RBS 2008 Annual Report Download - page 206

Download and view the complete annual report

Please find page 206 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

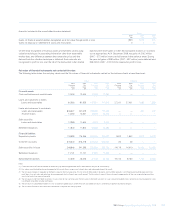

205RBS Group Annual Report and Accounts 2008

Due to the subjectivity of the inputs to the pricing model, alternative

valuation points are constructed to benchmark the output of the model.

These valuation points include determining an ABS index implied

collateral valuation, which provides a market calibrated valuation data

point. A collateral net asset value methodology is also considered which

uses dealer buy side marks to determine an upper bound for super

senior CDO valuations. Both the ABS index implied valuation and the

collateral net asset value methodology apply an assumed immediate

liquidation approach.

The Group, using all pricing points available, may make necessary and

appropriate valuation adjustments to the pricing information derived

from the proprietary model. These adjustments reflect the Group’s

assessment of factors that market participants would consider in setting

a price, to the extent that these factors that have not already been included

in the model and may include adjustments made for liquidity discounts.

In order to provide disclosures of the valuation of super senior CDOs

using reasonably possible alternative assumptions, the Group has

considered macroeconomic conditions, including house price

appreciation and depreciation, and the effect of regional variations. The

output from using these alternative assumptions has been compared

with inferred pricing from other published data. The Group believes that

reasonably possible alternative assumptions could reduce or increase

valuations by up to 4%. Using these alternative assumptions would

reduce the fair value of level 3 CDOs of £1.7 billion by up to £440 million

(super senior CDOs: £292 million) and increase the fair value by up to

£410 million (super senior CDOs: £292 million).

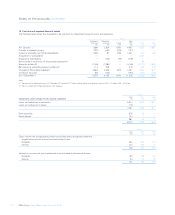

Collateralised loan obligations

To determine the fair value of CLOs purchased from third parties, the

Group use third-party broker or lead manager quotes as the primary

pricing source. These quotes are benchmarked to consensus pricing

sources where they are available.

For CLOs originated and still held by the Group, the fair value is

determined using a correlation model based on a Monte Carlo

simulation framework. The main model inputs are credit spreads and

recovery rates of the underlying assets and their correlation. A credit

curve is assigned to each underlying asset based on prices, from third-

party dealer quotes, and cash flow profiles, sourced from an industry

standard model. Losses are calculated taking into account the

attachment and detachment point of the exposure. As the correlation

inputs to this model are not observable CLOs are deemed to be level 3.

Using reasonably possible alternative assumptions the fair value of

CLOs of £1.0 billion would be £40 million lower or £40 million higher.

Other debt securities

Other level 3 debt securities comprise £1.4 billion of other ABS and

£1.7 billion of other debt securities. Where observable market prices for

a particular debt security are not available, the fair value will typically be

determined with reference to observable market transactions in other

related products, such as similar debt securities or credit derivatives.

Assumptions are made about the relationship between the individual

debt security and the available benchmark data. Where significant

management judgement has been applied in identifying the most relevant

related product, or in determining the relationship between the related

product and the instrument itself, the valuation is shown in level 3. Using

differing assumptions about this relationship would result in different fair

values for these assets. The main assumption made is that of relative

creditworthiness. Using reasonably possible alternative assumption

credit assumptions, taking into account the underlying currency, tenor,

and rating of the debt securities within each portfolio, would reduce the

fair value of other debt securities of £3.1 billion by up to £50 million or

increase the fair value by up to £50 million.

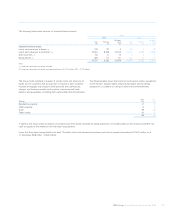

Derivatives

Level 3 derivative assets comprised credit derivatives of £8.0 billion, equity

derivatives of £0.1 billion and interest rate, foreign exchange rate and

commodity derivative contracts of £2.2 billion. Derivative liabilities

comprise credit derivatives of £2.6 billion interest rate, foreign exchange

rate and commodity derivatives contracts of £1.4 billion.

Derivatives are priced using quoted prices for the same or similar

instruments where these are available. However, the majority of

derivatives are valued using pricing models. Inputs for these models are

usually observed directly in the market, or derived from observed

prices. However, it is not always possible to observe or corroborate all

model inputs. Unobservable inputs used are based on estimates taking

into account a range of available information including historic analysis,

historic traded levels, market practice, comparison to other relevant

benchmark observable data and consensus pricing data.

Credit derivatives

The Group’s credit derivatives include vanilla and bespoke portfolio

tranches, gap risk products and certain other unique trades. The

bespoke portfolio tranches are synthetic tranches referenced to a

bespoke portfolio of corporate names on which the Group purchases

credit protection. Bespoke portfolio tranches are valued using Gaussian

Copula, a standard method which uses observable market inputs

(credit spreads, index tranche prices and recovery rates) to generate an

output price for the tranche via a mapping methodology. In essence this

method takes the expected loss of the tranche expressed as a fraction

of the expected loss of the whole underlying portfolio and calculates

which detachment point on the liquid index, and hence which

correlation level, coincides with this expected loss fraction. Where the

inputs into this valuation technique are observable in the market,

bespoke tranches are considered to be level 2 assets. Where inputs are

not observable, bespoke tranches are considered to be level 3 assets.

However, all transactions executed with a CDPC counterparty are

considered level 3 as the counterparty credit risk assessment is a

significant component of these valuations.

Gap risk products are leveraged trades, with the counterparty’s

potential loss capped at the amount of the initial principal invested. Gap

risk is the probability that the market will move discontinuously too quickly

to exit a portfolio and return the principal to the counterparty without

incurring losses, should an unwind event be triggered. This optionality is

embedded within these portfolio structures and is very rarely traded

outright in the market. Gap risk is not observable in the markets and, as

such, these structures are deemed to be level 3 instruments.

Other unique trades are valued using a specialised model for each

instrument and the same market data inputs as all other trades where

applicable. By their nature, the valuation is also driven by a variety of

other model inputs, many of which are unobservable in the market.