RBS 2008 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

93RBS Group Annual Report and Accounts 2008

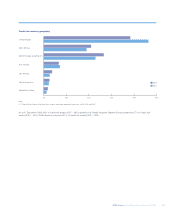

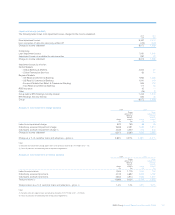

Corporate sectors (unaudited)

This section discusses the automotive, shipping, oil and gas sectors,

given their significance in the current market environment.

Automotive

The automotive sector exposure totals £14.5 billion, the majority falling

within GBM (£9.1 billion), RBS UK (£3.3 billion) and CFG (£1.3 billion).

The exposure is spread across the following segments and

geographies:

Credit book

Segment £bn %

Original equipment manufacturer/commercial vehicles 3.3 23

Captive finance companies 1.1 8

Component suppliers 2.4 16

Retailers/services 5.1 35

Rental 2.6 18

Total 14.5 100

Credit book

Domicile £bn %

Americas 4.0 28

Central Eastern Europe

Middle East and Africa 1.1 7

UK 4.2 29

Western Europe 4.3 30

Asia 0.9 6

Total 14.5 100

The automotive sector faces numerous challenges with a heavy reliance

on discretionary consumer spending, high leverage, volatile input prices

and an ongoing pressure to reduce fuel emissions resulting in a shift to

smaller cars and overseas production. The Group has maintained a

cautious approach to this sector and focus on the largest, most

diversified and financially strong counterparties with a wide product

offering. Notwithstanding this approach, due to the scale of the

downturn in this sector the Group can expect further pressure to be

seen across the portfolio. Of particular concern are exposures to the

captive finance companies where credit impaired limits total £1.4 billion.

The Group continues to seek ongoing limit reductions and improved

security.

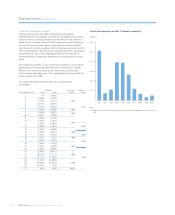

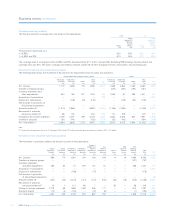

Shipping

The shipping exposure is £16.6 billion and is almost entirely within

GBM. The portfolio is divided across the following sectors:

Credit book

Sector £bn %

Dry bulk 4.8 29

Tankers 6.3 38

Container 1.6 10

Gas/offshore 2.3 14

Other 1.6 9

Total 16.6 100

The majority of the exposures are strong relationships with loans

structured to capture direct vessel cash flows, secured on the vessels

themselves with the benefit of full security over the asset and all related

cash flows. The Group’s approach to the sector recognises the cyclical

nature of shipping with a focus on experienced independent owners

with strong liquidity; customer deposits across the portfolio total £5

billion. Assets financed are non-specialist dry bulk, double hulled

tankers and containers.

Following an unprecedented rise in ship values over recent years there

has been a material correction since mid 2008 with the dry bulk index

falling by c.90% which may affect owners’ ability to meet collateral calls.

Combined with record ship deliveries for 2009-10 the Group has seen a

significant decline in asset values. The Group’s exposure to new build

assets is significant with commitments relating to 236 vessels in the dry

bulk and tanker segment.

The Group currently has £0.5 billion of limits to clients on watch list, but

the portfolio comprises modern assets (86% of exposures are secured

on vessels built since 2000), which exhibit, for the most part, good cash

flow and liquidity.

Oil and gas

The Group’s exposure to this sector totals £24.0 billion across the

following sectors and geographies:

Credit book

Sector £bn %

Vertically integrate/exploration and production 9.5 40

Midstream 5.0 21

Refining and marketing 4.6 19

Oilfield services 4.9 20

Total 24.0 100

Credit book

Domicile £bn %

Americas 10.6 44

Western Europe 7.6 32

CEEMEA 4.6 19

Asia Pacific 1.2 5

Total 24.0 100

ABN AMRO and RBS have a number of common clients in this sector,

and the Group is working to reduce exposures back within Group

concentration limits, primarily in relation to investment grade, vertically

integrated counterparties and several of the larger, global exploration

and production companies. The Group’s exposures to exploration and

production companies are principally secured borrowing base facilities

referenced to conservative forward looking oil price assumptions that

are adjusted on a regular basis. Unsecured exposures are primarily to

oil majors and state owned entities.