RBS 2008 Annual Report Download - page 131

Download and view the complete annual report

Please find page 131 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

Business review continued

RBS Group Annual Report and Accounts 2008130

The Group’s largest concentration of RMBS assets relate to a portfolio

of US agency asset backed securities comprising mainly current year

vintage positions of £33.5 billion at 31 December 2008 (2007: £26.0

billion). Due to the US government backing explicit or implicit in these

securities, the counterparty credit risk exposure is low. The losses

arising from the movements in fair value recorded for these assets were

comparatively lower than other RMBS. Financial markets and economic

conditions have been extremely difficult in the US throughout 2008,

particularly in the last quarter. Credit conditions have deteriorated and

financial markets have experienced widespread illiquidity and elevated

levels of volatility due to forced de-leveraging. Transaction activity in the

securities portfolio has been reduced due to general market illiquidity.

Residential mortgages have been affected by the stress that consumers

experienced from depreciating house prices, rising unemployment and

tighter credit conditions, resulting in higher levels of delinquencies and

foreclosures. In particular, the deteriorating economy and financial

markets have negatively impacted the valuation, liquidity, and credit

quality of private-label securities.

Citizens maintains an available-for-sale investment securities portfolio to

provide high-quality collateral to provide a liquidity buffer and to

enhance earnings. The size of the portfolio has been relatively stable

through 2008, but both the absolute and relative size (% of earning

assets) declined in 2006-2007. The portfolio comprises high credit

quality mortgage-backed securities, to ensure both pledgeability and

liquidity. The U.S. Government guarantees on MBS, whether explicit or

implicit, put most of the portfolio in a secure credit position. The non-

agency MBS holdings derive credit support in two ways. Firstly, there is

senior and subordinated structuring, and Citizens hold only the most

senior tranches. Secondly, there is high quality supporting loan

collateral. The collateral quality is evidenced (a) by the vintages, with

82% issued in 2005 and earlier, (b) by the borrower’s weighted loan to

value (LTV) ratio of 65%, and (c) by the borrower’s weighted-average

FICO score of 734.

£7.6 billion (2007 – £6.0 billion) of the RMBS exposure consists of

available-for-sale portfolio of European RMBS in Group Treasury,

referencing primarily Dutch and Spanish government-backed loans, and

accordingly the quality of these assets has held up relative to other

RMBS types. A further £10.0 billion (2007 – £7.8 billion) European

RMBS comprised covered mortgage bonds.

The Group has other portfolios of RMBS from secondary trading

activities, warehoused positions previously acquired with the intention of

further securitisation and a portfolio of assets from the unwinding of a

securities arbitrage conduit. This conduit was established to benefit

from the margin between the assets purchased and the notes issued.

The majority of these held-for-trading RMBS have been grouped

together for management purposes.

Some of these assets (£7.0 billion) were reclassified from held-for-

trading category to the loans and receivables (£1.8 billion) and

available-for-sale categories during the year (£5.2 billion).

Overall, the Group has recognised significant fair value losses on RMBS

assets during the year due to reduced market liquidity and deteriorating

credit ratings of these assets. The Group has reduced its exposure to

RMBS predominantly through fair value hedges and asset sales during

the year. These decreases were partially offset by the weakening of

sterling relative to the US dollar and euro.

Commercial mortgage-backed securities (audited)

Commercial mortgages backed securities (CMBS) are securities that

are secured by mortgage loans on commercial land and buildings. The

securities are structured in the same way as an RMBS but typically the

underlying assets referenced will be of greater individual value. The

performance of the securities are highly dependent upon the sector of

commercial property referenced and the geographical region.

The Group accumulated CMBS for the purpose of securitisation and

secondary trading. The largest holding of CMBS arose as a result of the

Group’s purchase of senior tranches in mezzanine and high grade

CMBS structures from third parties. These securities are predominantly

hedged with monoline insurers. As a result, the Group’s risk is limited to

the counterparty credit risk exposure to the hedge. The Group also

holds CMBS arising from securitisations of European commercial

mortgages originated by the Group.

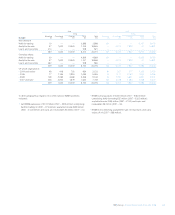

The following table shows the composition of the Groups holdings of CMBS portfolios.

2008 2007

US UK Europe ROW(1) Total US UK Europe ROW Total

£m £m £m £m £m £m £m £m £m £m

Office 435 938 402 — 1,775 599 534 ——1,133

Mixed use 32 106 1,048 45 1,231 — 73 192 — 265

Healthcare 805 143 ——948 1,210 ———1,210

Retail 295 43 17 48 403 398 13 ——411

Industry 24 13 81 — 118 61 ——100 161

Multi-family 40 — 49 — 89 48 ———48

Leisure — 76 ——76 —————

Hotel 40 35 ——75 36 ———36

Other 474 41 49 48 612 932 530 765 64 2,291

2,145 1,395 1,646 141 5,327 3,284 1,150 957 164 5,555

Note;

(1) Rest of the World.