RBS 2008 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

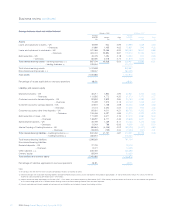

37RBS Group Annual Report and Accounts 2008

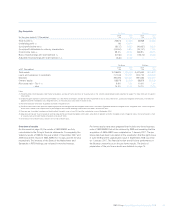

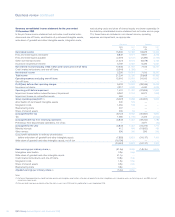

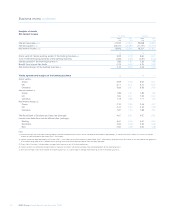

2008 compared with 2007 – pro forma

Profit

Group operating profit, excluding credit market write-downs and one-off

items, impairment losses on reclassified assets, amortisation of

purchased intangible assets, write-down of goodwill and other

intangible assets, integration costs, restructuring costs and share of

shared assets, was £80 million, compared with a profit of £10,314

million in 2007. The reduction is primarily a result of a substantial

decline in non-interest income, a number of specific losses such as

counterparty failures, and a marked increase in the credit impairment

charge, reflecting weakness in financial markets and a deteriorating

global economy.

Losses from previously disclosed credit market exposures increased to

£7,781 million, compared with £2,387 million in 2007, with the great

majority incurred in the first half of the year. Other one-off items

amounted to a credit of £1,674 million, 23% higher than in 2007,

principally as a result of a £1,232 million increase in the carrying value

of own debt carried at fair value. After integration costs, restructuring

costs, amortisation of purchased intangibles, write-down of goodwill

and other intangible assets and share of shared assets, the Group

recorded a loss before tax of £25,038 million, compared with a profit

before tax of £8,962 million in 2007.

After tax, minority interests and preference share dividends, the loss

attributable to ordinary shareholders was £24,051 million, compared

with an attributable profit of £6,823 million in 2007.

Total income

Total income, excluding credit market write-downs and one-off items,

declined by 20% to £26,875 million, with a significant deterioration

experienced during the second half of the year principally as a result of

£5.8 billion of trading asset write-downs, counterparty failure and

incremental reserving within GBM. While income increased in 2008 in

Global Transaction Services, and held steady in Regional Markets and

Insurance, a significant reduction occurred in Global Banking &

Markets, where a strong performance in rates, currencies and

commodities was offset by marked deterioration in credit markets and

equities.

Net interest income

Net interest income increased by 29% to £15,939 million, with average

loans and advances to customers up 17% and average customer

deposits up 6%. Group net interest margin rose from 2.00% to 2.10%

largely reflecting the success of the rates business in a declining

interest rate environment. However, margins tightened within Regional

Markets as market interest rates fell, with deposit markets remaining

competitive and price adjustments on lending taking some time to feed

through to the back book.

Non-interest income

Non-interest income was severely affected by the weakness in financial

markets experienced over the course of the year, particularly in the

fourth quarter. Excluding credit market write-downs and one-off items,

non-interest income totalled £10,936 million, 48% lower than in 2007.

While the decline was particularly marked in GBM’s credit markets and

equities businesses, with reduced business volumes and mounting

mark-to-market trading losses, Regional Markets also saw non-interest

income fall in the latter part of the year as declining consumer

confidence led to lower demand for credit and other financial products.

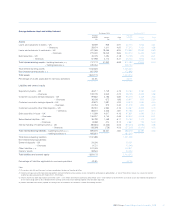

Operating expenses

Total operating expenses were reduced by 4% to £15,916 million, with

cost growth in the Group’s core retail and commercial banking

franchises offset by efficiency programmes and a significant reduction

in Global Banking & Markets staff costs. The Group cost:income ratio

deteriorated to 59.2%, compared with 49.5% in 2007, largely reflecting

the impact on income of the year’s difficult market conditions.

Net insurance claims

Net insurance claims fell by 13% to £3,917 million. General insurance

claims fell by 7%, reflecting improved risk selection, better claims

management and the non-recurrence of the severe floods experienced

in 2007. Bancassurance claims declined by 64% as a result of

movements in financial market values.

Impairment losses

Credit impairment losses (excluding reclassified assets) increased to

£6,962 million in 2008, compared with £2,104 million in 2007. The Group

experienced a pronounced deterioration in impairments in the second

half of the year, as financial stress spread to a broad range of

customers. The greatest increase in impairments occurred in GBM,

where fourth quarter impairments totalled £2,938 million, including a

loss of approximately £900 million on the Group’s exposure to

LyondellBasell. However, the Regional Markets businesses in all

geographies also experienced a noticeable increase in impairments in

the second half, particularly in the UK and Irish corporate and US

personal segments.

Impairments represented 0.46% of gross loans and advances, excluding

reverse repos, in the first half but reached 1.41% in the second half. For

2008 as a whole, impairments amounted to 0.91% of loans and

advances, excluding reverse repos, compared with 0.37% in 2007.

Risk elements in lending and potential problem loans at 31 December

2008 represented 2.69% of loans and advances, excluding reverse

repos, compared with 1.49% a year earlier. Provision coverage was

50%, compared with 59% at 31 December 2007 reflecting the higher

proportion of secured loans included in risk elements in lending and

potential problem loans.

Credit market losses

Losses for 2008 relating to the Group’s previously identified credit

market exposures totalled £7,781 million, net of hedging gains of

£1,642 million. This includes impairment losses of £466 million incurred

on credit market assets reclassified out of the ‘held-for-trading’ category

in line with the amendments to IAS 39 ‘Financial Instruments:

Recognition and Measurement’ issued in October. While the majority of

these write-downs were incurred in the first half of 2008, the severity of

the financial market dislocation intensified in the fourth quarter, resulting

in further losses in particular on the Group’s structured credit portfolios.