Bank of America 2014 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

66 Bank of America 2014

orderly liquidation provisions of the Dodd-Frank Wall Street Reform

and Consumer Protection Act. On November 14, 2013, Moody’s

concluded its review of the ratings for Bank of America and certain

other systemically important U.S. BHCs, affirming our current

ratings and noting that those ratings no longer incorporate any

uplift for U.S. government support. Concurrently, Moody’s

upgraded Bank of America, N.A.’s senior debt and stand-alone

ratings by one notch, citing a number of positive developments at

Bank of America. Moody’s also moved its outlook for all of our

ratings to stable.

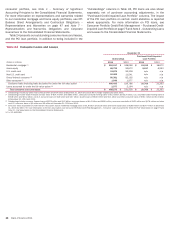

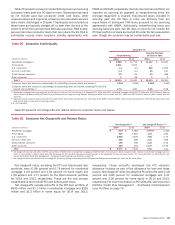

Table 21 presents the Corporation’s current long-term/short-

term senior debt ratings and outlooks expressed by the rating

agencies.

Table 21 Senior Debt Ratings

Moody’s Investors Service Standard & Poor’s Fitch Ratings

Long-term Short-term Outlook Long-term Short-term Outlook Long-term Short-term Outlook

Bank of America Corporation Baa2 P-2 Stable A- A-2 Negative A F1 Negative

Bank of America, N.A. A2 P-1 Stable A A-1 Stable A F1 Negative

Merrill Lynch, Pierce, Fenner & Smith NR NR NR A A-1 Stable A F1 Negative

Merrill Lynch International NR NR NR A A-1 Stable A F1 Negative

NR = not rated

A reduction in certain of our credit ratings or the ratings of

certain asset-backed securitizations may have a material adverse

effect on our liquidity, potential loss of access to credit markets,

the related cost of funds, our businesses and on certain trading

revenues, particularly in those businesses where counterparty

creditworthiness is critical. In addition, under the terms of certain

OTC derivative contracts and other trading agreements, in the

event of downgrades of our or our rated subsidiaries’ credit ratings,

the counterparties to those agreements may require us to provide

additional collateral, or to terminate these contracts or

agreements, which could cause us to sustain losses and/or

adversely impact our liquidity. If the short-term credit ratings of

our parent company, bank or broker-dealer subsidiaries were

downgraded by one or more levels, the potential loss of access to

short-term funding sources such as repo financing and the effect

on our incremental cost of funds could be material.

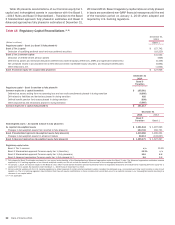

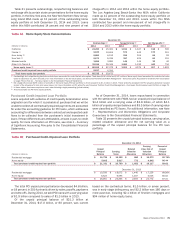

Table 22 presents the amount of additional collateral that

would have been contractually required by derivative contracts and

other trading agreements at December 31, 2014 if the rating

agencies had downgraded their long-term senior debt ratings for

the Corporation or certain subsidiaries by one incremental notch

and by an additional second incremental notch.

Table 22 Additional Collateral Required to be Posted

Upon Downgrade

December 31, 2014

(Dollars in millions)

One

incremental

notch

Second

incremental

notch

Bank of America Corporation $ 1,402 $ 2,825

Bank of America, N.A. and subsidiaries (1) 1,072 1,886

(1) Included in Bank of America Corporation collateral requirements in this table.

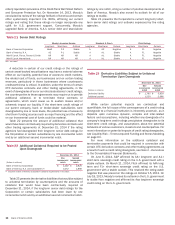

Table 23 presents the derivative liabilities that would be subject

to unilateral termination by counterparties and the amounts of

collateral that would have been contractually required at

December 31, 2014, if the long-term senior debt ratings for the

Corporation or certain subsidiaries had been lower by one

incremental notch and by an additional second incremental notch.

Table 23 Derivative Liabilities Subject to Unilateral

Termination Upon Downgrade

December 31, 2014

(Dollars in millions)

One

incremental

notch

Second

incremental

notch

Derivative liability $ 1,785 $ 3,850

Collateral posted 1,520 2,986

While certain potential impacts are contractual and

quantifiable, the full scope of the consequences of a credit rating

downgrade to a financial institution is inherently uncertain, as it

depends upon numerous dynamic, complex and inter-related

factors and assumptions, including whether any downgrade of a

company’s long-term credit ratings precipitates downgrades to its

short-term credit ratings, and assumptions about the potential

behaviors of various customers, investors and counterparties. For

more information on potential impacts of credit rating downgrades,

see Liquidity Risk – Time-to-required Funding and Stress Modeling

on page 63.

For more information on the additional collateral and

termination payments that could be required in connection with

certain OTC derivative contracts and other trading agreements as

a result of such a credit rating downgrade, see Note 2 – Derivatives

to the Consolidated Financial Statements.

On June 6, 2014, S&P affirmed its AA+ long-term and A-1+

short-term sovereign credit rating on the U.S. government with a

stable outlook. On March 21, 2014, Fitch affirmed its AAA long-

term and F1+ short-term sovereign credit rating on the U.S.

government with a stable outlook. This resolved the rating watch

negative that was placed on the ratings on October 15, 2013. On

July 18, 2013, Moody’s revised its outlook on the U.S. government

to stable from negative and affirmed its Aaa long-term sovereign

credit rating on the U.S. government.