RBS 2008 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

106

Business review continued

RBS Group Annual Report and Accounts 2008

Conduits – the Group’s most significant multi-seller conduits have thus

far continued to fund the vast majority of their assets solely through

ABCP issuance. There were significant disruptions to the liquidity of the

financial markets during the year following the bankruptcy filing of

Lehman Brothers in September 2008 and this required a small amount

of the assets held in certain conduits to be funded by the Group rather

than through ABCP issuance. By the end of 2008 there had been an

improvement in market conditions, supported by central bank initiatives,

which enabled normal ABCP funding to replace this Group funding of

the conduits.

The average maturity of ABCP issued by the Group’s conduits as at 31

December 2008 was 72.1 days (2007– 60.9 days).

The total assets held by the Group’s sponsored conduits are £49.9

billion (2007– £48.1 billion). Since these liquidity facilities are sanctioned

on the basis of total conduit purchase commitments, the liquidity facility

commitments will exceed the level of assets held, with the difference

representing undrawn commitments.

The Group values the funding flexibility and liquidity provided by the

ABCP market to fund client and Group-originated assets. Whilst there

are plans to decrease the multi-seller conduit business in line with the

Group’s balance sheet, the Group is reviewing the potential for new

own-asset conduit structures to add funding diversity.

Outlook for 2009 (unaudited)

The market outlook for 2009 remains uncertain with the prospect of

recession on a global scale. The wholesale funding markets remain

difficult with a high degree of risk aversion towards the banking market

and no restoration of the unguaranteed debt capital markets for bank

issuance yet visible. The continuation of these conditions means that the

use of central bank and other government facilities are likely to be

required for some time. Other deposit initiatives have commenced to

widen wholesale and other retail deposit gathering actions.

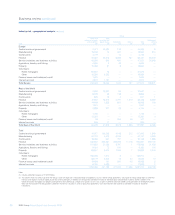

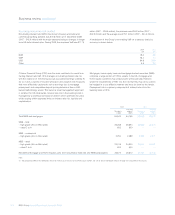

Group balance sheet (audited)

The following tables show the contractual undiscounted cash flows receivable and payable up to a period of twenty years including future receipts

and payments of interest.

On balance sheet assets by contractual maturity

Group

0-3 months 3-12 months 1-3 years 3-5 years 5-10 years 10-20 years

2008 £m £m £m £m £m £m

Cash and balances at central banks 12,333 25 —— 229

Loans and advances to banks 61,630 19,369 2,673 921 111 70

Loans and advances to customers 195,553 81,054 138,378 125,621 160,271 152,084

Debt securities 26,006 12,895 24,629 23,927 57,846 24,535

Derivatives held for hedging 266 1,796 2,281 1,359 1,517 649

Settlement balances 17,830 ——— 2—

Other financial assets 621 193 58 111 343 —

314,239 115,332 168,019 151,939 220,092 177,367

On balance sheet liabilities by contractual maturity

Group

0-3 months 3-12 months 1-3 years 3-5 years 5-10 years 10-20 years

2008 £m £m £m £m £m £m

Deposits by banks 154,614 14,347 3,345 2,754 2,048 34

Customer accounts 523,268 33,450 6,577 6,337 7,298 5,319

Debt securities in issue 131,714 48,652 40,067 38,223 38,667 5,626

Derivatives held for hedging 394 2,216 2,543 1,334 2,682 1,373

Subordinated liabilities 1,753 4,271 6,824 5,793 24,503 13,030

Settlement balances and other liabilities 13,351 5 12 6 10 6

825,094 102,941 59,368 54,447 75,208 25,388