RBS 2008 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

139

RBS Group Annual Report and Accounts 2008

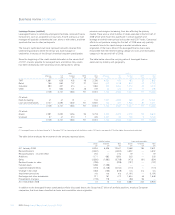

SPEs and conduits

SPEs (audited)

The Group arranges securitisations to facilitate client transactions and

undertakes securitisations to sell financial assets or to fund specific

portfolios of assets. The Group also acts as an underwriter and

depositor in securitisation transactions involving both client and

proprietary transactions. In a securitisation, assets, or interests in a pool

of assets, are transferred generally to a special purpose entity (SPE)

which then issues liabilities to third party investors. SPEs are vehicles

established for a specific, limited purpose, usually do not carry out a

business or trade and typically have no employees. They take a variety

of legal forms – trusts, partnerships and companies – and fulfil many

different functions. As well as being a key element of securitisations,

SPEs are also used in fund management activities to segregate custodial

duties from the fund management advice provided by the Group.

It is primarily the extent of risks and rewards assumed that determines

whether these entities are consolidated in the Group’s financial statements.

The following section aims to address the significant exposures which

arise from the Group’s activities through specific types of SPEs.

The Group sponsors and arranges own-asset securitisations, whereby

the sale of assets or interests in a pool of assets into an SPE is

financed by the issuance of securities to investors. The pool of assets

held by the SPE may be originated by the Group, or (in the case of

whole loan programmes) purchased from third parties, and may be of

varying credit quality. Investors in the debt securities issued by the SPE

are rewarded through credit-linked returns, according to the credit

rating of their securities. The majority of securitisations are supported

through liquidity facilities, other credit enhancements and derivative

hedges extended by financial institutions, some of which offer

protection against initial defaults in the pool of assets. Thereafter, losses

are absorbed by investors in the lowest ranking notes in the priority of

payments. Investors in the most senior ranking debt securities are

typically shielded from loss, since any subsequent losses may trigger

repayment of their initial principal.

The Group also employs synthetic structures, where assets are not sold

to the SPE, but credit derivatives are used to transfer the credit risk of the

assets to an SPE. Securities may then be issued by the SPE to investors,

on the back of the credit protection sold to the Group by the SPE.

In general residential and commercial mortgages and credit card

receivables form the types of assets generally included in cash

securitisations, while corporate loans and commercial mortgages

typically serve as reference obligations in synthetic securitisations.

The Group sponsors own-asset securitisations as a way of diversifying

funding sources, managing specific risk concentrations, and achieving

capital efficiency. The Group purchases the securities issued in own-

asset securitisations set up for funding purposes. During 2008, the

Group was able to pledge AAA-rated asset-backed securities as

collateral for repurchase agreements with major central banks under

schemes such as the Bank of England’s Special Liquidity Scheme,

launched in April 2008, which allowed banks to temporarily swap high-

quality mortgage-backed and other securities for liquid UK Treasury

Bills. This practice has contributed to the Group’s sources of funding

during 2008 in the face of the contraction in the UK market for inter-

bank lending and the investor base for securitisations.

The Group typically does not retain the majority of risks and rewards of

own-asset securitisations set up for the purposes of risk diversification

and capital efficiency, where the majority of investors tend to be third

parties. Therefore, the Group is typically not required to consolidate the

related SPEs.

The Group has also established whole loan securitisation programmes

in the US and UK where assets originated by third parties are

warehoused by the Group for securitisation. The majority of these

vehicles are not consolidated by the Group, as it is not exposed to the

risks and rewards of ownership.

Conduits (audited)

The Group sponsors and administers a number of asset-backed

commercial paper (ABCP) conduits. A conduit is an SPE that issues

commercial paper and uses the proceeds to purchase or fund a pool of

assets. The commercial paper is secured on the assets and is

redeemed either by further commercial paper issuance, repayment of

assets or liquidity drawings. Commercial paper is typically short-dated –

the length of time from issuance to maturity of the paper is typically up

to three months.

The Group’s conduits can be divided into multi-seller conduits and own-

asset conduits. In line with market practice, the Group consolidates both

types of conduit where it is exposed to the majority of risks and

rewards of ownership of these entities. The Group also extends liquidity

commitments to multi-seller conduits sponsored by other banks, but

typically does not consolidate these entities as it is not exposed the

majority of the risks and rewards.

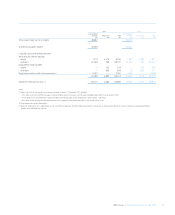

Funding and liquidity

The Group’s most significant multi-seller conduits have thus far

continued to fund the vast majority of their assets solely through ABCP

issuance. There were significant disruptions to the liquidity of the

financial markets during the year following the bankruptcy filing of

Lehman Brothers in September 2008 and this required a small amount

of the assets held in certain conduits to be funded by the Group rather

than through ABCP issuance. By the end of 2008 there had been an

improvement in market conditions, supported by central bank initiatives,

which enabled normal ABCP funding to replace this Group funding of

the conduits.

The average maturity of ABCP issued by the Group’s conduits as at 31

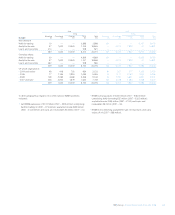

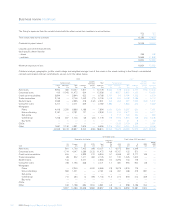

December 2008 was 72.1 days (2007 – 60.9 days).

The total assets held by the Group’s sponsored conduits are £49.9

billion (2007 – £48.1 billion). Since these liquidity facilities are

sanctioned on the basis of total conduit purchase commitments, the

liquidity facility commitments will exceed the level of assets held, with

the difference representing undrawn commitments.