RBS 2008 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

RBS Group Annual Report and Accounts 2008214

Notes on the accounts continued

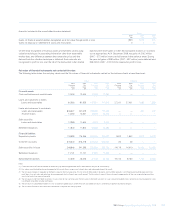

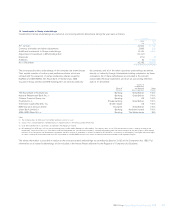

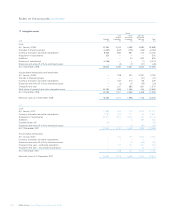

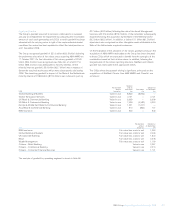

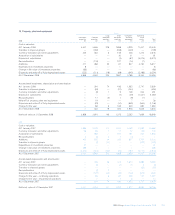

13 Derivatives

Companies in the Group transact derivatives as principal either as a

trading activity or to manage balance sheet foreign exchange, interest

rate and credit risk.

The Group enters into fair value hedges, cash flow hedges and hedges

of net investments in foreign operations. The majority of the Group’s

interest rate hedges relate to the management of the Group’s non-

trading interest rate risk. The Group manages this risk to Value-at-Risk

limits. The risk is assessed using gap reports that show maturity

mismatches. To the extent that such mismatches exceed predetermined

limits they are closed by executing derivatives principally interest rate

swaps. Suitable larger ticket financial instruments are fair value hedged;

the remaining exposure, where possible, is hedged by derivatives

documented as cash flow hedges and qualifying for hedge accounting.

The majority of the Group’s fair value hedges involve interest rate swaps

hedging the interest rate risk in recognised financial assets and

financial liabilities. Cash flow hedges relate to exposure to variability in

future interest payments and receipts on forecast transactions and on

recognised financial assets and financial liabilities. The Group hedges

its net investments in foreign operations with currency borrowings and

forward foreign exchange contracts.

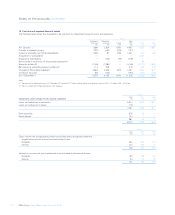

For cash flow hedge relationships of interest rate risk, the hedged items

are actual and forecast variable interest rate cash flows arising from

financial assets and financial liabilities with interest rates linked to LIBOR,

EURIBOR or the Bank of England Official Bank Rate. The financial

assets are customer loans and the financial liabilities are customer

deposits and LIBOR linked medium-term notes and other issued

securities. As at 31 December 2008, variable rate financial assets of

£34.6 billion and variable rate financial liabilities of £56.4 billion were

hedged in such cash flow hedge relationships.

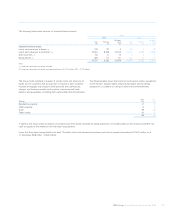

For cash flow hedging relationships, the initial and ongoing prospective

effectiveness is assessed by comparing movements in the fair value of

the expected highly probable forecast interest cash flows with

movements in the fair value of the expected changes in cash flows from

the hedging interest rate swap or by comparing the respective changes

in the price value of a basis point. Prospective effectiveness is

measured on a cumulative basis i.e. over the entire life of the hedge

relationship. The method of calculating hedge ineffectiveness is the

hypothetical derivative method. Retrospective effectiveness is assessed

by comparing the actual movements in the fair value of the cash flows

and actual movements in the fair value of the hedged cash flows from

the interest rate swap over the life to date of the hedging relationship.

Exchange rate contracts in cash flow hedge relationships hedge future

foreign currency cash inflow and outflows; mainly principal and interest

on foreign currency loans.

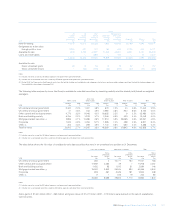

For fair value hedge relationships of interest rate risk, the hedged items

are typically large corporate fixed-rate loans, fixed-rate finance leases,

fixed-rate medium-term notes or preference shares classified as debt.

As at 31 December 2008 fixed rate financial assets of £42.5 billion and

fixed rate financial liabilities of £46.4 billion were hedged by interest rate

swaps in fair value hedge relationships.

The initial and ongoing prospective effectiveness of fair value hedge

relationships is assessed on a cumulative basis by comparing

movements in the fair value of the hedged item attributable to the

hedged risk with changes in the fair value of the hedging interest rate

swap or by comparing the respective changes in the price value of a

basis point. Retrospective effectiveness is assessed by comparing the

actual movements in the fair value of the hedged items attributable to

the hedged risk with actual movements in the fair value of the hedging

derivative over the life to date of the hedging relationship.