RBS 2008 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

123

RBS Group Annual Report and Accounts 2008

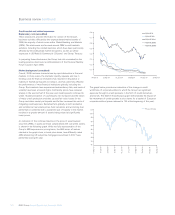

The first quarter of 2008 saw a further credit and liquidity shortages

experienced during 2007, culminating in the collapse of Bear Stearns in

March. The centre of the credit issues remained the ABS market with

worsening US economic data supporting higher levels of default

expectation in the property market. However, these default expectations

started to go beyond the sub-prime market with Alt A and other non-

conforming classes of loans particularly seeing significant price

deterioration. In addition, wider economic concerns led to heavy fair

value losses in the commercial mortgage backed securities (CMBS)

market, in corporate debt and in leveraged loan exposures. Following

this tightening of conditions, the Group incurred significant losses in

March and took steps in April to materially strengthen its capital base

through a £12 billion rights issue which was completed in June.

During the second quarter ABS prices initially rallied and steadied,

however towards the end of the quarter a negative house price trend in

the UK became clear, and in the US, market reaction to sub-prime

mortgages extended to prime and near prime lending. Corporate credit

spreads followed a similar pattern reacting to rising oil prices,

inflationary pressures and continuing high LIBOR despite base rate cuts

to 5% in April.

Credit spreads continued to widen across the market through the third

quarter and liquidity levels reduced further, resulting in pressure on

banks and economies worldwide. This culminated in the demise of

Lehman Brothers in September and further market consolidation and

global state intervention to provide support to the banking sector.

During the fourth quarter there was a continued lack of confidence in

the inter-bank market, with demand for stable investments resulting in

US treasuries reaching negative spreads. Corporate and ABS prices fell

further particularly in the last two months of the year increasing

pressure on banks’ capital positions. The Group moved to strengthen its

capital position through an open offer to raise £15 billion, underwritten

by the UK government. The year concluded with S&P downgrading the

credit ratings of eleven global banks, including the Group.

Asset-backed exposures

Significant risk concentrations (audited)

The Group’s credit markets activities gives rise to risk concentrations

that have been particularly affected by the market turmoil experienced

since the second half of 2007. The Group structures, originates,

distributes and trades debt in the form of loan, bond and derivative

instruments in all major currencies and debt capital markets in North

America, Western Europe, Asia and major emerging markets.

During 2008, certain assets identified as being high risk were also

transferred to a centrally managed asset unit, set up to provide specific

management of this portfolio of higher risk assets. Transferred assets

are predominantly ABS and associated protection purchased from

monoline insurers and other counterparties.

The tables below summarise the net exposures and balance sheet

carrying values of these securities by measurement classification and

references to sections with further information on specific products.

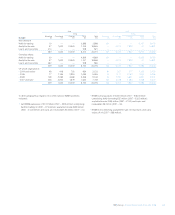

Held-for-trading Available-for-sale Loans and receivables Designated at fair value All ABS

2008 2007 2008 2007 2008 2007 2008 2007 2008 2007

Net exposure(1) £m £m £m £m £m £m £m £m £m £m

RMBS 24,462 35,105 44,450 27,875 2,578 5182 90 71,672 63,075

CMBS 1,178 2,749 918 977 1,437 626 13 47 3,546 4,399

CDOs/CLOs 2,463 7,288 2,538 2,174 1,282 ——23 6,283 9,485

Other ABS 195 3,479 6,572 5,579 3,621 72 40 186 10,428 9,316

Total 28,298 48,621 54,478 36,605 8,918 703 235 346 91,929 86,275

Carrying value(2)

RMBS 27,849 37,280 44,791 27,880 2,618 5182 90 75,440 65,255

CMBS 2,751 3,916 1,126 976 1,437 626 13 37 5,327 5,555

CDOs/CLOs 7,774 15,477 9,579 2,173 1,284 ——26 18,637 17,676

Other ABS 1,505 5,758 6,572 5,579 3,621 72 41 186 11,739 11,595

Total 39,879 62,431 62,068 36,608 8,960 703 236 339 111,143 100,081

Notes:

(1) Net exposure is carrying value after taking account of hedge protection purchased from monolines and other counterparties but excludes the effect of counterparty credit valuation adjustment.

The protection provides credit protection against the notional and interest cash flows due to the holders of debt instruments in the event of default by the debt security counterparty. The value of

the protection is based on the underlying instrument being protected.

(2) Carrying value is the amount recorded on the balance sheet.

(3) Certain instruments have been reclassified from the held-for-trading category to loans and receivables or available-for-sale categories, as permitted by the amendment to IAS 39 issued in October

2008, therefore affecting comparability by measurement classification.