RBS 2008 Annual Report Download - page 279

Download and view the complete annual report

Please find page 279 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

RBS Group Annual Report and Accounts 2008278

Additional information continued

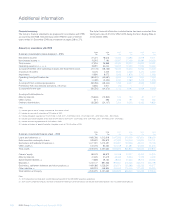

Economic and monetary environment

The world economy entered its most difficult period in a generation in

the second half of 2008. The failure of a large financial institution in

September coincided with the near-seizure of already fragile interbank

funding markets. Heightened risk aversion among investors led to

unprecedented volatility across global financial markets including

equities, fixed income and foreign exchange. Many asset prices

tumbled, with global real estate and equity markets the worst hit, while a

‘flight to quality’ prompted an historic rally in government bond markets

that pushed long-term risk free interest rates towards all time lows in

many developed economies.

The pronounced increase in commodity prices in the first half of 2008,

together with the intensifying financial crisis led to a further sharp

deterioration in private sector confidence in all major economies. Private

spending weakened significantly. Softer demand conditions adversely

affected prospects for profitability and employment. Policymakers

responded aggressively. Since September, governments have either

proposed or implemented measures that include the recapitalisation of

the banking sector, tax cuts and/or new infrastructure spending. Central

banks provided support through rate cuts and increased liquidity

provision. Despite these supportive actions, the global economy

remained on a downward trajectory at the beginning of 2009, with many

industrialised economies in recession.

In the UK, the Bank Rate fell from 5.5% at the beginning of 2008 to

1.0% in February 2009. The Bank of England remained cautious in the

first half of 2008, lowering policy rates a modest 25bps twice. Mounting

inflationary pressures were a major constraint, with the annual inflation

rate climbing as high as 5.2% in September, the highest reading since

the Bank of England’s operational independence in 1997, and some

way above the official target of 2%. Before October, the Bank focused

on liquidity measures to support the financial system. When it became

clear in the final quarter of 2008 that the confidence in the wider

economy had fallen to levels consistent with a deep contraction, policy

became more aggressive. The government assisted the recapitalisation

of the banking sector, while the Bank of England reduced rates rapidly,

from 5.0% in October to 1.0% in February 2009.

However, the economy had already gathered too much negative

momentum to stop an official recession – GDP declined by 2.1% in the

second half of 2008, and is widely expected to fall further in 2009. One

reason is lower policy rates have failed to translate effectively into looser

monetary conditions for the private sector. Three-month sterling LIBOR,

a key determinant of borrowing costs for households and firms,

remained on average almost 100bps above the prevailing Bank Rate,

well above its long-term average of 20bps. Sterling’s 17% depreciation

on a trade-weighted basis did not deliver a significant offset to

weakening domestic demand due to the difficult economic conditions

prevailing in the UK’s main trading partners.

US policy rates also declined substantially in 2008, from 4.25% in

January to effectively zero in December. With no room to cut interest

rates further, the Federal Reserve has since started to target longer term

market interest rates to directly lower the cost of funds for households

and firms, for example by purchasing mortgage-backed securities and

corporate commercial paper. More unorthodox policy measures are

likely this year. Similar to the UK, monetary policy failed to gain much

traction in the wider economy. Three-month US$ LIBOR averaged close

to 100bps higher than the prevailing policy rate.

The US officially entered recession in December 2007 and, in spite of a

fiscal stimulus in the first half of the year, activity continued to fall

through 2008 and is forecast to decline markedly in 2009. The effects

were acutely felt in employment, with US non-farm businesses shedding

2.6 million jobs in the twelve months to December. The dollar’s 11%

depreciation in 2007 helped to boost net exports, making trade the

single biggest contributor to GDP growth in 2008. However, this support

was fading in early 2009, due to slumping overseas demand.

The Eurozone started 2008 on a strong footing, with some member

countries experiencing above-trend growth in the first quarter. However,

for reasons that varied across countries, conditions worsened markedly

throughout the remainder of the year, and the region officially entered

recession in the second quarter. Growth in Germany, the region’s largest

economy and the world’s largest exporter, was hit hard by the slowdown

in global trade. Many of the more peripheral economies, like Ireland and

Spain, with higher debt levels were hit hard by the turbulence in credit

markets and falling asset prices. Economic activity in the entire region is

forecast to continue to contract in 2009.

Policy in the Eurozone was on average less supportive than in the UK or

the US, with the Repo Rate on hold at 4% in the first half of 2008. In

July 2008, the ECB raised rates by 25bps to fend off the dangers of

spiralling inflation. Official rates finally started to fall in October, when

the ECB participated in a globally co-ordinated rate cut to calm

investors’ fears amid intensifying strains in the global financial system.

The euro’s strong appreciation against the dollar also reduced the

competitiveness of the region’s exporters.

Initially, Asia Pacific appeared insulated from economic difficulties

elsewhere as China and India continued to grow strongly in the first half

of 2008. In fact, surging inflation reinforced concerns about overheating,

and prompted a series of policy measures aimed at cooling monetary

conditions. But this perception changed towards the end of 2008, when

recession in the major industrialised countries highlighted the region’s

exposure to a retrenchment in global trade. Growth forecasts have been

cut substantially, with 2009 growth in China and India potentially falling

to half its level from a year earlier. Increasing risk aversion of

international investors also led to large capital outflows, putting

downward pressure on floating currencies and local equity markets.

Exchange rates affect earnings and costs reported by the Group’s

non-UK subsidiaries, and the value of non-sterling denominated assets

and liabilities. Sterling weakened significantly during 2008, losing 28%

against the dollar and 30% against the euro, respectively. These

movements increase the sterling-value of non-sterling earnings, costs,

assets and liabilities. As a result, the Group recognises translation

benefits if it reports profits and/or has a positive net asset position

denominated in foreign currency.