RBS 2008 Annual Report Download - page 207

Download and view the complete annual report

Please find page 207 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

Notes on the accounts continued

RBS Group Annual Report and Accounts 2008206

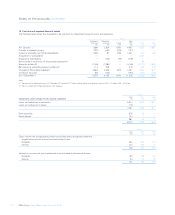

11 Financial instruments (continued)

Where these instruments have embedded optionality it is valued using a

variation of the Black-Scholes option pricing formula, and where they

have correlation exposure it is valued using a variant of the Gaussian

Copula model. The volatility or unique correlation inputs required to

value these products are generally unobservable and the instruments

are therefore deemed to be level 3 instruments.

Other derivatives

Exotic equity, interest rate and commodity options provide a payout (or

series of payouts) linked to the performance of one or more underlying,

including equities, interest rates, foreign exchange rates and

commodities. Included in commodities derivatives are energy contracts

entered into by RBS Sempra Commodities. Most of these contracts are

valued using models that incorporate observable data. A small number

are more complex, structured derivatives which incorporate in their

valuation assumptions regarding power price volatilities and correlation

between inputs, which are not market observable. These include certain

tolling agreements, where power is purchased in return for a given

quantity of fuel, and load deals, where a seller agrees to deliver a fixed

proportion of power used by a client’s utility customers.

Exotic options do not trade in active markets except in a small number

of cases. Consequently, the Group uses models to determine fair value

using valuation techniques typical for the industry. These techniques

can be divided, firstly, into modelling approaches and, secondly, into

methods of assessing appropriate levels for model inputs. The Group

uses a variety of proprietary models for valuing exotic trades.

Exotic valuation inputs include correlation between equities, interest

rates, foreign exchange rates and commodity prices. Correlations for

more liquid equity and rate pairs are valued using independently

sourced consensus pricing levels. Where a consensus pricing

benchmark is unavailable, these instruments are categorised as level 3.

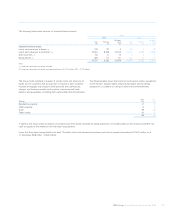

Reasonably possible alternative assumptions

In determining the effect of reasonably possible alternative assumptions

for unobservable inputs, the Group has considered credit derivative

trades with CDPCs separately from all other level 3 derivatives due to

the significant element of subjectivity in determining the counterparty

credit risk.

The fair value of credit derivative trades with CDPCs as at 31 December

2008 was £4.8 billion before applying a CVA of £1.3 billion. The Group’s

credit derivative exposures to CDPCs are valued using pricing models

with inputs observed directly in the market. An adjustment is made to

the model valuation as the creditworthiness of CDPC counterparties

differs from that of the credit risk assumptions used in the model. The

adjustment reflects the estimated cost of hedging the counterparty risk

arising from each trade. In the absence of market observable credit

spreads of CDPCs, the cost of hedging the counterparty risk is

estimated from an analysis of the underlying trades and the cost of

hedging expected default losses in excess of the capital available in

each vehicle. A reasonably possible alternative approach would be to

estimate the cost of hedging the counterparty risk from market

observable credit spreads of entities considered similar to CDPCs (for

example monoline insurers with similar business or similarly rated

entities). These reasonably possible alternative approaches would

reduce the fair value credit derivatives with CDPCs by up to £740 million

or increase the fair value by up to £600 million.

For all other level 3 derivatives, unobservable inputs are principally

comprised of correlations and volatilities. Where a derivative valuation

relies significantly on an unobservable input, the valuation is shown in

level 3. It is usual for such derivative valuations to depend on several

observable, and one or few unobservable model inputs. In determining

reasonably possible alternative assumptions, the relative impact of

unobservable inputs as compared to those which may be observed

was considered. Using reasonably possible alternative assumptions the

fair value of all other level 3 derivative assets (excluding CDPCs) would

be reduced by up to £600 million or increased by up to £560 million and

derivative liabilities of £4.0 billion, would be reduced by up to £300

million or increased by upto £280 million.

Equity shares – private equity

Private equity investments include unit holdings and limited partnership

interests primarily in corporate private equity funds, debt funds and fund

of hedges funds. Externally managed funds are valued using recent

prices where available. Where not available, the fair value of

investments in externally managed funds is generally determined using

statements or other information provided by the fund managers.

Although such valuations are provided from third parties, the Group

recognises that such valuations may rely significantly on the judgements

and estimates made by those fund managers, particularly in assessing

private equity components. Following the decline in liquidity in world

markets, the Group believes that there is sufficient subjectivity in such

valuations to report them in level 3.

Reasonably possible alternative valuations have been determined based

on the historic trends in valuations received, and by considering the

possible impact of market movements towards the end of the reporting

period, which may not be fully reflected in valuations received. Using

these reasonably possible alternate assumptions would reduce the fair

value of externally managed funds of £1.1 billion by up to £160 million

or increase the fair value by up to £80 million.

Other financial instruments

Other than the portfolios discussed above, there are other financial

instruments which are held at fair value determined from data which are

not market observable, or incorporating material adjustments to market

observed data. Using reasonably possible alternate assumptions

appropriate to the liability in question, such as credit spreads, derivative

inputs and equity correlations, would reduce the fair value of other

financial instruments held at fair value of £5.0 billion, primarily debt

securities in issue of £4.4 billion, by up to £250 million or increase the

fair value by up to £210 million.