RBS 2008 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2008 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

|

|

135

RBS Group Annual Report and Accounts 2008

The widening of credit spreads of corporate and financial institution

counterparties during the year contributed to a significant increase in

the level of CVA adjustments recorded across all counterparties

particularly monoline insurers and credit derivative product companies.

The monoline insurer CVA is calculated on a trade-by-trade basis,

and is derived using market observable monoline credit spreads. The

majority of the monoline CVA is taken against credit derivatives hedging

exposures to ABS. The CDPC CVA is calculated using a similar

approach. However, in the absence of market observable credit

spreads, the cost of hedging the counterparty risk is estimated by

analysing the underlying trades and the cost of hedging expected

default losses in excess of the capital available in each vehicle.

The CVA for all other counterparties, including those in respect of

derivatives with banks, is calculated either on a trade-by-trade basis,

reflecting the estimated cost of hedging the risk through credit

derivatives, or on a portfolio basis reflecting an estimate of the amount

a third party would charge to assume the risk.

Monoline insurers

The Group has purchased protection from monoline insurers, mainly

against specific ABS, CDOs and CLOs. Monoline insurers are entities

which specialise in providing credit protection against the notional and

interest cash flows due to the holders of debt instruments in the event of

default by the debt security counterparty. This protection is typically

held in the form of derivatives such as credit default swaps (CDS)

referencing the underlying exposures held by the Group.

During the year the market value of securities protected by monoline

insurers continued to decline as markets deteriorated. As the fair value

of the protected assets declined, the fair value of the CDS protection from

monoline insurers increased. As the monoline insurers had concentrated

their exposures to credit market risks, their perceived credit quality has

deteriorated as concerns increased regarding the ability of these

counterparties to meet their contractual obligations. This resulted in

increased levels of CVA being recorded on the protection asset.

The change in exposure during the year has been driven by the

increased value of purchased derivative protection and the

strengthening of the US dollar against sterling as significantly all of the

exposures are US dollar denominated. The combination of greater

exposure and widening credit spreads has increased the level of CVA

required. Towards the end of the year the Group reached settlement on

a group of contracts with one monoline counterparty, thereby reducing

the overall exposure.

The covered bonds comprise asset-backed securities issued by several

Spanish financial institutions. These securities benefit from additional

credit enhancement provided by the issuing institutions. The other major

asset types that increased since 2007 include other consumer loans by

£1.8 billion, leases by £0.5 billion and student loans by £0.2 billion.

These and other increases were driven by the weakening of sterling

against the US dollar and euro.

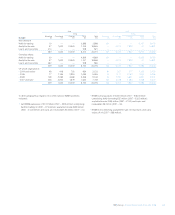

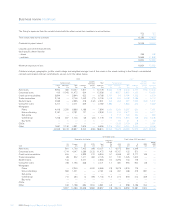

Other mortgage-related exposures (unaudited)

The Group’s whole loans and warehouse facilities collateralised by

mortgages are analysed below. These facilities primarily relate to UK

and European mortgages with US mortgages representing £260 million

of whole loans, of which more than 75% comprised prime mortgages.

2008 2007

Whole Warehouse Whole Warehouse

loans facilities loans facilities

£m £m £m £m

Prime 1,905 1,731 453 575

Commercial 1,262 409 2,200 900

Non-conforming 1,396 1019 57 1,445

Sub-prime 27 — 97 —

4,590 3,159 2,807 2,920

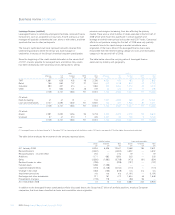

Counterparty valuation adjustments (audited)

Credit valuation adjustments

Credit valuation adjustments (CVAs) represent an estimate of the

adjustment to fair value that a market participant would make to

incorporate the credit risk inherent in counterparty derivative exposures.

During 2008, as credit spreads have widened, there has been a

significant increase in the CVA as set out in the table below.

2008 2007

£m £m

Monoline insurers 5,988 862

CDPCs 1,311 44

Other counterparties 1,738 263

Total CVA adjustments 9,037 1,169

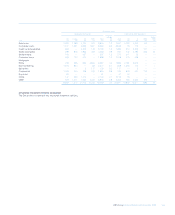

The tables below analyse the Group’s holdings of CDS with monoline counterparties.

2008 2007

£m £m

Gross exposure to monolines 11,581 3,409

Hedges with bank counterparties (789) —

Credit valuation adjustment (5,988) (862)

Net exposure to monolines 4,804 2,547