Bank of America 2014 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

96 Bank of America 2014

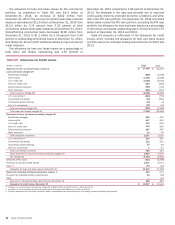

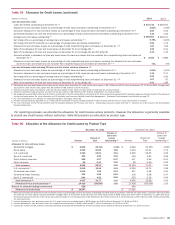

Reserve for Unfunded Lending Commitments

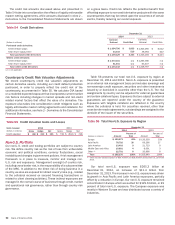

In addition to the allowance for loan and lease losses, we also

estimate probable losses related to unfunded lending

commitments such as letters of credit, financial guarantees,

unfunded bankers’ acceptances and binding loan commitments,

excluding commitments accounted for under the fair value option.

Unfunded lending commitments are subject to the same

assessment as funded loans, including estimates of probability

of default and LGD. Due to the nature of unfunded commitments,

the estimate of probable losses must also consider utilization. To

estimate the portion of these undrawn commitments that is likely

to be drawn by a borrower at the time of estimated default, analyses

of the Corporation’s historical experience are applied to the

unfunded commitments to estimate the funded EAD. The expected

loss for unfunded lending commitments is the product of the

probability of default, the LGD and the EAD, adjusted for any

qualitative factors including economic uncertainty and inherent

imprecision in models.

The reserve for unfunded lending commitments was $528

million at December 31, 2014, an increase of $44 million from

December 31, 2013. The increase was driven by increases in

expected loss.

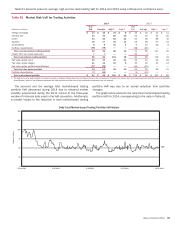

Market Risk Management

Market risk is the risk that values of assets and liabilities or

revenues will be adversely affected by changes in market

conditions. This risk is inherent in the financial instruments

associated with our operations, primarily within our Global Markets

segment. We are also exposed to these risks in other areas of the

Corporation (e.g., our ALM activities). In the event of market stress,

these risks could have a material impact on the results of the

Corporation. For additional information, see Interest Rate Risk

Management for Non-trading Activities on page 102.

Our traditional banking loan and deposit products are non-

trading positions and are generally reported at amortized cost for

assets or the amount owed for liabilities (historical cost). However,

these positions are still subject to changes in economic value

based on varying market conditions, with one of the primary risks

being changes in the levels of interest rates. The risk of adverse

changes in the economic value of our non-trading positions arising

from changes in interest rates is managed through our ALM

activities. We have elected to account for certain assets and

liabilities under the fair value option.

Our trading positions are reported at fair value with changes

reflected in income. Trading positions are subject to various

changes in market-based risk factors. The majority of this risk is

generated by our activities in the interest rate, foreign exchange,

credit, equity and commodities markets. In addition, the values of

assets and liabilities could change due to market liquidity,

correlations across markets and expectations of market volatility.

We seek to manage these risk exposures by using a variety of

techniques that encompass a broad range of financial

instruments. The key risk management techniques are discussed

in more detail in the Trading Risk Management section.

A subcommittee has been designated by the MRC as the

primary risk governance authority for Global Markets (Global

Markets, or GM subcommittee). The GM subcommittee’s focus is

to take a forward-looking view of the primary credit, market and

operational risks impacting Global Markets and prioritize those

that need a proactive risk mitigation strategy.

Global Markets Risk Management is responsible for providing

senior management with a clear and comprehensive

understanding of the trading risks to which the Corporation is

exposed. These responsibilities include ownership of market risk

policy, developing and maintaining quantitative risk models,

calculating aggregated risk measures, establishing and monitoring

position limits consistent with risk appetite, conducting daily

reviews and analysis of trading inventory, approving material risk

exposures and fulfilling regulatory requirements. Market risks that

impact businesses outside of Global Markets are monitored and

governed by their respective governance functions.

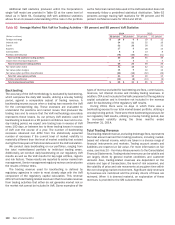

Quantitative risk models, such as VaR, are an essential

component in evaluating the market risks within a portfolio. A

subcommittee of the MRC is responsible for providing

management oversight and approval of model risk management

and governance (Risk Management, or RM subcommittee). The

RM subcommittee defines model risk standards, consistent with

the Corporation’s risk framework and risk appetite, prevailing

regulatory guidance and industry best practice. Models must meet

certain validation criteria, including effective challenge of the

model development process and a sufficient demonstration of

developmental evidence incorporating a comparison of alternative

theories and approaches. The RM subcommittee ensures model

standards are consistent with model risk requirements and

monitors the effective challenge in the model validation process

across the Corporation. In addition, the relevant stakeholders must

agree on any required actions or restrictions to the models and

maintain a stringent monitoring process to ensure continued

compliance.

For more information on the fair value of certain financial assets

and liabilities, see Note 20 – Fair Value Measurements to the

Consolidated Financial Statements.

Interest Rate Risk

Interest rate risk represents exposures to instruments whose

values vary with the level or volatility of interest rates. These

instruments include, but are not limited to, loans, debt securities,

certain trading-related assets and liabilities, deposits, borrowings

and derivatives. Hedging instruments used to mitigate these risks

include derivatives such as options, futures, forwards and swaps.

Foreign Exchange Risk

Foreign exchange risk represents exposures to changes in the

values of current holdings and future cash flows denominated in

currencies other than the U.S. Dollar. The types of instruments

exposed to this risk include investments in non-U.S. subsidiaries,

foreign currency-denominated loans and securities, future cash

flows in foreign currencies arising from foreign exchange

transactions, foreign currency-denominated debt and various

foreign exchange derivatives whose values fluctuate with changes

in the level or volatility of currency exchange rates or non-

U.S. interest rates. Hedging instruments used to mitigate this risk

include foreign exchange options, currency swaps, futures,

forwards, and foreign currency-denominated debt and deposits.

Mortgage Risk

Mortgage risk represents exposures to changes in the values of

mortgage-related instruments. The values of these instruments

are sensitive to prepayment rates, mortgage rates, agency debt

ratings, default, market liquidity, government participation and

interest rate volatility. Our exposure to these instruments takes