Bank of America 2014 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

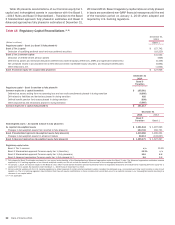

56 Bank of America 2014

Capital Management

The Corporation manages its capital position to maintain sufficient

capital to support its business activities and maintain capital, risk

and risk appetite commensurate with one another. Additionally, we

seek to maintain safety and soundness at all times even under

adverse scenarios, take advantage of organic growth

opportunities, maintain ready access to financial markets,

continue to serve as a credit intermediary, remain a source of

strength for our subsidiaries, and satisfy current and future

regulatory capital requirements. Capital management is integrated

into our risk and governance processes, as capital is a key

consideration in the development of our strategic plan, risk

appetite and risk limits.

We set goals for capital ratios to meet key stakeholder

expectations, including investors, regulators and rating agencies,

and to achieve our financial performance objectives and strategic

goals, while maintaining adequate capital, including during periods

of stress. We assess capital adequacy at least on a quarterly basis

to operate in a safe and sound manner and maintain adequate

capital in relation to the risks associated with our business

activities and strategy.

We conduct an Internal Capital Adequacy Assessment Process

(ICAAP) on a quarterly basis. The ICAAP is a forward-looking

assessment of our projected capital needs and resources,

incorporating earnings, balance sheet and risk forecasts under

baseline and adverse economic and market conditions. We utilize

quarterly stress tests to assess the potential impacts to our

balance sheet, earnings, regulatory capital and liquidity under a

variety of stress scenarios. We perform qualitative risk

assessments to identify and assess material risks not fully

captured in our forecasts or stress tests. We assess the capital

impacts of proposed changes to regulatory capital requirements.

Management assesses ICAAP results and provides documented

quarterly assessments of the adequacy of our capital guidelines

and capital position to the Board or its committees.

The Corporation periodically reviews capital allocated to its

businesses and allocates capital annually during the strategic and

capital planning processes. For more information, see Business

Segment Operations on page 31.

CCAR and Capital Planning

The Federal Reserve requires BHCs to submit a capital plan and

requests for capital actions on an annual basis, consistent with

the rules governing the Comprehensive Capital Analysis and

Review (CCAR) capital plan. The CCAR capital plan is the central

element of the Federal Reserve’s approach to ensure that large

BHCs have adequate capital and robust processes for managing

their capital.

On October 17, 2014, the Federal Reserve released 2015

CCAR instructions as well as an update to the capital plan and

stress test rules. The revised rules shift the dates of the annual

stress testing cycle by approximately three months to April,

beginning with 2016 CCAR capital plans.

In January 2015, we submitted our 2015 CCAR capital plan

and related supervisory stress tests. The Federal Reserve has

announced that it will release summary results, including

supervisory projections of capital ratios, losses and revenues

under stress scenarios, and publish the results of stress tests

conducted under the supervisory adverse and supervisory severely

adverse scenarios in March 2015.

In January 2014, we submitted our 2014 CCAR capital plan

and received results in March 2014. Based on the information in

our January 2014 submission, the Federal Reserve advised that

it did not object to our 2014 capital actions. In April 2014, we

announced the revision of certain regulatory capital amounts and

ratios that had previously been reported, and suspended our

previously announced 2014 capital actions stating that we would

resubmit information pursuant to the 2014 CCAR to the Federal

Reserve. In May 2014, we submitted our revised 2014 CCAR

capital plan, and in August 2014, the Federal Reserve informed

us that it did not object to our revised 2014 CCAR capital plan.

The requested capital actions included an increase in the quarterly

common stock dividend to $0.05 per share from $0.01 per share,

but no additional common stock repurchases.

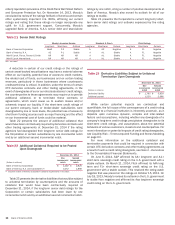

Regulatory Capital

As a financial services holding company, we are subject to

regulatory capital rules issued by U.S. banking regulators. On

January 1, 2014, we became subject to the Basel 3 rules, which

include certain transition provisions through January 1, 2019

(Basel 3 Standardized – Transition). Basel 3 generally continues

to be subject to interpretation and clarification by U.S. banking

regulators. Basel 3 also expands and modifies the risk-sensitive

calculation of risk-weighted assets (defined in the Basel 1 – 2013

Rules) for credit and market risk (applicable to banks that meet

the definition as advanced approaches); and introduces a

Standardized approach for the calculation of risk-weighted assets,

which serves as a minimum. The Corporation and its primary

affiliated banking entity, BANA, meet the definition of an advanced

approaches bank and measure regulatory capital adequacy based

on the Basel 3 rules. Through December 31, 2013, we were subject

to the Basel 1 general risk-based capital rules which included new

measures of market risk including a charge related to stressed

Value-at-Risk (VaR), an incremental risk charge and the

comprehensive risk measure (CRM), as well as other technical

modifications to Basel 1 (the Basel 1 – 2013 Rules).

The risk-sensitive approach for calculating risk-weighted assets

under Basel 3 replaces the approach under the Basel 1 – 2013

Rules. Risk-weighted assets are calculated for credit risk for all

on- and off-balance sheet credit exposures and for market risk on

trading assets and liabilities, including derivative exposures. Credit

risk-weighted assets are calculated by assigning a prescribed risk

weight to all on-balance sheet assets and to the credit equivalent

amount of certain off-balance sheet exposures. Off-balance sheet

exposures include financial guarantees, unfunded lending

commitments, letters of credit and derivatives. Market risk-

weighted assets are calculated using risk models for trading

account positions, including all foreign exchange and commodity

positions regardless of the applicable accounting guidance. Any

assets that are a direct deduction from the computation of capital

are excluded from risk-weighted assets and adjusted average total

assets, consistent with regulatory guidance.

For more information on the regulatory capital amounts and

calculations, see Basel 3 below.