RBS 2008 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

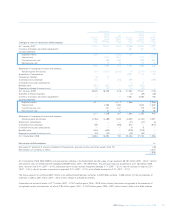

Accounting policies continued

RBS Group Annual Report and Accounts 2008188

Accounting developments

International Financial Reporting Standards

The International Accounting Standards Board issued a revised IAS 23

‘Borrowing Costs’ in March 2007. Entities are required to capitalise

borrowing costs attributable to the development or construction of

intangible assets or property plant or equipment. The standard is

effective for accounting periods beginning on or after 1 January 2009

and is not expected to have a material effect on the Group or company.

The IASB issued a revised IAS 1 ‘Presentation of Financial Statements’

in September 2007 effective for accounting periods beginning on or

after 1 January 2009. The amendments to the presentation requirements

for financial statements are not expected to have a material effect on the

Group or company.

The IASB published a revised IFRS 3 ‘Business Combinations’ and

related revisions to IAS 27 ‘Consolidated and Separate Financial

Statements’ following the completion in January 2008 of its project on

the acquisition and disposal of subsidiaries. The standards improve

convergence with US GAAP and provide new guidance on accounting

for changes in interests in subsidiaries. The cost of an acquisition will

comprise only consideration paid to vendors for equity; other costs will

be expensed immediately. Groups will only account for goodwill on

acquisition of a subsidiary; subsequent changes in interest will be

recognised in equity and only on a loss of control will there be a profit

or loss on disposal to be recognised in income. The changes are

effective for accounting periods beginning on or after 1 July 2009 but

both standards may be adopted together for accounting periods

beginning on or after 1 July 2007. These changes will affect the Group’s

accounting for future acquisitions and disposals of subsidiaries.

The IASB published revisions to IAS 32 ‘Financial Instruments:

Presentation’ and consequential revisions to other standards in February

2008 to improve the accounting for and disclosure of puttable financial

instruments. The revisions are effective for accounting periods

beginning on or after 1 January 2009 but together they may be adopted

earlier. They are not expected to have a material affect on the Group or

the company.

The IASB issued an amendment, 'Vesting Conditions and Cancellations',

to IFRS 2 'Share-based Payment' in January 2008 that will change the

accounting for share awards that have non-vesting conditions. The fair

value of these awards does not currently take account of the effect of

non-vesting conditions and where such conditions are not subsequently

met, costs recognised up to the date of cancellation are reversed. The

amendment requires costs not recognised up to the date of

cancellation to be recognised immediately. The amendment is effective

for accounting periods beginning on or after 1 January 2009. The Group

estimates that adoption will cause a restatement of 2008 results,

reducing profit by £110 million with no material affect on earlier periods.

There is not expected to be a material effect on the company.

The IASB issued amendments to a number of standards in May 2008 as

part of its annual improvements project. The amendments are effective

for accounting periods beginning on or after 1 January 2009 and are

not expected to have a material effect on the Group or company.

Also in May 2008, the IASB issued amendments to IFRS 1 ‘First-time

Adoption of International Financial Reporting Standards’ and IAS 27

‘Consolidated and Separate Financial Statements’ that change the

investor's accounting for the cost of an investment in a subsidiary, jointly

controlled entity or associate. It does not affect the consolidated

accounts but may prospectively affect the company’s accounting and

presentation of receipts of dividends from such entities.

The IASB issued an amendment to IAS 39 in July 2008 to clarify the

IFRS stance on eligible hedged items. The amendment is effective for

accounting periods beginning on or after 1 January 2009 and is not

expected to have a material effect on the Group or the Bank.

The International Financial Reporting Interpretations Committee (IFRIC)

issued interpretation IFRIC 15 ‘Agreements for the Construction of Real

Estate’ in July 2008. This interpretation clarifies the accounting for

construction profits. It is applicable for accounting periods beginning on

or after 1 January 2009 and is not expected to have a material effect on

the Group or company.

The IFRIC issued interpretation IFRIC 16 ‘Hedges of a Net Investment in

a Foreign Operation’ in July 2008. The interpretation addresses the

nature of the hedged risk and the amount of the hedged item; where in

a group the hedging item could be held; and what amounts should be

reclassified from equity on the disposal of a foreign operation that had

been subject to hedging. The interpretation is effective for accounting

periods beginning on or after 1 October 2008 and is not expected to

have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 17 ‘Distributions of Non-Cash

Assets to Owners’ and the IASB made consequential amendments to

IFRS 5 'Non-Current Assets Held for Sale and Discontinued Operations'

in December 2008. The interpretation requires distributions to be

presented at fair value with any surplus or deficit to be recognised in

income. The amendment to IFRS 5 extends the definition of disposal

groups and discontinued operations to disposals by way of distribution.

The interpretation is effective for accounting periods beginning on or after

1 July 2009, to be adopted at the same time as IFRS 3 (revised 2008),

and is not expected to have a material effect on the Group or company.

The IFRIC issued interpretation IFRIC 18 ‘Transfers of Assets from

Customers’ in January 2009. The interpretation addresses the

accounting by suppliers that receive assets from customers, requiring

measurement at fair value. The interpretation is effective for assets from

customers received on or after 1 July 2009 and is not expected to have

a material effect on the Group or company.