RBS 2008 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

111RBS Group Annual Report and Accounts 2008

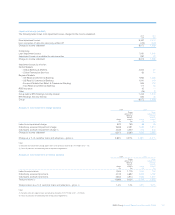

The Group is exposed to the following non-traded risks:

Interest Rate Risk in the Banking Book (IRRBB) represents exposures

to instruments whose values vary with the level or volatility of interest

rates. These instruments include, but are not limited to, loans, debt

securities, equity shares, deposits, certificates of deposits, and other

debt securities issued, loan capital and derivatives. Hedging

instruments used to mitigate these risks include related derivatives such

as options, futures, forwards and swaps. Interest rate risk arises from

the Group’s non-trading activities in four principal forms:

•Repricing risk – arises from differences in the repricing terms of the

Group’s assets and liabilities.

•Optionality – arises where a customer has an option to exit a deal

early.

•Basis risk – arises, for example, where one month LIBOR is used to

fund base rate assets.

•Yield curve risk – arises as a result of non-parallel changes in the

yield curve.

From an economic perspective, it is the Group’s policy to minimise the

sensitivity to changes in interest rates in its retail and commercial

businesses and, where interest rate risk is retained, to ensure that

appropriate resources, measures and limits are applied.

Non-trading interest rate risk is calculated in each business on the basis

of establishing the repricing behaviour of each asset, liability and off-

balance sheet product. For many retail and commercial products, the

actual interest rate repricing characteristics differ from the contractual

repricing. In most cases, the repricing maturity is determined by the

market interest rate that most closely fits the historical behaviour of the

product interest rate. For non-interest bearing current accounts, the

repricing maturity is determined by the stability of the portfolio. The

repricing maturities used are approved by Group Treasury and

divisional asset and liability committees at least annually. Key

conventions are reviewed annually by GALCO.

A static maturity gap report is produced as at the month-end for each

business, in each functional currency based on the behavioural

repricing for each product. It is Group policy to include in the gap

report, non-financial assets and liabilities, mainly property, plant and

equipment and the Group’s capital and reserves, spread over medium

and longer term maturities. The report includes hedge transactions,

principally derivatives.

Any residual non-trading interest rate exposures are controlled by

limiting repricing mismatches in the individual business balance sheets.

Potential exposures to interest rate movements in the medium to long-

term are measured and controlled using a version of the same VaR

methodology that is used for the Group’s trading portfolios. Net accrual

income exposures are measured and controlled in terms of sensitivity

over time to movements in interest rates.

Risk is managed within VaR limits approved by GALCO, through the

execution of cash and derivative instruments (see Note 13 on the

accounts, on page 214). Execution of the hedging is carried out by the

relevant division through the Group`s treasury functions. The residual

risk position is reported to divisional asset and liability committees,

GALCO and the Board.

Foreign Exchange Risk in the Banking Book (FXRBB) represents

exposures to changes in the values of current holdings and future

cashflows denominated in other currencies. Hedging instruments used

to mitigate these risks include foreign currency options, currency swaps,

futures, forwards and deposits. Foreign exchange risk results from the

Group’s investments in overseas subsidiaries, associates and branches

in three principal forms:

(i) Structural foreign currency exposures that arise from net investment

in overseas subsidiaries, associates and branches;

(ii) Transactional/commercial foreign currency exposures that arise from

mismatches in the currency balance sheet; and

(iii) Foreign currency profit streams.

Equity Risk in the Banking Book (ERBB) is defined as the potential

variation in the Group’s non-trading income and reserves arising from

changes in equity prices/income. This risk may crystallise during the

course of normal business activities or in stressed market conditions.

Equity positions in the Group’s banking book are retained to achieve

strategic objectives, support venture capital transactions or in respect of

restructuring arrangements. From an economic perspective, it is the

Group’s policy to ensure that equity exposures in the banking book are

identified, monitored and controlled, with the aim of maximising their

potential strategic or business value.

The commercial decision to invest in equity holdings is taken by GEMC,

GCC or an appropriate sub-committee within delegated authority.

Investments of a strategic nature are referred to GEMC for approval;

those involving the purchase or sale by the Group or subsidiary

companies also require Board approval, after consideration by GEMC.

Treasury (audited)

The Group’s treasury activities include its money market business and

the management of internal funds flow within the Group’s businesses.

In addition, this includes GBM trading portfolio assets that have been

reclassified to available-for-sale. Money market portfolios include cash

instruments (principally debt securities, loans and deposits) and related

hedging derivatives. VaR for the Group’s treasury portfolios, which

relates mainly to interest rate risk including credit spreads, was £52.0

million at 31 December 2008 (2007 – £5.5 million). During the year

the maximum VaR was £52.0 million (2007 – £6.4 million), the minimum

£4.8 million (2007 – £1.3 million) and the average £8.3 million

(2007 – £3.7 million).