RBS 2008 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

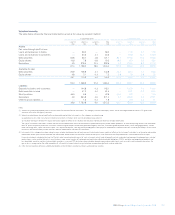

199RBS Group Annual Report and Accounts 2008

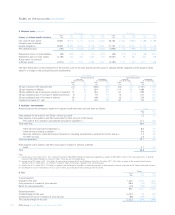

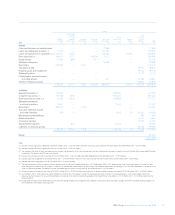

Valuation of financial instruments

Control environment

The Group’s control environment for the determination of the fair value

of financial instruments has been designed to ensure there are

formalised review protocols for independent review and validation of fair

values separate from those businesses entering into the transactions.

This includes specific controls to ensure consistent pricing policies and

procedures, incorporating disciplined price verification for both

proprietary and counterparty risk trades. The Group ensures special

attention is given to bespoke transactions, structured products, illiquid

products, and other assets which are difficult to price.

The business entering into the transaction is responsible for the initial

determination and recording of the fair value of the transaction. There

are daily controls over the profit or loss recorded by trading and

treasury front office traders.

A key element of the control environment, segregated from the

recording of the transaction’s valuation, is the independent price

verification (IPV) process. Valuations are first calculated by the business

which entered into the transaction. Such valuations may be direct

prices, or may be derived using a model and variable model inputs.

These valuations are reviewed, and if necessary amended, by the IPV

process. This process involves a team, independent of those trading the

financial instruments, reviewing valuations in the light of available

pricing evidence. IPV is performed at a frequency to match the

availability of independent data, and the size of the Group’s exposure.

For liquid instruments the process is performed daily. The minimum

frequency of review in GBM is monthly for regulatory trading book

positions, and six monthly for regulatory banking book positions. The

IPV control includes formalised reporting and escalation of any

valuation differences in breach of defined thresholds. In addition, within

GBM, there is a dedicated team (the Global Pricing Unit) which

determines IPV policy, monitors adherence to policy, and performs

additional independent review on highly subjective valuation issues.

In GBM, when models are used to value products, those models are

subject to a review process which requires different levels of model

documentation, testing and review, depending on the complexity of the

model and the size of the Group’s exposure. A key element of the

control environment over model use in GBM is a review committee

which comprises of valuations experts from several functions within

GBM. The committee sets the policy for model documentation, testing

and review, and prioritises models with significant exposure for review

by the Group’s quantitative research centre. This centre, which is

independent of the trading businesses, assesses the appropriateness

of the application of the model to the product, the mathematical

robustness of the model, and (where appropriate), considers alternative

modelling approaches.

GBM also maintains a valuation control committee that meets formally

on a monthly basis to discuss and review escalated items and to

consider highly complex and subjective valuation matters. The

committee includes valuation specialists representing several

independent review functions (including market risk, quantitative

research and finance) and senior members of the Group’s front office

trading businesses.

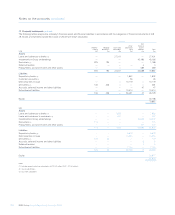

Certain financial instruments have become more difficult and subjective

to value and have therefore been transferred to a centrally managed

asset unit, to separate them from business as usual activities and to

allow dedicated focus on the management and valuation of the

exposures. The unit has a valuation committee comprising senior

representatives of the trading function, risk management and GBM

Global Pricing Unit which meets regularly and is responsible for

monitoring, assessing and enhancing the adequacy of the valuation

techniques being adopted for these instruments.

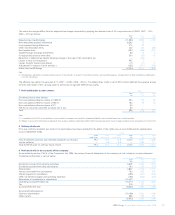

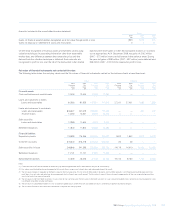

Valuation techniques

The Group uses a number of methodologies to determine the fair values

of financial instruments for which observable prices in active markets

for identical instruments are not available. These techniques include:

relative value methodologies based on observable prices for similar

instruments; present value approaches where future cash flows from the

asset or liability are estimated and then discounted using a risk-adjusted

interest rate; option pricing models (such as Black-Scholes or binomial

option pricing models) and simulation models such as Monte-Carlo.

The principal inputs to these valuation techniques are listed below.

Values between and beyond available data points are obtained by

interpolation and extrapolation. When utilising valuation techniques, the

fair value can be significantly affected by the choice of valuation model

and underlying assumptions made concerning factors such as the

amounts and timing of cash flows, discount rates and credit risk.

•Bond prices – quoted prices are generally available for government

bonds, certain corporate securities and some mortgage-related

products.

•Credit spreads – where available, these are derived from prices of

CDS or other credit based instruments, such as debt securities. For

others, credit spreads are obtained from pricing services.

•Interest rates – these are principally benchmark interest rates such as

the London Inter-Bank Offered Rate (LIBOR) and quoted interest

rates in the swap, bond and futures markets.

•Foreign currency exchange rates – there are observable markets both

for spot and forward contracts and futures in the world’s major

currencies.