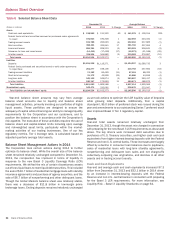

Bank of America 2014 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

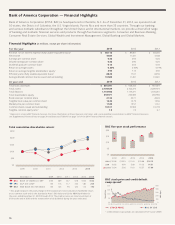

22 Bank of America 2014

Financial Highlights

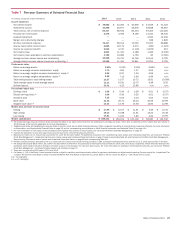

Net income was $4.8 billion, or $0.36 per diluted share in 2014

compared to $11.4 billion, or $0.90 per diluted share in 2013.

The results for 2014 included an increase of $10.3 billion in

litigation expense primarily as a result of charges related to the

settlements with the U.S. Department of Justice (DoJ) and the

Federal Housing Finance Agency (FHFA).

Table 2 Summary Income Statement

(Dollars in millions) 2014 2013

Net interest income (FTE basis) (1) $ 40,821 $ 43,124

Noninterest income 44,295 46,677

Total revenue, net of interest expense (FTE basis) (1) 85,116 89,801

Provision for credit losses 2,275 3,556

Noninterest expense 75,117 69,214

Income before income taxes (FTE basis) (1) 7,724 17,031

Income tax expense (FTE basis) (1) 2,891 5,600

Net income 4,833 11,431

Preferred stock dividends 1,044 1,349

Net income applicable to common shareholders $ 3,789 $ 10,082

Per common share information

Earnings $0.36

$0.94

Diluted earnings 0.36 0.90

(1) FTE basis is a non-GAAP financial measure. For more information on this measure, see

Supplemental Financial Data on page 29, and for a corresponding reconciliation to GAAP financial

measures, see Statistical Table XV.

Net Interest Income

Net interest income on a fully taxable-equivalent (FTE) basis

decreased $2.3 billion to $40.8 billion for 2014 compared to

2013. The net interest yield on an FTE basis decreased 12 basis

points (bps) to 2.25 percent for 2014. These declines were

primarily due to the acceleration of market-related premium

amortization on debt securities as the decline in long-term interest

rates shortened the expected lives of the securities. Also

contributing to these declines were lower loan yields and consumer

loan balances, lower net interest income from the asset and liability

management (ALM) portfolio and a decrease in trading-related net

interest income. Market-related premium amortization was an

expense of $1.2 billion in 2014 compared to a benefit of $784

million in 2013. Partially offsetting these declines were reductions

in funding yields, lower long-term debt balances and commercial

loan growth.

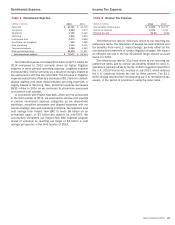

Noninterest Income

Table 3 Noninterest Income

(Dollars in millions) 2014 2013

Card income $ 5,944 $ 5,826

Service charges 7,443 7,390

Investment and brokerage services 13,284 12,282

Investment banking income 6,065 6,126

Equity investment income 1,130 2,901

Trading account profits 6,309 7,056

Mortgage banking income 1,563 3,874

Gains on sales of debt securities 1,354 1,271

Other income (loss) 1,203 (49)

Total noninterest income $ 44,295 $ 46,677

Noninterest income decreased $2.4 billion to $44.3 billion for

2014 compared to 2013. The following highlights the significant

changes.

Investment and brokerage services income increased $1.0

billion primarily driven by increased asset management fees

driven by the impact of long-term assets under management

(AUM) inflows and higher market levels.

Equity investment income decreased $1.8 billion to $1.1 billion

primarily due to a lower level of gains compared to 2013 and

the continued wind-down of Global Principal Investments (GPI).

Trading account profits decreased $747 million, which included

a charge of $497 million in 2014 related to the adoption of a

funding valuation adjustment (FVA) in Global Markets, partially

offset by a $359 million change in net debit valuation

adjustments (DVA) on derivatives. Excluding the FVA/DVA

charges, trading account profits decreased $609 million due to

both lower market volumes and volatility.

Mortgage banking income decreased $2.3 billion primarily

driven by lower servicing income and core production revenue,

partially offset by lower representations and warranties

provision.

Other income (loss) improved $1.3 billion due to an increase of

$1.1 billion in net DVA gains on structured liabilities as our

spreads widened, and gains associated with the sales of

residential mortgage loans, partially offset by increases in U.K.

consumer payment protection insurance (PPI) costs. The prior

year also included the write-down of $450 million on a monoline

receivable.

Provision for Credit Losses

The provision for credit losses decreased $1.3 billion to $2.3

billion for 2014 compared to 2013. The provision for credit losses

was $2.1 billion lower than net charge-offs for 2014, resulting in

a reduction in the allowance for credit losses. The decrease from

the prior year was driven by portfolio improvement, including

increased home prices in the home loans portfolio and lower

unemployment levels driving improvement in the credit card

portfolios, and improved asset quality in the commercial portfolio.

Partially offsetting this decline was $400 million of additional costs

in 2014 associated with the consumer relief portion of the

settlement with the DoJ. We expect reserve releases in 2015 to

moderate when compared to 2014.

Net charge-offs totaled $4.4 billion, or 0.49 percent of average

loans and leases for 2014 compared to $7.9 billion, or 0.87

percent for 2013. The decrease in net charge-offs was due to

credit quality improvement across all major portfolios and the

impact of increased recoveries primarily from nonperforming and

delinquent loan sales. For more information on the provision for

credit losses, see Provision for Credit Losses on page 92.