Bank of America 2014 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

98 Bank of America 2014

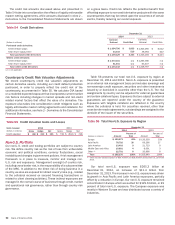

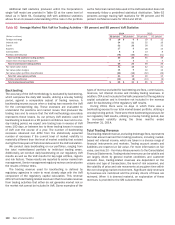

Global Markets Risk Management continually reviews,

evaluates and enhances our VaR model so that it reflects the

material risks in our trading portfolio. Changes to the VaR model

are reviewed and approved prior to implementation and any

material changes are reported to management through the

appropriate management committees.

Trading limits on quantitative risk measures, including VaR, are

monitored on a daily basis. These trading limits are independently

set by Global Markets Risk Management and reviewed on a regular

basis to ensure they remain relevant and within our overall risk

appetite for market risks. Trading limits are reviewed in the context

of market liquidity, volatility and strategic business priorities.

Trading limits are set at both a granular level to ensure extensive

coverage of risks as well as at aggregated portfolios to account

for correlations among risk factors. All trading limits are approved

at least annually and the MRC has given authority to the GM

subcommittee to approve changes to trading limits throughout the

year. Approved trading limits are stored and tracked in a centralized

limits management system. Trading limit excesses are

communicated to management for review. Certain quantitative

market risk measures and corresponding limits have been

identified as critical in the Corporation’s Risk Appetite Statement.

These risk appetite limits are monitored on a daily basis and are

approved at least annually by the ERC and the Board.

In periods of market stress, the GM subcommittee members

communicate daily to discuss losses, key risk positions and any

limit excesses. As a result of this process, the businesses may

selectively reduce risk.

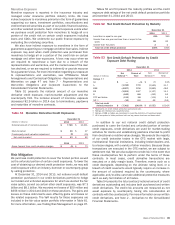

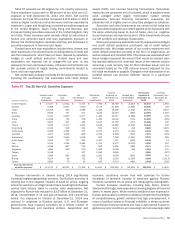

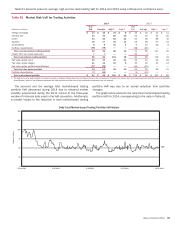

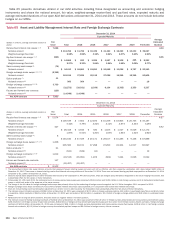

Market risk VaR for trading activities as presented in Table 61

differs from VaR used for regulatory capital calculations (regulatory

VaR). The VaR disclosed in Table 61 excludes both CVA, which are

adjustments to the mark-to-market value of our derivative

exposures to reflect the impact of the credit quality of

counterparties on our derivative assets, and the corresponding

hedges. Current regulatory standards require that regulatory VaR

only exclude CVA but include the corresponding hedges. The

holding period for regulatory VaR for capital calculations is 10 days,

while for the market risk VaR presented below, it is one day. Except

for the differences between regulatory and market risk VaR

regarding the inclusion of CVA hedges and the holding period, both

measures utilize the same process and methodology.

To provide visibility of market risks to which the Corporation is

exposed, Table 61 presents the total market-based trading

portfolio VaR which includes our total covered positions trading

portfolio and the impact from less liquid trading exposures.

Covered positions are defined by regulatory standards as trading

assets and liabilities, both on- and off-balance sheet, that meet a

defined set of specifications. These specifications identify the

most liquid trading positions which are intended to be held for a

short-term horizon and where the Corporation is able to hedge the

material risk elements in a two-way market. Positions in less liquid

markets, or where there are restrictions on the ability to trade the

positions, typically do not qualify as covered positions. Foreign

exchange and commodity positions are always considered covered

positions, except for structural foreign currency positions that we

choose to exclude with prior regulatory approval. Certain positions

related to our CVA and corresponding hedges are considered

covered positions; however, these are excluded from the VaR

results presented in Table 61. In addition, Table 61 presents our

fair value option portfolio, which includes the funded and unfunded

exposures for which we elect the fair value option, and their

corresponding hedges. The fair value option portfolio combined

with the total market-based trading portfolio VaR represents the

Corporation’s total market-based portfolio VaR. This population is

consistent with the risk appetite limits set by the ERC and the

Board.

The market risk across all business segments to which the

Corporation is exposed is included in the total market-based

portfolio VaR results. The majority of this portfolio is within the

Global Markets segment.