RBS 2008 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

91RBS Group Annual Report and Accounts 2008

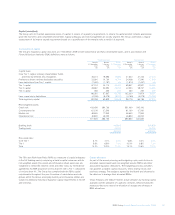

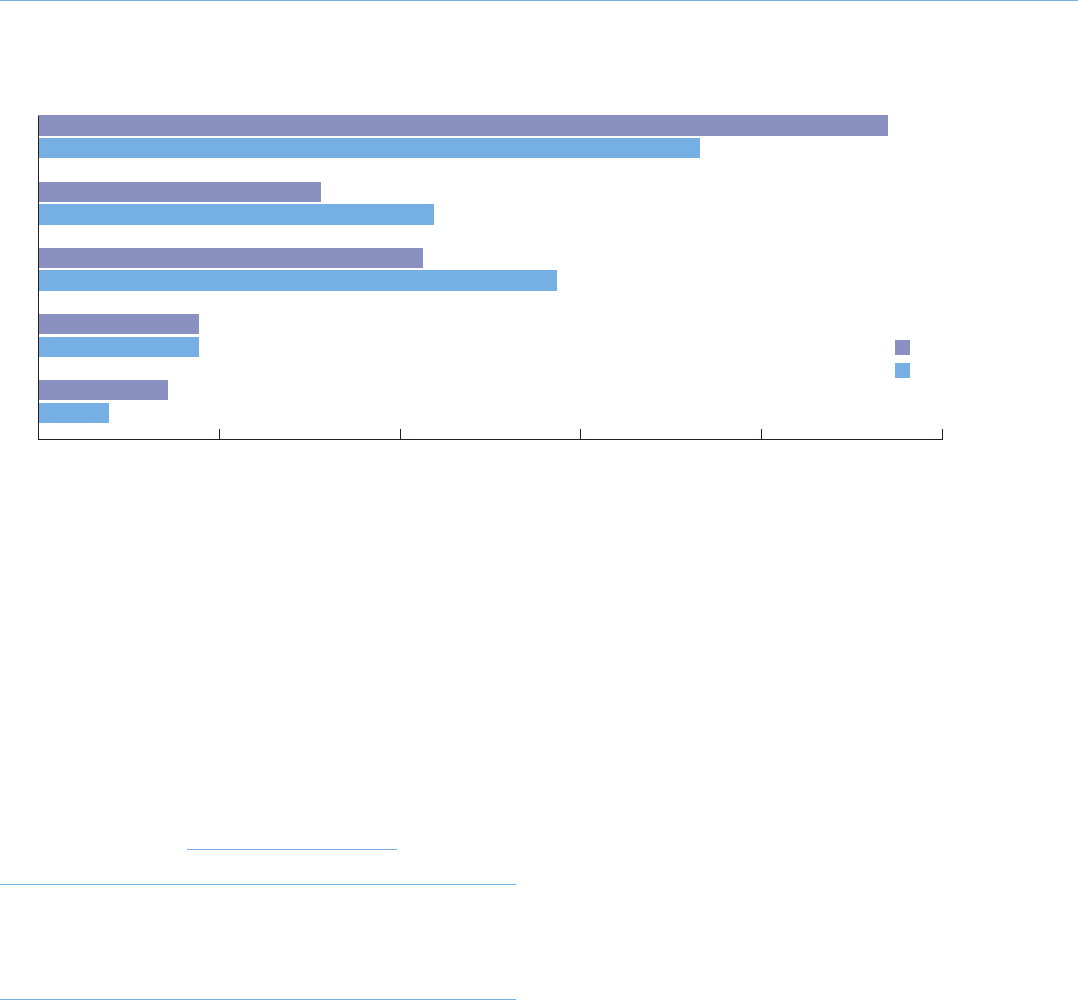

The following table shows the movement between 2007 and 2008 based on the old AQ1-5 bands. (unaudited)

AQ1

AQ2

AQ3

AQ4

AQ5

2007

2008

0% 10% 20% 30% 40% 50%

Note:

(1) Graph data are shown net of provisions, reverse repurchase agreements and issuer risk for 2008 and 2007.

(unaudited)

As at 31 December 2008, including ABN AMRO net of minority interest,

exposure to investment grade counterparties (AQ1) accounted for 47%

(2007 – 37%) of credit risk assets and 46% (2007 – 59%) of exposures

were to counterparties between AQ2 and AQ4. The exposure to the

lowest asset quality (AQ5) is 7% (2007 – 4%).

Expressed as an annual PD, the upper and lower boundaries and the

midpoint for each of these Group level asset quality grades are as

follows:

Annual probability of default

Minimum Midpoint Maximum S&P

Asset quality grade %%%equivalent

AQ1 0.00 0.10 0.20 AAA to BBB-

AQ2 0.21 0.40 0.60 BB+ to BB

AQ3 0.61 1.05 1.50 BB- to B+

AQ4 1.51 3.25 5.00 B+ to B

AQ5 5.01 52.50 100.00 B and below

Key credit portfolios (unaudited)

All exposures are monitored closely, but in the current environment the

following are under specific scrutiny:

Property lending (unaudited)

Commercial property

The commercial property portfolio totals £97 billion. The bulk of this is

concentrated in GBM (£31 billion) and RBS UK (£42 billion) with the

remainder in Ulster Bank (£17 billion) and CFG (£6 billion).

Lending falls into different categories and is spread across Investment

(72.6%), Development (24.1%) and Other (3.3%). Speculative lending

represents 1.6% of this portfolio. 58% of the lending is in the UK, 30%

Western Europe, 8% North America and 4% RoW but with the extent of

the current global downturn all markets are coming under considerable

pressure.

Whilst the Group expects to see an overall deterioration in LTV ratios,

72% of the portfolio within GBM and UKCB continue to have an LTV less

than 75% and an average interest coverage ratio (ICR) for GBM of

164% and 151% for RBS UK. The Group’s lending approach has always

been predominantly cash flow driven and areas of stress in the portfolio

will primarily be impacted by the wider corporate and economic

environment affecting tenant quality with the retail sector being an area

of focus at the present time.

The Group has experienced a number of defaults in its Spanish portfolio

with current limits of £2 billion managed via the Global Restructuring

Group. Total impaired limits across the portfolio are £3.9 billion. Limits

currently subject to a higher level of monitoring (watch) total £18.9

billion and are actively risk managed.

The outlook for commercial property will remain challenging during

2009 with further falls in capital values expected due to a lack of

liquidity and weak demand for assets. There is emerging evidence of

falling rents and increasing vacancy rates although downward pressure

on rents and longer void periods can be expected due to the weakening

economic climate. The Group’s strategy throughout 2008 has been to

reduce its exposures wherever prudent, continuing the process of

tightening lending parameters begun in the second half of 2007.

Residential mortgages

The Group originates residential mortgages through retail channels in all

four divisions within Regional Markets however activity is primarily in the

UK, the US and Ireland.