfolios. SBO was closed to new purchases in

the third quarter of 2007 and is in run-off with exposure down from $8.3

billion (31 December 2007) to $7.0 billion (31 December 2008).

Ireland residential mortgages

The residential mortgage portfolio in Ireland across the Ulster Bank and

First Active brands totalled £24.6 billion (as at 31 December 2008) with

92.8% in the Republic of Ireland and 7.2% in Northern Ireland. This

represents growth of 6% in the Republic of Ireland (ignoring exchange

rate movements) and 6% in Northern Ireland. During the course of

2008, Ulster Bank exited the 100% LTV market and tightened LTV and

affordability criteria in other segments. The arrears rate (three or more

payments missed) increased to 1.6% at 31 December 2008 from 0.8%

at end 2007 driven by deteriorating economic conditions. Repossession

remained low and totalled 37 for 2008.

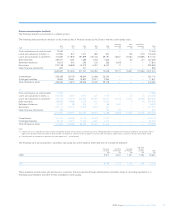

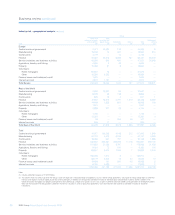

Financial institutions

The confidence and liquidity crisis affecting the banking sector saw the

near collapse of some major banks in Western countries along with the

fall of Lehman Brothers and the Icelandic banking system, which in turn

threatened the stability of national and global banking systems.

Government actions to restore stability by providing guarantees, liquidity

facilities, capital injections and facilitating the consolidation of weaker banks

with stronger ones met with some success. There remains a high level

of risk in the banking sector in 2009, particularly due to the deepening

recession that many countries face and increasing corporate defaults.

Financial Institutions constitute the largest segment of the Group’s

wholesale credit portfolio with exposure of £181 billion. Due to

difficulties faced by the sector, the portfolio quality has weakened

during 2008. 92% of exposure is to counterparties in developed OECD

countries while 90% of exposure is to investment grade counterparties.

The Banks portfolio is the biggest sub-sector with exposure of £86

billion. At the time of default, the Group’s exposures to Lehman Brothers

and the Icelandic banks totalled £802 million and £494 million

respectively and represented less than 1% of the total Banks portfolio.

2008 was a difficult year for the hedge funds sector. More hedge funds

collapsed during 2008 than in the previous ten years and the values of

many declined significantly. The spate of redemptions from investors

forced major hedge fund groups to halt withdrawals. The trends are set

to continue in 2009 and the contraction of this sector is expected.

The Group’s exposure to leveraged funds (including hedge funds)

totalled £10.3 billion. The majority of hedge funds are domiciled in the

UK and US but the portfolio is diversified by fund strategy. The Group’s

activities with hedge funds are primarily collateralised derivatives

trading. Exposures to funds encountering problems were reduced,

collateral margining was reviewed upwards to further mitigate risk and

the appropriateness of limits is regularly reviewed.

During 2009, the Group will continue to place emphasis on the pro-

active management of financial institutions at counterparty and portfolio

levels, recognising that liquidity is likely to remain tight and credit quality

is likely to deteriorate further across a range of portfolios.