Bank of America 2014 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

52 Bank of America 2014

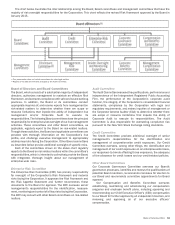

Managing Risk

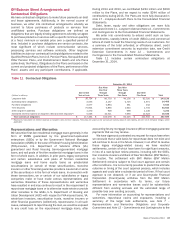

Overview

Risk is inherent in all our business activities. Sound risk

management enables us to serve our customers and deliver for

our shareholders. If not managed well, risks can result in financial

loss, regulatory sanctions and penalties, and damage to our

reputation, each of which may adversely impact our ability to

execute our business strategies. The seven types of risk faced by

Bank of America are strategic, credit, market, liquidity, compliance,

operational and reputational risks.

Strategic risk is the risk resulting from incorrect assumptions

about external or internal factors, inappropriate business plans,

ineffective business strategy execution, or failure to respond in a

timely manner to changes in the regulatory, macroeconomic or

competitive environments. Credit risk is the risk of loss arising

from the inability or failure of a borrower or counterparty to meet

its obligations. Market risk is the risk that changes in market

conditions may adversely impact the value of assets or liabilities,

or otherwise negatively impact earnings. Liquidity risk is the

potential inability to meet contractual or contingent financial

obligations, either on- or off-balance sheet, as they come due.

Compliance risk is the risk of legal or regulatory sanctions or

penalties arising from the failure of the Corporation to comply with

requirements of applicable laws, rules and regulations.

Operational risk is the risk of loss resulting from inadequate or

failed internal processes, people and systems, or from external

events. Reputational risk is the potential that negative perceptions

of the Corporation’s conduct or business practices may adversely

impact its profitability or operations through an inability to

establish new or maintain existing customer/client relationships.

Reputational risk is evaluated along with all of the risk categories

and throughout the risk management process and, as such, is not

discussed separately herein. The following sections, Strategic Risk

Management on page 55, Capital Management on page 56

Liquidity Risk on page 62, Credit Risk Management on page 67,

Market Risk Management on page 96, Compliance Risk

Management on page 105 and Operational Risk Management on

page 106, address in more detail the specific procedures,

measures and analyses of the major categories of risk. This

discussion of managing risk focuses on the Risk Framework that,

as part of its annual review process, was approved by the

Corporation’s Board of Directors (the Board) and its Enterprise

Risk Committee (ERC) in January 2015. The key enhancements

from the 2014 Risk Framework include further increasing the focus

on our strong risk culture and ensuring consistency with recent

regulatory guidance. It continues to recognize the same seven key

risk types as discussed above, and the five components of our

risk management approach as outlined below.

A strong risk culture is fundamental to our core values and

operating principles. It requires us to focus on risk in all activities

and encourages the necessary mindset and behavior to enable

effective risk management, and promotes sound risk taking within

our risk appetite. Sustaining a strong risk culture throughout the

organization is critical to the success of the Corporation and is a

clear expectation of our executive management team and the

Board.

Our Risk Framework is the foundation for comprehensive

management of the risks facing the Corporation. It outlines clear

responsibilities and accountabilities for managing risk. The Risk

Framework sets forth roles and responsibilities for the

management of risk by front line units (FLUs), independent risk

management, control functions and Corporate Audit, each of which

is described below in Managing Risk – Risk Management

Governance, and provides a blueprint for how the Board, through

delegation of authority to committees and executive officers,

establishes risk appetite and associated limits for our activities.

It describes the five components of our risk management approach

(risk culture, risk appetite, risk management processes, risk data

aggregation and reporting, and risk governance) and the seven key

types of risk we face.

Executive management assesses, with Board oversight, the

risk-adjusted returns of each business. Management reviews and

approves strategic and financial operating plans, and recommends

a financial plan annually to the Board for approval. Our strategic

plan takes into consideration return objectives and financial

resources, which must align with risk capacity and risk appetite.

Management sets financial objectives for each business by

allocating capital and setting a target for return on capital for each

business. Capital allocations and operating limits are regularly

evaluated as part of our overall governance processes as the

businesses and the economic environment in which we operate

continue to evolve. For more information regarding capital

allocations, see Business Segment Operations on page 31.

Our Risk Appetite Statement is intended to ensure that the

Corporation maintains an acceptable risk profile by providing a

common framework and a comparable set of measures for senior

management and the Board to clearly indicate the level of risk the

Corporation is willing to accept. The Risk Appetite Statement

includes both quantitative limits and qualitative components. Risk

appetite is set at least annually in conjunction with the strategic,

capital and financial operating plans to align risk appetite with the

Corporation’s strategy and financial resources. Line of business

strategies and risk appetite are also aligned. As part of its annual

review, the Board approved the Risk Appetite Statement in January

2015.

Our overall capacity to take risk is limited; therefore, we prioritize

the risks we take in order to maintain a strong and flexible financial

position so we can withstand challenging economic times and take

advantage of organic growth opportunities. Therefore, we set

objectives and targets for capital and liquidity that are intended

to permit the Corporation to continue to operate in a safe and

sound manner at all times, including during periods of stress.

Each of our lines of business operates within their credit, market

and operational risk appetite limits. These limits are based on

analyses of risk and reward within each line of business. Executive

management is responsible for tracking and reporting

performance measurements as well as any exceptions to

guidelines or limits. The Board, and its committees when

appropriate, oversees financial performance, execution of the

strategic and financial operating plans, adherence to risk appetite

limits and the adequacy of internal controls.

Risk Management Governance

The Risk Framework includes delegations of authority whereby the

Board and its committees may delegate authority to management-

level committees or executive officers. Such delegations may

authorize certain decision-making and approval functions, which

may be evidenced in, for example, committee charters, job

descriptions, meeting minutes and resolutions.