Bank of America 2014 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

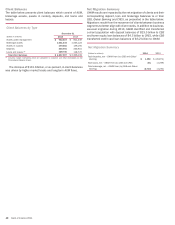

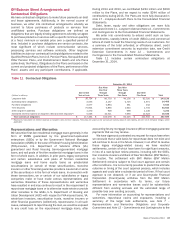

50 Bank of America 2014

Experience with Monoline Insurers

During 2014, we had limited loan-level representations and

warranties repurchase claims experience with the monoline

insurers due to settlements and ongoing litigation with a single

monoline insurer. For more information related to the monolines,

see Note 7 – Representations and Warranties Obligations and

Corporate Guarantees and Note 12 – Commitments and

Contingencies to the Consolidated Financial Statements.

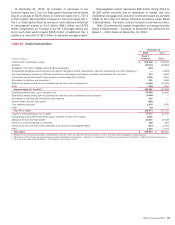

Estimated Range of Possible Loss

We currently estimate that the range of possible loss for

representations and warranties exposures could be up to $4 billion

over existing accruals at December 31, 2014. The estimated range

of possible loss reflects principally non-GSE exposures. It

represents a reasonably possible loss, but does not represent a

probable loss, and is based on currently available information,

significant judgment and a number of assumptions that are subject

to change.

For more information on the methodology used to estimate the

representations and warranties liability, the corresponding

estimated range of possible loss and the types of losses not

considered in such estimates, see Item 1A. Risk Factors of our

2014 Annual Report on Form 10-K and Note 7 – Representations

and Warranties Obligations and Corporate Guarantees to the

Consolidated Financial Statements and, for more information

related to the sensitivity of the assumptions used to estimate our

liability for obligations under representations and warranties, see

Complex Accounting Estimates – Representations and Warranties

Liability on page 110.

Department of Justice Settlement

On August 20, 2014, we reached a comprehensive settlement with

the DoJ and certain federal and state agencies (DoJ Settlement).

The DoJ Settlement included releases for securitization,

origination, sale and other specified conduct relating to RMBS and

collateralized debt obligations (CDOs), and an origination release

on specified populations of residential mortgage loans sold to

GSEs and private-label RMBS trusts. The DoJ Settlement resolved

certain actual and potential civil claims by the DoJ, the Securities

and Exchange Commission and State Attorneys General from six

states, the FHA and GNMA, as well as all pending RMBS claims

against Bank of America entities brought by the FDIC. For FHA-

insured loans originated on or after May 1, 2009, we also received

a release of origination liability for loans only if an insurance claim

had been submitted to the FHA prior to January 1, 2014. If a claim

had not been submitted by that date, we did not receive a release

and we may be exposed to losses on such loans. For more

information on FHA-insured loans originated on or before April 30,

2009, see Off-Balance Sheet Arrangements and Contractual

Obligations – National Mortgage Settlement on page 51.

As part of the DoJ Settlement, we paid civil monetary penalties

and compensatory remediation payments totaling $9.65 billion in

2014 and agreed to provide $7.0 billion worth of creditable

consumer relief activities primarily in the form of mortgage

modifications, including first-lien principal forgiveness and

forbearance modifications and second- and junior-lien

extinguishments, low- to moderate-income mortgage originations,

and community reinvestment and neighborhood stabilization

efforts, with initiatives focused on communities experiencing, or

at risk of, blight. In addition, we recorded $400 million of provision

for credit losses for additional costs associated with the consumer

relief portion of the settlement. Also, we will support the expansion

of available affordable rental housing. We have committed to

complete delivery of the consumer relief by no later than August

31, 2018. The consumer relief requirements are subject to

oversight by an independent monitor.

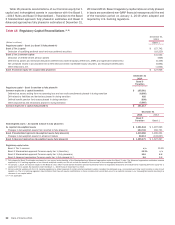

Servicing, Foreclosure and Other Mortgage Matters

We service a large portion of the loans we or our subsidiaries have

securitized and also service loans on behalf of third-party

securitization vehicles and other investors. Our servicing

obligations are set forth in servicing agreements with the

applicable counterparty. These obligations may include, but are

not limited to, loan repurchase requirements in certain

circumstances, indemnifications, payment of fees, advances for

foreclosure costs that are not reimbursable, or responsibility for

losses in excess of partial guarantees for VA loans.

Servicing agreements with the GSEs generally provide the GSEs

with broader rights relative to the servicer than are found in

servicing agreements with private investors. For example, the

GSEs claim that they have the contractual right to demand

indemnification or loan repurchase for certain servicing breaches.

In addition, the GSEs’ first-lien mortgage seller/servicer guides

provide timelines to resolve delinquent loans through workout

efforts or liquidation, if necessary, and purport to require the

imposition of compensatory fees if those deadlines are not

satisfied except for reasons beyond the control of the servicer. In

addition, many non-agency RMBS and whole-loan servicing

agreements state that the servicer may be liable for failure to

perform its servicing obligations in keeping with industry standards

or for acts or omissions that involve willful malfeasance, bad faith

or gross negligence in the performance of, or reckless disregard

of, the servicer’s duties.

It is not possible to reasonably estimate our liability with

respect to certain potential servicing-related claims. While we have

recorded certain accruals for servicing-related claims, the amount

of potential liability in excess of existing accruals could be material

to the Corporation’s results of operations or cash flows for any

particular reporting period.

2013 IFR Acceleration Agreement

On January 7, 2013, we and other mortgage servicing institutions

entered into an agreement in principle with the Office of the

Comptroller of the Currency (OCC) and the Federal Reserve to

cease the Independent Foreclosure Review (IFR) that had

commenced pursuant to consent orders entered into by Bank of

America with the Federal Reserve (2011 FRB Consent Order) and

the 2011 OCC Consent Order entered into between BANA and the

OCC and replaced it with an accelerated remediation process

(2013 IFR Acceleration Agreement). The 2013 IFR Acceleration

Agreement requires us to provide $1.8 billion of borrower

assistance in the form of loan modifications and other foreclosure

prevention actions, and in addition, we made a cash payment of

$1.1 billion into a qualified settlement fund in 2013. The borrower

assistance program is not expected to result in any incremental

credit provision, as we believe that the existing allowance for credit

losses is adequate to absorb any costs that have not already been

recorded as charge-offs.