RBS 2008 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

137

RBS Group Annual Report and Accounts 2008

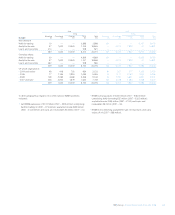

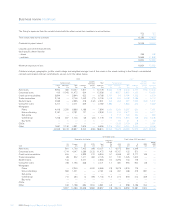

2008 2007

£m £m

Gross exposure to CDPCs 4,776 863

Credit valuation adjustment (1,311) (44)

Net exposure to CDPCs 3,465 819

2008 2007

Notional Notional

amount Fair value Credit amount Fair value Credit

protected protected Gross valuation protected protected Gross valuation

assets assets exposure adjustment assets assets exposure adjustment

£m £m £m £m £m £m £m £m

AAA/AA rated 19,092 15,466 3,626 908 20,605 19,742 863 44

A/BBB rated 6,147 4,997 1,150 403 ————

25,239 20,463 4,776 1,311 20,605 19,742 863 44

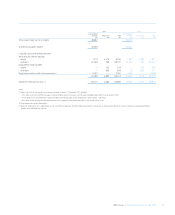

The movement in the year in CDPC CVA is analysed below:

£m

At 1 January 2008 44

Net benefit on CVA hedges 533

Net benefit on FX hedges 119

Net income statement effect 615

Balance at 31 December 2008 1,311

Credit derivative product companies

A credit derivative product company (CDPC) is a company that sells

protection on credit derivatives. CDPCs are similar to monoline insurers.

However, unlike monoline insurers, they are not regulated as insurers.

The Group has £4.8 billion of exposures with CDPCs which

predominatly relates to tranched credit derivatives. Tranched credit

derivatives have exposure to certain default losses that arise in

reference portfolio of assets. The Group has bought protection on

tranched credit derivatives from CDPCs. The reference portfolios of

assets are predominantly investment grade loans and bonds and on

average, the trades have exposure to total portfolio default losses that

exceed 16% of the portfolio notional up to a level of 50%. CDS spreads

have widened and credit protection has become more valuable and the

gross exposure to CDPC counterparties has increased. At the same

time, the credit quality of CDPC counterparties has declined, reflecting

the negative impact of their concentrated credit risk in a declining

market. As a result CVA adjustments taken against exposures to these

counterparties have increased significantly as described above.

The tables below present a comparison of the protected assets and the

fair value and CVA of the CDPC protection.