RBS 2008 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

Notes on the accounts continued

RBS Group Annual Report and Accounts 2008204

11 Financial instruments (continued)

tenor and nature of the trades that have been observed. This method is

most frequently used for US and UK RMBS. The RMBS of Dutch and

Spanish originated mortgages guaranteed by those governments are

valued using the credit spreads of the respective government debt and

certain assumptions made by the Group, or based on observable prices

from Bloomberg or consensus pricing services.

Where there is an absence of trading activity, models are used.

The Group primarily uses an industry standard model to project the

expected future cash flows to be received from the underlying

mortgages and to forecast how these cash flows will be distributed to

the various holders of the RMBS. This model utilises data provided by

the servicer of the underlying mortgage portfolio, layering on

assumptions for mortgage prepayments, probability of default,

expected losses, and yield. The Group uses data from third-party

sources to calibrate its assumptions, including pricing information from

third party pricing services, independent research, broker quotes, and

other independent sources. An assessment is made of third-party data

source to determine its applicability and reliability. The Group adjusts

the model price with a liquidity premium to reflect the price that the

instrument could be traded at in the market and may also make

adjustments for model deficiencies.

The weighted average of the key significant inputs utilised in valuing US

level 3 RMBS positions are shown in the table below.

The fair value of securities within each class of asset changes on a

broadly consistent basis in response to changes in given market factors.

However, the extent of the change, and therefore the range of

reasonably possible alternative assumptions, may be either more or less

pronounced, depending on the particular terms and circumstances of

the individual security. Through most of 2008, while default rates on

sub-prime mortgages were on the rise, there was less transparency and

historical data to predict future defaults on both Alt-A and prime

securities. As such, the Group felt that probability of default was the

least transparent input into Alt-A and prime RMBS modelled valuations

throughout 2008 (and most sensitive to variations). The Group believes

that a range of 500 basis points greater than and 500 basis points less

than the weighted average constant default rate, and a range of 200

basis points greater than and 200 basis points less than the weighted

average constant default rate represents a reasonably possible set of

acceptable pricing alternatives for Alt-A and prime RMBS, respectively.

These assumptions consider the inherently risky nature of Alt-A over

prime securities, as well as declining economic conditions leading to an

increased likelihood of default at year-end. While other key inputs may

possess characteristics of unobservability in both Alt-A and prime

modelled valuations, the effect of utilising reasonably possible

alternatives for these respective inputs would have an immaterial effect

on the overall valuation. Using these reasonably possible alternative

assumptions the fair value of RMBS of £0.5 billion would be £90 million

lower or £40 million higher.

Commercial mortgage backed securities

CMBS is valued using an industry standard model and the inputs, where

possible, are corroborated using observable market data.

For senior CMBS and subordinated tranches, the Group determined

that the most sensitive input to reasonably possible alternatives valuation

is probability of default and yield respectively. Using reasonably possible

alternative assumptions for these inputs, the fair value of CMBS of

£0.6 billion would be £30 million lower or £30 million higher.

Collateralised debt obligations

CDOs purchased from third parties are valued using independent, third-

party quotes or independent lead manager indicative prices. For super

senior CDOs which have been originated by the Group no specific third-

party information is available. The valuation of these super senior CDOs

therefore takes into consideration outputs from a proprietary model,

market data and appropriate valuation adjustments.

The Group’s proprietary model calculates the expected cashflows from

the underlying mortgages using assumptions, derived from publicly

available data on future macroeconomic conditions (including house

price appreciation and depreciation) and on defaults and delinquencies

on these underlying mortgages. The model used by the Group comprises

an econometric loan-level model which provides the input to an industry

standard ABS model, the output of which feeds a proprietary model

generating expected cashflows which are discounted using a risk

adjusted rate.

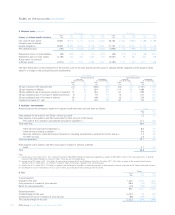

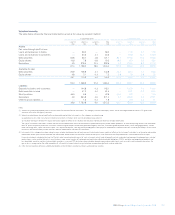

Weighted–average inputs

Non-agency

2008 prime RMBS Alt-A RMBS

Yield 11.02% 20.69%

Probability of default 3.00 CDR(1) 40.00 CDR(1)

Loss severity 45.00%(2) 52.25%(2)

Prepayment 12.67 CPR 10.65 CPR

Notes:

(1) Constant default rate or probability of default.

(2) Constant prepayment rate.