RBS 2008 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

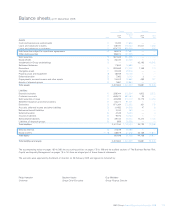

Accounting policies

RBS Group Annual Report and Accounts 2008178

1. Presentation of accounts

The accounts are prepared in accordance with International Financial

Reporting Standards issued by the International Accounting Standards

Board (IASB) and interpretations issued by the International Financial

Reporting Interpretations Committee of the IASB (together IFRS) as

adopted by the European Union (EU). The EU has not adopted the

complete text of IAS 39 ‘Financial Instruments: Recognition and

Measurement’; it has relaxed some of the standard’s hedging

requirements. The Group has not taken advantage of this relaxation and

has adopted IAS 39 as issued by the IASB: the Group’s financial

statements are prepared in accordance with IFRS as issued by the

IASB. The date of transition to IFRS for the Group and the company

(The Royal Bank of Scotland Group plc) and the date of their opening

IFRS balance sheets was 1 January 2004.

The Group adopted IFRS 8 ‘Operating Segments’ with effect from 1

January 2008. Early adoption of IFRS 8 has not materially affected

segmental disclosures.

In October 2008, the IASB issued and, the European Union endorsed,

amendments to IAS 39 ‘Financial Instruments: Recognition and

Measurement’ to permit the reclassification of financial assets out of

the held-for-trading (HFT) and available-for-sale (AFS) categories

subject to certain restrictions. Transfers must be made at fair value and

this fair value becomes the instruments’ new cost or amortised cost.

The amendments are effective from 1 July 2008. Reclassifications

made before 1 November 2008 were backdated to 1 July 2008;

subsequent reclassifications were effective from the date the

reclassification was made.

The Group has reclassified certain loans and debt securities out of the

held-for-trading and available-for-sale categories into the loans and

receivables category. It has also reclassified certain debt securities out

of the held-for-trading category into the available-for-sale category. The

balance sheet values of these assets, the effect of the reclassification

on the income statement and the impairment losses relating to these

assets are shown in Note 11 Financial instruments on page 208.

The 2007 comparative amounts have been restated for the netting of

certain derivative asset and derivative liability balances with the London

Clearing House as described in Note 13; the finalisation of the ABN AMRO

acquisition accounting as set out in Note 34; and for the classification of

Banco Real as a discontinued operation as described in Note 20.

The Group is not required to include reconciliations of shareholders’

equity and net income under IFRS and US GAAP in its filings with the

Securities and Exchange Commission in the US.

The company is incorporated in the UK and registered in Scotland.

The accounts are prepared on the historical cost basis except that the

following assets and liabilities are stated at their fair value: derivative

financial instruments, held-for-trading financial assets and financial

liabilities, financial assets and financial liabilities that are designated as

at fair value through profit or loss, available-for-sale financial assets and

investment property. Recognised financial assets and financial liabilities

in fair value hedges are adjusted for changes in fair value in respect of

the risk that is hedged.

The company accounts are presented in accordance with the

Companies Act 1985.

2. Basis of consolidation

The consolidated financial statements incorporate the financial

statements of the company and entities (including certain special

purpose entities) that continue to be controlled by the Group (its

subsidiaries). Control exists where the Group has the power to govern

the financial and operating policies of the entity; generally conferred by

holding a majority of voting rights. On acquisition of a subsidiary, its

identifiable assets, liabilities and contingent liabilities are included in the

consolidated accounts at their fair value. Any excess of the cost (the fair

value of assets given, liabilities incurred or assumed and equity

instruments issued by the Group plus any directly attributable costs) of

an acquisition over the fair value of the net assets acquired is

recognised as goodwill. The interest of minority shareholders is stated

at their share of the fair value of the subsidiary’s net assets.

The results of subsidiaries acquired are included in the consolidated

income statement from the date control passes up until the Group

ceases to control them through a sale or significant change in

circumstances.

All intra-group balances, transactions, income and expenses are

eliminated on consolidation. The consolidated accounts are prepared

using uniform accounting policies.

3. Revenue recognition

Interest income on financial assets that are classified as loans and

receivables, available-for-sale or held-to-maturity and interest expense

on financial liabilities other than those at fair value through profit or loss

are determined using the effective interest method. The effective

interest method is a method of calculating the amortised cost of a

financial asset or financial liability (or group of financial assets or

liabilities) and of allocating the interest income or interest expense over

the expected life of the asset or liability. The effective interest rate is the

rate that exactly discounts estimated future cash flows to the

instrument’s initial carrying amount. Calculation of the effective interest

rate takes into account fees payable or receivable, that are an integral

part of the instrument’s yield, premiums or discounts on acquisition or

issue, early redemption fees and transaction costs. All contractual terms

of a financial instrument are considered when estimating future cash

flows.

Financial assets and financial liabilities held-for-trading or designated as

at fair value through profit or loss are recorded at fair value. Changes in

fair value are recognised in profit or loss together with dividends and

interest receivable and payable.

Commitment and utilisation fees are determined as a percentage of the

outstanding facility. If it is unlikely that a specific lending arrangement

will be entered into, such fees are taken to profit or loss over the life of

the facility otherwise they are deferred and included in the effective

interest rate on the advance.