RBS 2008 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

127

RBS Group Annual Report and Accounts 2008

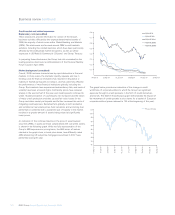

Residential mortgage-backed securities (audited)

Residential mortgage backed securities (RMBS) are securities that

represent an interest in a portfolio of residential mortgages.

Repayments made on the underlying mortgages are used to make

payments to holders of the RMBS. The risk of the RMBS will vary

primarily depending on the quality and geographic region of the

underlying mortgage assets and the credit enhancement of the

securitisation structure.

Several tranches of notes are issued, each secured against the same

portfolio of mortgages, but providing differing levels of seniority to

match the risk appetite of investors. The most junior (or equity) notes will

suffer early capital and interest losses experienced by the referenced

mortgage collateral, with each more senior note benefiting from the

protection provided by the subordinated notes below. Additional credit

enhancements may be provided to the holder of senior RMBS notes,

including guarantees over the value of the exposures, often provided by

monoline insurers.

The main categories of mortgages that serve as collateral to RMBS held

by the Group are described below. As can be seen from the table

below, the Group’s RMBS portfolio covers a range of geographic

locations and different categories are used to classify the exposures

depending on the geographical region of the underlying mortgage.

These categories are described below. The US market has more

established definitions of differing underlying mortgage quality and

these are used as the basis for the Group’s RMBS categorisation.

Sub-prime mortgages: are loans to sub-prime borrowers typically

having weakened credit histories that include payment delinquencies,

and potentially more severe problems such as court judgements and

bankruptcies. They may also display reduced repayment capacity as

measured by credit scores, high debt-to-income ratios, or other criteria

indicating heightened risk of default.

Non-conforming mortgages (or ‘Alt-A’ used for US exposure) have a

higher credit quality than sub-prime mortgages, but lower than those

prime borrowers. Within the US mortgage industry, non-conforming

mortgages are those that do not meet the lending criteria for US agency

mortgages (described below). For non-US mortgages, judgement is

applied in identifying loans with similar characteristics to US non-

conforming loans and also include self-certified loans. Alt-A describes a

category of mortgages in which lenders consider the risk to be greater

than prime mortgages though less than sub-prime. The offered interest

rate is usually representative of the associated risk level.

Guaranteed mortgages are mortgages that form part of a mortgage

backed security issuance by a government agency, or in the US an

entity that benefits from a guarantee (direct or indirect) provided by the

US government. For US RMBS, this category includes, amongst others,

RMBS issued by Ginnie Mae, Freddie Mac and Fannie Mae. For

European RMBS, this includes mortgages guaranteed by the Dutch

Government.

Other prime mortgages are those of a higher credit quality than non-

conforming and sub-prime mortgages, and exclude guaranteed

mortgages.

Covered mortgage bonds are debt instruments that have recourse to a

pool of mortgage assets, where investors have a preferred claim if a

default occurs. These underlying assets are segregated from the other

assets held by the issuing entity. These underlying assets are

segregated from other assets held by the issuing entity.

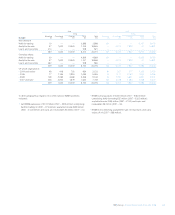

The tables below show the Group’s RMBS net exposures and carrying

values by measurement classification, underlying asset type, the main

geographical locations of the property that the mortgage is secured

against, and the year in which the underlying mortgage was originated.

2008 2007

Non Prime Non Prime

Sub-prime conforming Guaranteed(2) Other(3) Total Sub-prime conforming Guaranteed(2) Other(3) Total

£m £m £m £m £m £m £m £m £m £m

Net exposure: (1)

Held-for-trading 345 346 18,631 5,140 24,462 3,497 2,913 15,627 13,068 35,105

Available-for-sale 572 2,184 22,546 19,148 44,450 139 865 16,539 10,332 27,875

Loans and receivables 527 1,482 — 569 2,578 5——— 5

Designated at fair value 16 ——166 182 18 ——72 90

1,460 4,012 41,177 25,023 71,672 3,659 3,778 32,166 23,472 63,075

Carrying values: (2)

Held-for-trading 1,594 352 18,631 7,272 27,849 5,073 2,913 15,627 13,667 37,280

Available-for-sale 913 2,183 22,546 19,149 44,791 139 865 16,545 10,331 27,880

Loans and receivables 566 1,482 — 570 2,618 5——— 5

Designated at fair value 16 ——166 182 18 ——72 90

3,089 4,017 41,177 27,157 75,440 5,235 3,778 32,172 24,070 65,255

Notes:

(1) Net exposures reflect the effect of hedge protection purchased from monolines and other counterparties but excludes the effect of counterparty credit valuation adjustment. Carrying value is the

amount recorded on the balance sheet.

(2) Prime guaranteed exposures and carrying values include:

• £7.6 billion (2007 – £6.0 billion) available-for-sale exposures guaranteed by the Dutch government

• £5.7 billion (2007 – £5.0 billion) guaranteed by US government via Ginnie Mae of which £0.5 billion (2007 – £0.3 billion) are held-for-trading

• £27.8 billion (2007 – £ 21.0 million) effectively guaranteed by the US government via its support for Freddie Mac and Fannie Mae of which £18.1 billon (2007 – £15.2 billion) are held-for-trading

(3) Other prime mortgage exposures include £10.0 billion (2007 – £7.8 billion) covered European mortgage bonds.