RBS 2008 Annual Report Download - page 234

Download and view the complete annual report

Please find page 234 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

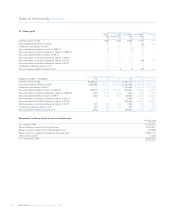

233RBS Group Annual Report and Accounts 2008

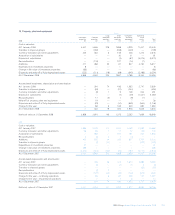

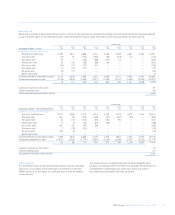

Assumptions 2008 2007 2006

Valuation interest rate

Term assurance 2.50% 3.00% 3.00%

Interest 2.50% 3.00% 3.00%

Unit growth 3.70% 3.50% 3.50%

Expense inflation 3.00% 4.00% 4.00%

Sample mortality rates, expressed as deaths per million per annum, for term assurance products (age 40).

Mortality

Male non-smoker 723 810 517

Male smoker 1,590 1,830 983

Female non-smoker 568 460 278

Female smoker 1,277 1,310 618

In 2007 the Group moved from the UK 80 series to the 00 series for mortality.

Expenses:

2008 2007 2006

Pre-2000 products – RSA per annum per annum per annum

Lifestyle protection plan £29.30 £25.18 £28.96

Mortgage savings plan £65.92 £56.67 £65.15

Pre-2000 products – NatWest Life

Term assurances £26.01 £26.01 £26.01

Linked life bonds £26.01 £23.17 £23.17

Post-2000 products

Term assurances £23.17 £23.16 £23.16

Guaranteed bonds £25.71 £25.71 £25.71

Life business

The Group’s three UK regulated life companies, National Westminster

Life Assurance Limited (NatWest Life), Royal Scottish Assurance plc

(RSA) and Direct Line Life Insurance Company Limited, are required to

meet minimum capital requirements at all times under the UK Financial

Service Authority’s Prudential Sourcebook. The capital resources

covering the regulatory requirement are not transferable to other areas

of the Group. To ensure that the capital requirement is satisfied at all

times, each company holds an additional voluntary buffer above the

regulatory minimum.

The Group is not exposed to price, currency, credit, or interest risk on

unit linked life contracts but it is exposed to variation in management

fees. A decrease of 10% in the value of the assets would reduce the

asset management fees by £5 million per annum (2007 – £2 million).

The Group writes insurance contracts with minimum guaranteed death

benefits that expose it to the risk that declines in the value of underlying

investments may increase the Group’s net exposure to death risk.

The Group’s long-term assurance contracts include whole-life, term

assurance, endowment assurances, flexible whole life, pension and

annuity contracts that are expected to remain in force for an extended

period of time.

Contracts under which the Group does not accept significant insurance

risk are classified as investment contracts. As required by IFRS 4

‘Insurance Contracts’ long term business provisions are calculated in

accordance with existing local GAAP (UK accounting standard FRS 27

‘Life Assurance’).

Estimations (assumptions) including future mortality, morbidity,

persistency and levels of expenses are made in calculating actuarial

reserves. Key metrics for the UK include: