Bank of America 2014 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 73

The Community Reinvestment Act (CRA) encourages banks to

meet the credit needs of their communities for housing and other

purposes, particularly in neighborhoods with low or moderate

incomes. Our CRA portfolio was $9.0 billion and $10.3 billion at

December 31, 2014 and 2013, or seven percent of the residential

mortgage portfolio, at both December 31, 2014 and 2013. The

CRA portfolio included $986 million and $1.7 billion of

nonperforming loans at December 31, 2014 and 2013,

representing 14 percent of total nonperforming residential

mortgage loans, at both December 31, 2014 and 2013. Net

charge-offs in the CRA portfolio were $52 million compared to net

recoveries of $114 million for the residential mortgage portfolio

in 2014 and $260 million of the $1.1 billion total net charge-offs

for the residential mortgage portfolio in 2013.

Home Equity

At December 31, 2014, the home equity portfolio made up 18

percent of the consumer portfolio and is comprised of HELOCs,

home equity loans and reverse mortgages.

At December 31, 2014, our HELOC portfolio had an

outstanding balance of $74.2 billion, or 87 percent of the total

home equity portfolio compared to $80.3 billion, or 86 percent,

at December 31, 2013. HELOCs generally have an initial draw

period of 10 years. During the initial draw period, the borrowers

are only required to pay the interest due on the loans on a monthly

basis. After the initial draw period ends, the loans generally convert

to 15-year amortizing loans.

At December 31, 2014, our home equity loan portfolio had an

outstanding balance of $9.8 billion, or 11 percent of the total home

equity portfolio compared to $12.0 billion, or 13 percent, at

December 31, 2013. Home equity loans are almost all fixed-rate

loans with amortizing payment terms of 10 to 30 years and of the

$9.8 billion at December 31, 2014, 53 percent have 25- to 30-

year terms. At December 31, 2014, our reverse mortgage portfolio

had an outstanding balance, excluding loans accounted for under

the fair value option, of $1.7 billion, or two percent of the total

home equity portfolio compared to $1.4 billion, or one percent, at

December 31, 2013. We no longer originate reverse mortgages.

At December 31, 2014, approximately 90 percent of the home

equity portfolio was included in CRES while the remainder of the

portfolio was primarily in GWIM. Outstanding balances in the home

equity portfolio, excluding loans accounted for under the fair value

option, decreased $7.9 billion in 2014 primarily due to paydowns

and charge-offs outpacing new originations and draws on existing

lines. Of the total home equity portfolio at December 31, 2014

and 2013, $20.6 billion and $20.7 billion, or 24 percent and 22

percent, were in first-lien positions (26 percent and 24 percent

excluding the PCI home equity portfolio). At December 31, 2014,

outstanding balances in the home equity portfolio that were in a

second-lien or more junior-lien position and where we also held

the first-lien loan totaled $15.4 billion, or 19 percent of our total

home equity portfolio excluding the PCI loan portfolio.

Unused HELOCs totaled $53.7 billion and $56.8 billion at

December 31, 2014 and 2013. The decrease was primarily due

to customers choosing to close accounts, which more than offset

customer paydowns of principal balances, as well as the impact

of new production. The HELOC utilization rate was 58 percent and

59 percent at December 31, 2014 and 2013.

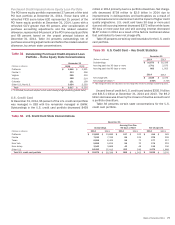

Table 30 presents certain home equity portfolio key credit

statistics on both a reported basis excluding loans accounted for

under the fair value option, and excluding the PCI loan portfolio

and loans accounted for under the fair value option. Additionally,

in the “Reported Basis” columns in the table below, accruing

balances past due 30 days or more and nonperforming loans do

not include the PCI loan portfolio, in accordance with our

accounting policies, even though the customer may be

contractually past due. As such, the following discussion presents

the home equity portfolio excluding the PCI loan portfolio and loans

accounted for under the fair value option. For more information on

the PCI loan portfolio, see page 75.

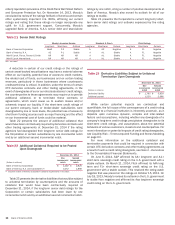

Table 30 Home Equity – Key Credit Statistics

December 31

Reported Basis (1)

Excluding Purchased

Credit-impaired Loans

(Dollars in millions) 2014 2013 2014 2013

Outstandings $ 85,725 $ 93,672 $80,108 $ 87,079

Accruing past due 30 days or more (2) 640 901 640 901

Nonperforming loans (2) 3,901 4,075 3,901 4,075

Percent of portfolio

Refreshed CLTV greater than 90 but less than or equal to 100 (3) 8% 9% 7% 8%

Refreshed CLTV greater than 100 (3) 16 23 14 21

Refreshed FICO below 620 8878

2006 and 2007 vintages (4) 46 48 43 45

Net charge-off ratio (5) 1.01 1.80 1.09 1.94

(1) Outstandings, accruing past due, nonperforming loans and percentages of the portfolio exclude loans accounted for under the fair value option. There were $196 million and $147 million of home

equity loans accounted for under the fair value option at December 31, 2014 and 2013. For more information on the fair value option, see Consumer Portfolio Credit Risk Management – Consumer

Loans Accounted for Under the Fair Value Option on page 79 and Note 21 – Fair Value Option to the Consolidated Financial Statements.

(2) Accruing past due 30 days or more includes $98 million and $131 million and nonperforming loans includes $505 million and $582 million of loans where we serviced the underlying first-lien at

December 31, 2014 and 2013.

(3) Effective December 31, 2014, with the exception of high-value properties, underlying values for LTV ratios are primarily determined using automated valuation models. For high-value properties,

generally with an original value of $1 million or more, estimated property values are determined using the CoreLogic Case-Shiller Index. Prior-period values have been updated to reflect this change.

Previously reported values were primarily determined through an index-based approach.

(4) These vintages of loans have higher refreshed combined LTV ratios and accounted for 47 percent and 50 percent of nonperforming home equity loans at December 31, 2014 and 2013, and 59

percent and 63 percent of net charge-offs in 2014 and 2013.

(5) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans excluding loans accounted for under the fair value option.