RBS 2008 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

RBS Group Annual Report and Accounts 200862

Business review continued

In January 2009, Ulster Bank announced its intention to adopt a single

brand strategy under the Ulster Bank brand. This will see the merger of

the operations of Ulster Bank and First Active in the Republic of Ireland

(‘RI’) by the end of 2009. This action is being taken to strengthen the

Ulster Bank Group franchise by positioning it to deal with the prevailing

local and global market conditions. A number of cost management

initiatives have also commenced across the business.

Ulster Bank has launched a series of initiatives to support its customers

in this difficult economic period. We announced in February 2009 that

we will be making significant funds available to the Northern Ireland

(‘NI’) SME market. A similar announcement will be made in the coming

weeks regarding the RI SME market. Ulster Bank has also indicated that

it is adopting the RBS Group pledge regarding certainty of overdraft

limits for this sector.

The Momentum and Secure Step mortgages have been launched in NI

and RI respectively to support First Time Buyers and the Bank has

confirmed its pledge of a six-month moratorium to mortgage customers

facing potential repossession. In support of our retail customers across

the island of Ireland, the Group’s MoneySense programme is being

rolled out, with trained advisers being introduced to all Ulster Bank

branches.

Outside Ireland, Europe & Middle East Retail & Commercial Banking

continued to trade satisfactorily, although our markets in the United Arab

Emirates, Romania and Kazakhstan have also experienced a marked

slowdown in the past year. In UAE, where we are a market leader in

credit cards with over 430,000 cards in issue, credit card revenue

increased 22% in the year.

The sale of the European Consumer Finance business to Santander

was completed on 1st July 2008, while the Imagine business in Spain

was sold to Bank of America in the second half of 2008. The former

ABN retail business in Russia was also closed during the year.

Strategic review

Ulster Bank, which remains a core part of the Group’s global banking

operations, has a strong franchise in both Northern Ireland, where it is

the leading bank, and the Republic of Ireland where it is overall the

third-positioned bank. It has the product and distribution capability to

grow profitably and well in normal market conditions. However, the

economic difficulties that the Irish markets currently face are expected

to persist for some time. Ulster Bank has been pro-active in responding

to these market conditions through a programme of initiatives. The

business plans to manage its balance sheet over the medium term, with

particular focus on reducing risk concentrations as market conditions

allow, whilst increasing and diversifying its customer deposit base.

The E&ME Retail and Commercial franchises outside of Ireland lack

scale and breadth. They would require a very significant investment of

capital and management resource to be able to achieve levels of

shareholder return equivalent to those possible from more established

core franchises in the Group. The Retail and Commercial businesses in

E&ME outside of Ireland will be transferred to the non-core division. We

have commenced a review to consider future options for these

businesses, including options for sale.

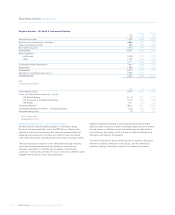

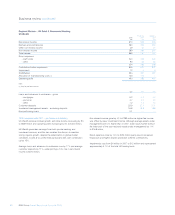

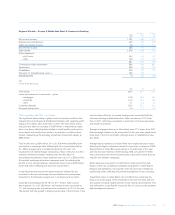

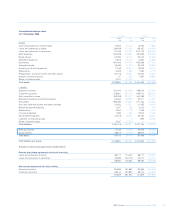

2008 compared with 2007 – statutory

Total income was up £172 million, 13% at £1,518 million benefiting from

the full year of the ABN AMRO businesses and movements in exchange

rates. Direct expenses rose by £104 million, 23%.

Impairment losses rose sharply to £526 million from £118 million in

2007 leading to a decline in contribution of £340 million to £429 million.

Contribution before impairment losses increased by £68 million.