RBS 2008 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

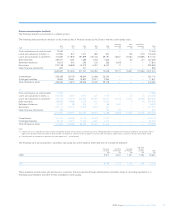

103RBS Group Annual Report and Accounts 2008

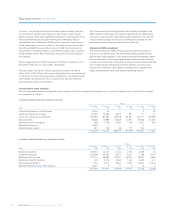

Liquidity risk (audited)

The Group’s liquidity policy is designed to ensure that the Group can at

all times meet its obligations as they fall due.

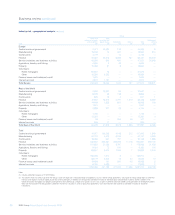

Liquidity management within the Group addresses the overall balance

sheet structure and the control, within prudent limits, of risk arising from

the mismatch of maturities across the balance sheet and from exposure

to undrawn commitments and other contingent obligations.

The management of liquidity risk within the Group is undertaken within a

formal governance structure. The Group Board of Directors oversees

the liquidity risk appetite and strategy of the Group; the Group

Executive Management Committee reviews the key liquidity metrics and

trends in the context of the Group’s overall risk profile; the Group Asset

and Liability Management Committee (GALCO), chaired by the Group

Finance Director and including the chief executives of the business

divisions as well as the Group Treasurer, Group Chief Risk Officer and

heads of other relevant Group functions, sets explicit metrics across a

number of asset and liability targets and these are cascaded to the

business and monitored by the Group Treasury and risk functions.

Group Treasury has overall responsibility for the daily monitoring and

control of the Group’s liquidity and funding positions. The Liquidity

Managers’ Forum is chaired and directed by the Group Treasurer with

membership including the Head of Short Term Markets and Financing,

GBM. The forum typically meets weekly with more frequent, ad hoc,

meetings as necessary. There are Regional and Country ALCOs that

oversee Group policy in our business in Europe, Asia and the Americas.

The Group is divided into Liquidity Reporting Units each of which is

required to have its own liquidity limits and contingency funding plan. In

addition, all subsidiaries and branches outside the UK are required to

comply with local regulatory liquidity requirements and are subject to

Group Treasury oversight.

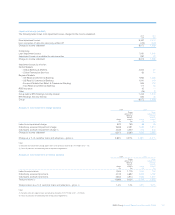

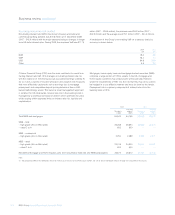

Management of term structure

The Group evaluates on a regular basis its structural liquidity risk and

applies a variety of balance sheet management and term funding

strategies to maintain this risk within its normal policy parameters. The

degree of maturity mismatch within the overall long-term structure of the

Group’s assets and liabilities is managed within internal policy

guidelines, aimed at ensuring term asset commitments may be funded

on an economic basis over their life. In managing its overall term

structure, the Group analyses and takes into account the effect of retail

and corporate customer behaviour on actual asset and liability

maturities where they differ materially from the underlying contractual

maturities.

Daily management

The primary focus of the daily management activity is to ensure access

to sufficient liquidity to meet cash flow obligations within key time

horizons, in particular out to one month ahead. The short-term maturity

structure of the Group’s liabilities and assets is managed daily to

ensure that all material or potential cash flow obligations, arising from

undrawn commitments and other contingent obligations can be met.

Potential sources include cash inflows from maturing assets, new

borrowings or the sale of various debt securities held (after allowing for

appropriate haircuts). Short-term liquidity risk is generally managed on

a consolidated basis with liquidity mismatch limits in place for

subsidiaries and non-UK branches which have material local treasury

activities, thereby assuring that the daily maintenance of the Group’s

overall liquidity risk position is not compromised. ABN AMRO, Citizens

Financial Group and RBS Insurance manage liquidity locally, given

different regulatory regimes, subject to review by Group Treasury. As

integration of ABN AMRO’s businesses within the Group proceeds, the

liquidity risk policies, parameters and metrics used will be progressively

aligned within a single framework.

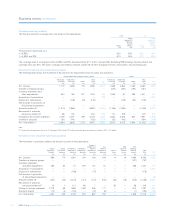

Stress testing

The Group performs stress tests to simulate how events may impact its

funding and liquidity capabilities. Such tests inform the overall balance

sheet structure and help define suitable limits for control of the risk

arising from the mismatch of maturities across the balance sheet and

from undrawn commitments and other contingent obligations. The form

and content of stress tests are updated where required as market

conditions evolve.

Contingency planning

Contingency funding plans have been developed to anticipate and

respond to approaching or actual material deterioration in market

conditions. The Group reviews its contingency plans in the light of

evolving market conditions. The contingency funding plan covers: the

available sources of contingent funding to supplement cash flow

shortages; the lead times to obtain such funding; the roles and

responsibilities of those involved in the contingency plans, including the

communication lines for escalation of events which give rise to liquidity

stress; assumptions, including the expected change impact of market

conditions; and the ability and circumstances within which the Group

accesses central bank liquidity.

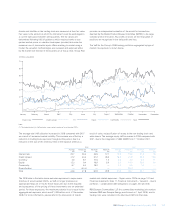

Global developments (unaudited)

The global financial system has experienced its greatest crisis in the

post war period and the dislocation became most acute in the second

half of 2008. This loss of confidence in the world’s banking system led

to massive dislocation in the capital markets and resulted in the

effective closure of the term debt and securitisation markets and money

markets. Government intervention in, and support for, the international

financial system has increased to unprecedented levels taking the form

of capital injections, guaranteed funding, asset insurance schemes and

expanded facilities from a number of central banks:

•In September 2007, the Bank of England announced that to alleviate

strains in longer-maturity money markets, it would conduct auctions to

provide funds at three month maturity against a wider range of

collateral, including mortgage collateral, than in its weekly open

market operations.