RBS 2008 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

RBS Group Annual Report and Accounts 2008112

Business review continued

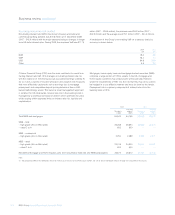

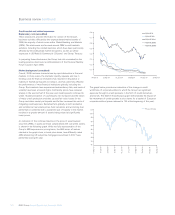

Non-trading interest rate VaR (audited)

Non-trading interest rate VaR for the Group’s treasury and retail and

commercial banking activities was £70.6 million at 31 December 2008

(2007 – £42.9 million) with the major exposure being to changes in longer

term US dollar interest rates. During 2008, the maximum VaR was £117.6

million (2007 – £53.6 million), the minimum was £53.9 million (2007 –

£32.9 million) and the average was £75.1 million (2007 – £43.2 million).

A breakdown of the Group’s non-trading VaR on a statutory basis by

currency is shown below.

Citizens Financial Group (CFG) was the main contributor to overall non-

trading interest rate VaR. CFG manages non-trading interest rate risk

with the objective of minimising accrual accounted earnings volatility. To

do so it uses a variety of income simulation and valuation risk measures

that more effectively capture the risk to earnings due to mortgage

prepayment and competitive deposit pricing behaviour than a VaR-

based methodology would. This balance sheet management approach

is common for US retail banks. Interest rate risk in the banking book is

managed by a professional treasury function which optimises the yield,

whilst staying within approved limits on interest rate risk, liquidity and

capitalisation.

Mortgages, home equity loans and mortgage-backed securities (MBS)

comprise a large portion of CFG’s assets. In the US, mortgage and

home equity customers may prepay loans without penalty. However,

under the requirements of FAS 133, the risk that they may do so cannot

be hedged in a cost effective manner and must be born by the lender.

Prepayment risk is a primary component of interest rate risk in the

banking book at CFG.

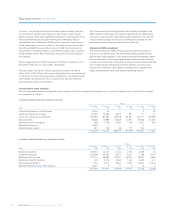

2008 2007

Carrying Carrying

Principal(1) amount Principal(1) amount

US$m US$m US$m US$m

Total MBS and mortgages 63,542 63,165 69,948 69,672

MBS – total

– high grade (AA or AAA rated) 26,268 25,893 26,848 26,572

– rated C to A 602 600 ——

MBS – commercial

– high grade (AA or AAA rated) 2,253 2,089 2,205 2,211

MBS – retail

– high grade (AA or AAA rated) 24,015 23,804 24,643 24,361

– rated C to A 602 600 ——

Residential Mortgage and Home Equity Loans (non-securitised, fixed rate and ARM, prepayable) 36,672 36,672 43,100 43,100

Note:

(1) The principal on MBS is the redemption amount on maturity or, in the case of an amortising instrument, the sum of future redemption amounts through the residual life of the security.

2008 2007

£m £m

EUR 19.0 4.5

GBP 18.3 7.3

USD 64.8 52.8

Other 4.5 2.6