Bank of America 2014 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 77

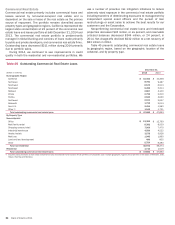

Purchased Credit-impaired Home Equity Loan Portfolio

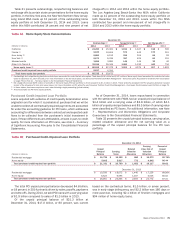

The PCI home equity portfolio represented 27 percent of the total

PCI loan portfolio at December 31, 2014. Those loans with a

refreshed FICO score below 620 represented 15 percent of the

PCI home equity portfolio at December 31, 2014. Loans with a

refreshed CLTV greater than 90 percent, after consideration of

purchase accounting adjustments and the related valuation

allowance, represented 64 percent of the PCI home equity portfolio

and 68 percent based on the unpaid principal balance at

December 31, 2014. Table 34 presents outstandings net of

purchase accounting adjustments and before the related valuation

allowance, by certain state concentrations.

Table 34 Outstanding Purchased Credit-impaired Loan

Portfolio – Home Equity State Concentrations

December 31

(Dollars in millions) 2014 2013

California $ 1,646 $ 1,921

Florida (1) 313 356

Virginia 265 310

Arizona 188 214

Colorado 151 199

Other U.S./Non-U.S. 3,054 3,593

Total $ 5,617 $ 6,593

(1) In this state, foreclosure requires a court order following a legal proceeding (judicial state).

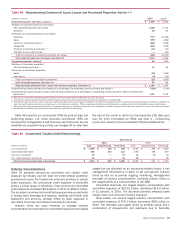

U.S. Credit Card

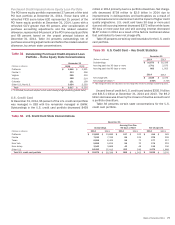

At December 31, 2014, 96 percent of the U.S. credit card portfolio

was managed in CBB with the remainder managed in GWIM.

Outstandings in the U.S. credit card portfolio decreased $459

million in 2014 primarily due to a portfolio divestiture. Net charge-

offs decreased $738 million to $2.6 billion in 2014 due to

improvements in delinquencies and bankruptcies as a result of

an improved economic environment and the impact of higher credit

quality originations. U.S. credit card loans 30 days or more past

due and still accruing interest decreased $372 million while loans

90 days or more past due and still accruing interest decreased

$187 million in 2014 as a result of the factors mentioned above

that contributed to lower net charge-offs.

Table 35 presents certain key credit statistics for the U.S. credit

card portfolio.

Table 35 U.S. Credit Card – Key Credit Statistics

December 31

(Dollars in millions) 2014 2013

Outstandings $ 91,879 $ 92,338

Accruing past due 30 days or more 1,701 2,073

Accruing past due 90 days or more 866 1,053

2014 2013

Net charge-offs $ 2,638 $ 3,376

Net charge-off ratios (1) 2.96% 3.74%

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans.

Unused lines of credit for U.S. credit card totaled $305.9 billion

and $315.1 billion at December 31, 2014 and 2013. The $9.2

billion decrease was driven by the closure of inactive accounts and

a portfolio divestiture.

Table 36 presents certain state concentrations for the U.S.

credit card portfolio.

Table 36 U.S. Credit Card State Concentrations

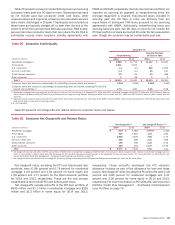

December 31

Outstandings

Accruing Past Due

90 Days or More Net Charge-offs

(Dollars in millions) 2014 2013 2014 2013 2014 2013

California $ 13,682 $ 13,689 $127 $ 162 $414 $ 562

Florida 7,530 7,339 89 105 278 359

Texas 6,586 6,405 58 72 177 217

New York 5,655 5,624 59 70 174 219

New Jersey 3,943 3,868 40 48 116 150

Other U.S. 54,483 55,413 493 596 1,479 1,869

Total U.S. credit card portfolio $ 91,879 $ 92,338 $866 $ 1,053 $ 2,638 $ 3,376