Bank of America 2014 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 61

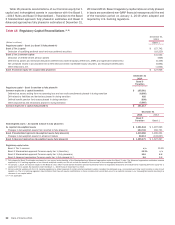

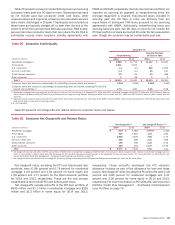

Bank of America, N.A. Regulatory Capital

Prior to October 1, 2014, we operated our banking activities

primarily under two charters: BANA and, to a lesser extent, FIA.

On October 1, 2014, FIA was merged into BANA. Table 17 presents

regulatory capital information for BANA at December 31, 2014 and

2013.

Table 17 Bank of America, N.A. Regulatory Capital

December 31

2014 2013

(Dollars in millions) Ratio Amount

Minimum

Required (1) Ratio Amount

Minimum

Required (1)

Common equity tier 1 capital (2) 13.1% $ 145,150 4.0% n/a n/a n/a

Tier 1 capital 13.1 145,150 6.0 12.3% $ 125,886 6.0%

Total capital 14.6 161,623 10.0 13.8 141,232 10.0

Tier 1 leverage 9.6 145,150 5.0 9.2 125,886 5.0

(1) Percent required to meet guidelines to be considered “well capitalized” under the Prompt Corrective Action framework, except for Common equity tier 1 capital which reflects capital adequacy minimum

requirements as an advanced approaches bank under Basel 3 during a transition period in 2014.

(2) When presented on a fully phased-in basis, beginning January 1, 2019, the minimum Basel 3 Common equity tier 1 capital ratio requirement for BANA is expected to significantly increase and will

be comprised of the minimum ratio of the then-applicable 4.5 percent, plus a capital conservation buffer and the GSIB buffer.

n/a = not applicable

BANA’s Tier 1 capital ratio under Basel 3 Standardized –

Transition was 13.1 percent at December 31, 2014, an increase

of 80 bps from December 31, 2013. The increase was largely

attributable to the merger of FIA into BANA in 2014. The Total

capital ratio increased 79 bps to 14.6 percent at December 31,

2014 compared to December 31, 2013. The Tier 1 leverage ratio

increased 42 bps to 9.6 percent. The increase in the Total capital

ratio was driven by the same factors as the Tier 1 capital ratio.

The increase in the Tier 1 leverage ratio was driven by an increase

in Tier 1 capital, partially offset by an increase in adjusted quarterly

average total assets. Further, the merger with FIA positively

impacted these ratios.

Other Regulatory Capital Matters

Supplementary Leverage Ratio

Basel 3 also will require the calculation of a supplementary

leverage ratio (SLR). The SLR is determined by dividing Tier 1

capital, using quarter-end Basel 3 Tier 1 capital on a fully phased-

in basis, by supplementary leverage exposure calculated as the

daily average of the sum of on-balance sheet as well as the simple

average of certain off-balance sheet exposures at the end of each

month in the quarter. Supplementary leverage exposure is

comprised of all on-balance sheet assets, plus a measure of

certain off-balance sheet exposures, including among other items,

lending commitments, letters of credit, OTC derivatives, repo-style

transactions and margin loan commitments. We are required to

disclose our SLR effective January 1, 2015. Effective January 1,

2018, the Corporation will be required to maintain a minimum SLR

of 3.0 percent, plus a supplementary leverage buffer of 2.0

percent, for a total SLR of 5.0 percent. If the Corporation’s

supplementary leverage buffer is not greater than or equal to 2.0

percent, then the Corporation will be subject to mandatory limits

on its ability to make distributions of capital to shareholders,

whether through dividends, stock repurchases or otherwise. In

addition, the insured depository institutions of such BHCs, which

for the Corporation is primarily BANA, will be required to maintain

a minimum 6.0 percent SLR to be considered “well capitalized.”

On September 3, 2014, U.S. banking regulators adopted a final

rule to revise the definition and scope of the denominator of the

SLR. The final rule prescribes the calculation of total leverage

exposure, the frequency of calculation and required disclosures.

The definition of total leverage exposure is revised to include the

effective notional principal amount of credit derivatives and other

similar instruments through which credit protection is sold.

Calculations of the components of total leverage exposure for

derivative and repo-style transactions are modified. The credit

conversion factors (CCF) applied to certain off-balance sheet

exposures are conformed to the graduated CCF used by the

Standardized approach, subject to the minimum 10 percent credit

conversion factor.

As of December 31, 2014, we estimate the Corporation’s SLR

would have been approximately 5.9 percent, which exceeds the

5.0 percent threshold that represents the minimum plus the

supplementary leverage buffer for BHCs. The estimated SLR for

BANA was approximately 7.0 percent, which exceeds the 6.0

percent “well capitalized” level for insured depository institutions

of BHCs.

Global Systemically Important Bank Surcharge

In November 2011, the Basel Committee on Banking Supervision

(Basel Committee) published a methodology to identify global

systemically important banks (GSIBs) and impose an additional

loss absorbency requirement through the introduction of a

surcharge of up to 3.5 percent, which must be satisfied with

Common equity tier 1 capital. The assessment methodology relies

on an indicator-based measurement approach to determine a

score relative to the global banking industry. The chosen indicators

are size, complexity, cross-jurisdictional activity, inter-

connectedness and substitutability/financial institution

infrastructure. Institutions with the highest scores are designated

as GSIBs and are assigned to one of four loss absorbency buckets

from 1.0 percent to 2.5 percent, in 0.5 percent increments based

on each institution’s relative score and supervisory judgment. The

fifth loss absorbency bucket of 3.5 percent is currently empty and

serves to discourage banks from becoming more systemically

important. Also in November 2011, the Financial Stability Board

(FSB) published an integrated set of policy measures and identified

an initial group of GSIBs, which included the Corporation.

In July 2013, the Basel Committee updated the November

2011 methodology to recalibrate the substitutability/financial

institution infrastructure indicator by introducing a cap on the

weighting of that component, and requiring the annual publication

by the FSB of key information necessary to permit each GSIB to

calculate its score and observe its position within the buckets and

relative to the industry total for each indicator. Every three years,