RBS 2008 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

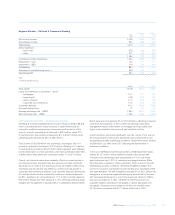

61RBS Group Annual Report and Accounts 2008

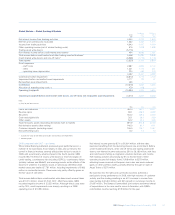

Regional Markets – Europe & Middle East Retail & Commercial Banking

Pro forma Statutory

2008 2007 2007

£m £m £m

Net interest income 1,152 1,066 1,014

Net fees and commissions 320 265 219

Other non-interest income 46 107 113

Non-interest income 366 372 332

Total income 1,518 1,438 1,346

Direct expenses

– staff costs 404 330 307

– other 159 173 152

563 503 459

Contribution before impairment 955 935 887

Impairment 526 136 118

Contribution 429 799 769

Allocation of manufacturing costs (1) 359 336 —

Operating profit 70 463 769

Note:

(1) Only for pro forma results.

£bn £bn £bn

Total assets 66.4 56.1 56.1

Loans and advances to customers – gross

– mortgages 24.6 18.3 18.3

– corporate 33.4 25.3 25.3

– other 3.7 4.2 4.2

Customer deposits 25.0 22.3 22.3

Non-performing loans 3.3 0.7 0.7

2008 compared with 2007 – pro forma

The significant deterioration in global and local market conditions has

impacted the main Europe & Middle East markets, with operating profit

falling to £70 million, 85% lower than in 2007. The main driver of this

reduction has been an increase of £390 million in impairments, albeit

from a low base, reflecting deterioration in credit quality particularly in

the property and construction sectors, as economic conditions have

slowed. Operating profit excluding impairment losses held steady at

£596 million.

Total income was up £80 million, 6% to £1,518 million benefiting from

movements in exchange rates. Adjusting for this, income declined by

5%. While average loans and deposits grew by 25% and 13%

respectively net interest margin reduced by 21bps in the year to 2.02%,

impacted primarily by higher funding costs and the effect of

discontinued businesses. Direct expenses were up 12% to £563 million.

At constant exchange rates direct expenses were flat reflecting the

benefit of cost saving initiatives. Impairment losses rose to £526 million

from £136 million reflecting the economic environment.

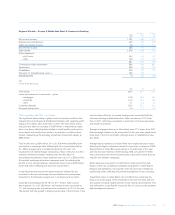

In sterling terms the results have been materially affected by the

movement in the euro exchange rate and references to percentage

movement in the following analysis are in constant currency terms.

Ulster Bank operating profit fell 76% to £117 million. Total income

decreased by 2% to £1,269 million; net interest income increased by

1%, with average loans and advances to customers up 12% in the year.

The benefit from the growth in lending, particularly in the first half of the

year has been offset by increased funding costs associated with the

wholesale funding market dislocation. Other income was 12% lower

than in 2007, reflecting a slowdown in particular in the bancassurance

and wealth businesses.

Average mortgage balances in Ulster Bank were 11% higher than 2007.

New mortgage volumes in the second half of the year were significantly

lower than in the first six months, although levels of redemptions have

also fallen.

Average deposit balances in Ulster Bank were largely flat year-on-year

reflecting the highly competitive market for resources in Ireland in 2008.

Deposit flows in Ulster Bank were strong in the latter part of the year

and into the early months of 2009. During 2008, we opened 119,000

new current accounts driven by particularly successful current account

switcher and student campaigns.

Direct expenses rose by 8% to £432 million, reflecting the full year

impact of the now completed investment programme in Ulster Bank’s

footprint and operations. Cost growth in the second half of 2008 was

significantly lower, reflecting disciplined management of the cost base.

Impairment losses in Ulster Bank rose to £394 million, reflecting the

impact on credit quality of the slowdown in the Irish economy, with the

final quarter showing notable decline in both activity and sentiment. This

was reflected in a significantly increased flow of cases into the problem

debt management process.