Bank of America 2014 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

112 Bank of America 2014

Noninterest Income

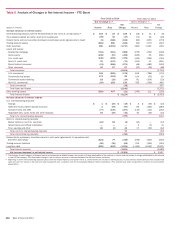

Noninterest income was $46.7 billion in 2013, an increase of $4.0

billion compared to 2012.

Card income decreased $295 million primarily driven by lower

revenue from consumer protection products.

Investment and brokerage services income increased $889

million primarily driven by the impact of long-term AUM inflows

and higher market levels.

Investment banking income increased $827 million primarily

due to strong equity issuance fees attributable to a significant

increase in global equity capital markets volume and higher debt

issuance fees, primarily within leveraged finance and

investment-grade underwriting.

Equity investment income increased $831 million. The results

for 2013 included $753 million of gains related to the sale of

our remaining investment in CCB and gains of $1.4 billion on

the sales of a portion of an equity investment. The results for

2012 included $1.6 billion of gains related to sales of certain

equity and strategic investments.

Trading account profits increased $1.2 billion. Net debit

valuation adjustment (DVA) losses on derivatives were $509

million in 2013 compared to losses of $2.5 billion in 2012.

Excluding net DVA, trading account profits decreased $782

million due to decreases in our FICC businesses driven by a

challenging trading environment, partially offset by an increase

in our equities businesses.

Mortgage banking income decreased $876 million primarily

driven by lower servicing income and lower core production

revenue, partially offset by lower representations and warranties

provision.

Other income (loss) improved $2.0 billion due to lower negative

fair value adjustments on our structured liabilities of $649

million compared to negative fair value adjustments of $5.1

billion in 2012. The prior year included gains of $1.6 billion

related to debt repurchases and exchanges of trust preferred

securities.

Provision for Credit Losses

The provision for credit losses was $3.6 billion for 2013, a

decrease of $4.6 billion compared to 2012. The provision for credit

losses was $4.3 billion lower than net charge-offs for 2013,

resulting in a reduction in the allowance for credit losses due to

continued improvement in the home loans and credit card

portfolios. This compared to a $6.7 billion reduction in the

allowance for credit losses in 2012.

Net charge-offs totaled $7.9 billion, or 0.87 percent of average

loans and leases for 2013 compared to $14.9 billion, or 1.67

percent for 2012. The decrease in net charge-offs was primarily

driven by credit quality improvement across all major portfolios.

Also, included in 2012 were charge-offs associated with the

National Mortgage Settlement and loans discharged in Chapter 7

bankruptcy due to the implementation of regulatory guidance.

Noninterest Expense

Noninterest expense was $69.2 billion for 2013, a decrease of

$2.9 billion compared to 2012. The decrease was primarily driven

by a $967 million decline in other general operating expense largely

due to a provision of $1.1 billion in 2012 for the 2013 Independent

Foreclosure Review (IFR) Acceleration Agreement, lower FDIC

expense, and lower default-related servicing expenses in Legacy

Assets & Servicing and mortgage-related assessments, waivers

and similar costs related to foreclosure delays. Partially offsetting

these declines was a $1.9 billion increase in litigation expense to

$6.1 billion in 2013. Personnel expense decreased $929 million

in 2013 as we continued to streamline processes and achieve

cost savings. Professional fees decreased $690 million due in

part to reduced default-related management activities in Legacy

Assets & Servicing.

Income Tax Expense

The income tax expense was $4.7 billion on pretax income of

$16.2 billion for 2013 compared to an income tax benefit of $1.1

billion on the pretax income of $3.1 billion for 2012. The effective

tax rate for 2013 was driven by our recurring tax preference items

and by tax benefits related to non-U.S. restructurings. These

benefits were partially offset by the $1.1 billion charge to reduce

the carrying value of certain U.K deferred tax assets due to the

U.K corporate income tax rate reduction in 2013. The negative

effective tax rate for 2012 included a $1.7 billion tax benefit

attributable to the excess of foreign tax credits recognized in the

U.S. upon repatriation of the earnings of certain subsidiaries over

the related U.S. tax liability. Partially offsetting the benefit was a

$788 million charge to reduce the carrying value of certain U.K.

deferred tax assets due to the U.K. corporate income tax rate

reduction enacted in 2012.

Business Segment Operations

Consumer & Business Banking

CBB recorded net income of $6.6 billion in 2013 compared to

$5.6 billion in 2012 with the increase primarily due to lower

provision for credit losses and noninterest expense. Net interest

income remained relatively unchanged as the impact of higher

deposit balances was offset by the impact of lower average loan

balances. Noninterest income of $9.8 billion remained relatively

unchanged as the allocation of certain card revenue to GWIM for

clients with a credit card, and lower deposit service charges were

offset by the net impact of consumer protection products primarily

due to changes in 2012. The provision for credit losses decreased

$1.0 billion to $3.1 billion in 2013 primarily as a result of

improvements in credit quality. Noninterest expense decreased

$661 million to $16.3 billion primarily due to lower operating,

personnel and FDIC expenses.