RBS 2008 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

59RBS Group Annual Report and Accounts 2008

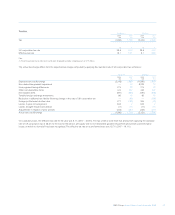

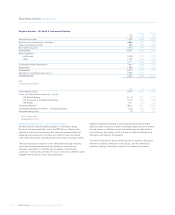

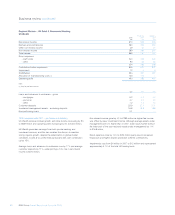

Regional Markets – US Retail & Commercial Banking

Pro forma Statutory

2008 2007 2007

£m £m £m

Net interest income 2,106 1,935 1,935

Non-interest income 904 846 846

Total income 3,010 2,781 2,781

Direct expenses

– staff costs 675 598 598

– other 411 364 364

1,086 962 962

Contribution before impairment 1,924 1,819 1,819

Impairment – core 722 177 177

Impairment – SBO 319 163 163

Contribution 883 1,479 1,479

Allocation of manufacturing costs (1) 359 336 —

Operating profit 524 1,143 1,479

Note:

(1) Only for pro forma results.

US$bn US$bn US$bn

Total assets 151.8 159.2 159.2

Loans and advances to customers – gross

– mortgages 15.7 19.1 19.1

– home equity 34.8 35.9 35.9

– other consumer 21.3 21.6 21.6

– corporate and commercial 41.2 37.6 37.6

Customer deposits 94.3 105.8 105.8

Non-performing loans 1.1 0.6 0.6

Average exchange rate – US$/£ 1.853 2.001 2.001

Spot exchange rate – US$/£ 1.460 2.004 2.004

2008 compared with 2007 – pro forma and statutory

US Retail & Commercial Banking held income steady in 2008 at $5,578

million, but experienced a sharp increase in impairment losses as

economic conditions progressively worsened over the course of the

year. As a result, operating profit declined to $972 million, down 57%.

In sterling terms, total income increased by 8% to £3,010 million while

operating profit declined by 54% to £524 million.

Total income of $5,578 million was essentially unchanged, with 11%

growth in commercial banking to $1,231 million offsetting a 2% decline

in retail banking income to $4,347 million. Both segments were affected

by the deterioration in credit conditions, with retail contribution down 58%

to $926 million and commercial contribution down 7% to $711 million.

Overall, net interest income grew modestly, offset by a small decline in

non-interest income. Average loans and advances to retail customers

decreased as a result of the slowing economy and tighter underwriting

standards, but this decline was offset by continued strong growth in

corporate and commercial lending. Core customer deposits declined by

5% and the division further reduced its reliance on brokered deposits

by 80%, leading to an overall decline of 11% in total customer deposits.

Net interest margin was held steady at 2.73%, reflecting widening asset

margins and management of savings rates in a competitive deposit market.

Direct expenses increased by 5% to $2,012 million, reflecting increased

costs from the expansion of the commercial banking relationship

management teams, write-downs on mortgage servicing rights, and

higher costs related to loan work-out and collection activity.

Credit conditions worsened significantly over the course of the year as

the housing market continued to deteriorate and unemployment rose,

exacerbating already challenging conditions. Impairment losses totalled

$1,929 million, up 184% from 2007 reflecting the deterioration in

economic conditions.

In the core US Retail & Commercial portfolio, 2008 impairment losses

totalled $1,337 million, with a marked increase in the second half.

Consumer non-performing loans represented 0.37% of core home

equity balances and 1.20% of residential mortgage balances. While

there has been a decline in some customers’ credit scores in line with

weakening economic conditions, refreshed weighted average FICO

scores for consumer real estate-secured lending at 31 December 2008

was approximately 740 with a weighted average LTV of 63%. Stress has

emerged in all consumer segments during the second half of the year,

with increased delinquency in core home equity (up 10bps to 0.86%),

and auto (up 94bps to 2.78%). US Retail & Commercial does not

originate negative amortization mortgages or option adjustable rate

mortgages. Closing provision balances for the core portfolio were

$1,303 million compared with $777 million at the end of 2007.