RBS 2008 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

87RBS Group Annual Report and Accounts 2008

Credit concentration risk (including country risk) (audited)

The Group defines three key areas of concentration in credit risk that

are monitored, reported and managed at Group and divisional levels.

These are single name concentration, industry/sector and country risk.

The Group has a series of quantitative and qualitative controls in place

to limit the amount of concentration risk in credit portfolios.

A threshold is set on the aggregate LGD to a single customer group

above which approval is required from the Group’s most senior credit

committee, the Advances Committee.

During the year work progressed on an enhancement of the frameworks

for managing single name and sector concentrations. These

enhancements are planned to be fully implemented in 2009 to improve

the identification and management of concentrations in the portfolio

through the introduction of additional parameters and increased

scrutiny of concentration limit excesses.

A stress testing framework, Correlated Exposure Loss Testing, assesses

the impact on the Group’s impairment charge of non-systemic events

that affect groups of inter-related sectors in order to limit the impact of

these scenarios to within defined tolerances.

Country risk arises from sovereign events (e.g. default or restructuring);

economic events (e.g. contagion of sovereign default to other parts of

the economy, cyclical economic shock); political events (e.g.

convertibility restrictions and expropriation or nationalisation) and natural

disaster or conflict. Losses are broadly defined and include credit,

market, liquidity, operational and franchise risk related losses. The

acquisition of ABN AMRO materially increased the Group's country risk

profile, therefore significant enhancements to the Group’s country risk

framework have been implemented and continue to be developed.

It is the Group’s policy to monitor and control country risk exposures

and to avoid excessive concentrations. The Group’s appetite is

expressed by a matrix of limits by country risk grade and is approved

by GEMC. The Group’s exposure is managed and measured within this

appetite by the Group Country Risk Management Committee (GCRMC),

that has delegated authority from the GRC to manage country risk and

agree related policy. Membership of GCRMC comprises the Group

Chief Credit Officer, Heads of Credit and business representatives from

those divisions with material country risk exposures. GCRMC sets limits

for each country based on a risk assessment taking into account the

Group’s franchise and business mix in that country. Additional limitations

– on product types with higher loss potential and longer tenor

transactions, for example – may be established depending on the

country outlook and business strategy. A country watch list framework is

in place to proactively monitor emerging issues and facilitates the

development of mitigation strategies.

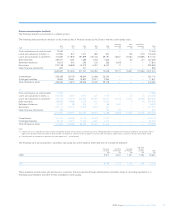

The country risk table below shows credit risk assets exceeding £1 billion

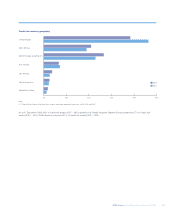

by borrower domicile and is stated gross of mitigating action which may

have been taken to reduce or eliminate exposure to country risk events.

Banks and

financial

Consumer Sovereign institutions Corporate Total

Risk countries (unaudited) £m £m £m £m £m

Russia 51.0 — 362.0 5,361.0 5,774.0

United Arab Emirates 756.8 91.5 1,721.9 2,988.6 5,558.8

India 1,020.0 5.7 737.9 3,800.6 5,564.2

Turkey 24.8 363.6 603.2 3,035.5 4,027.1

China 24.6 61.1 1,146.3 2,027.2 3,259.2

South Korea 1.5 — 1,743.0 1,104.1 2,848.6

Taiwan 1,019.3 — 1,393.2 825.0 3,237.5

Mexico 4.2 57.1 210.9 1,999.9 2,272.1

Czech Republic 2.1 593.5 175.5 1,057.9 1,829.0

Kazakhstan 69.5 17.0 900.8 858.9 1,846.2

Poland 6.8 38.5 309.1 1,308.6 1,663.0

Chile 0.3 26.1 383.7 1,250.5 1,660.6

Brazil 3.6 — 1,012.3 641.7 1,657.6

Saudi Arabia 23.2 — 534.9 679.4 1,237.5

Romania 583.6 145.3 160.4 916.8 1,806.1

Greece 15.1 135.3 210.3 702.7 1,063.4

Hungary 5.1 73.9 101.3 831.4 1,011.7

Note:

(1) Risk countries are defined as those with an internal rating of A+ and below. In addition, United Arab Emirates is included which has a rating of AA.

(unaudited)

The outlook for developing markets in 2009 is very challenging, as

developed economy demand is weak, liquidity conditions are tight and

risk appetite is yet to return. Asian growth is slowing sharply as trade

contracts, but generally, both sovereign and private sector leverage is

lower than during the 1998 crisis, providing scope for recovery. The

Middle East is more insulated from the effects of economic disruption

but certain high growth countries, such as UAE, will face challenges.

Eastern Europe faces a deep correction as large economic imbalances

unwind. Falling commodity prices and US weakness will also affect

Latin America, but the region is more resilient than during previous

downturns due to reform progress and policy orthodoxy in its largest

economies.