Bank of America 2014 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

92 Bank of America 2014

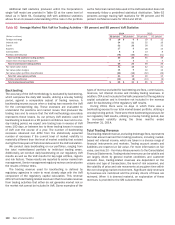

in these countries. Net exposure at December 31, 2014 to Italy

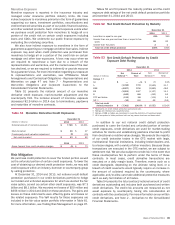

and Spain was $5.4 billion and $3.6 billion as presented in Table

57. For the remaining three countries noted above, net exposure

at December 31, 2014 was $2.1 billion which primarily relates to

Ireland. We expect to continue to support client activities in the

region and our exposures may vary over time as we monitor the

situation and manage our risk profile.

Table 58 presents countries where total cross-border exposure

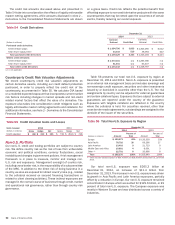

exceeded one percent of our total assets. At December 31, 2014,

the United Kingdom and France were the only countries where total

cross-border exposure exceeded one percent of our total assets.

At December 31, 2014, Germany had total cross-border exposure

of $15.9 billion representing 0.76 percent of our total assets. No

other countries had total cross-border exposure that exceeded

0.75 percent of our total assets at December 31, 2014.

Cross-border exposures in Table 58 are calculated using Federal

Financial Institutions Examination Council (FFIEC) guidelines and

not our internal risk management view; therefore, exposures are

not comparable between Tables 57 and 58. Exposure includes

cross-border claims by our non-U.S. offices including loans,

acceptances, time deposits placed, trading account assets,

securities, derivative assets, other interest-earning investments

and other monetary assets. Amounts also include unfunded

commitments, letters of credit and financial guarantees, and the

notional amount of cash loaned under secured financing

transactions. Sector definitions are consistent with FFIEC reporting

requirements for preparing the Country Exposure Report.

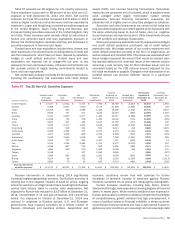

Table 58 Total Cross-border Exposure Exceeding One Percent of Total Assets

(Dollars in millions) December 31 Public Sector Banks Private Sector

Cross-border

Exposure

Exposure as a

Percent of

Total Assets

United Kingdom 2014 $ 11 $ 2,056 $ 34,595 $ 36,662 1.74%

2013 6 7,027 32,466 39,499 1.88

France (1) 2014 4,479 2,631 14,368 21,478 1.02

(1) At December 31, 2013, total cross-border exposure for France was $17.8 billion, representing 0.85 percent of total assets.

Provision for Credit Losses

The provision for credit losses decreased $1.3 billion to $2.3

billion in 2014 compared to 2013. The provision for credit losses

was $2.1 billion lower than net charge-offs for 2014, resulting in

a reduction in the allowance for credit losses. This compared to

a reduction of $4.3 billion in the allowance for credit losses for

2013. We expect reserve releases in 2015 to moderate when

compared to 2014.

The provision for credit losses for the consumer portfolio

decreased $533 million to $1.5 billion in 2014 compared to 2013.

The decrease was primarily due to continued improvement in the

home loans portfolios as a result of increased home prices,

improved delinquencies and continued loan balance run-off, as

well as improvement in the credit card portfolios primarily driven

by lower unemployment levels. These were partially offset by a

lower provision benefit related to the PCI loan portfolio of $31

million in 2014 compared to a benefit of $707 million in 2013.

Also offsetting the improvement was $400 million of additional

costs associated with the consumer relief portion of the DoJ

Settlement. For more information on the DoJ Settlement, see Off-

Balance Sheet Arrangements and Contractual Obligations –

Servicing, Foreclosure and Other Mortgage Matters on page 50.

The provision for credit losses for the commercial portfolio,

including unfunded lending commitments, decreased $748 million

to $793 million in 2014 compared to 2013 driven by improved

asset quality in 2014.

Allowance for Credit Losses

Allowance for Loan and Lease Losses

The allowance for loan and lease losses is comprised of two

components. The first component covers nonperforming

commercial loans and TDRs. The second component covers loans

and leases on which there are incurred losses that are not yet

individually identifiable, as well as incurred losses that may not

be represented in the loss forecast models. We evaluate the

adequacy of the allowance for loan and lease losses based on the

total of these two components, each of which is described in more

detail below. The allowance for loan and lease losses excludes

LHFS and loans accounted for under the fair value option as the

fair value reflects a credit risk component.

The first component of the allowance for loan and lease losses

covers both nonperforming commercial loans and all TDRs within

the consumer and commercial portfolios. These loans are subject

to impairment measurement based on the present value of

projected future cash flows discounted at the loan’s original

effective interest rate, or in certain circumstances, impairment

may also be based upon the collateral value or the loan’s

observable market price if available. Impairment measurement for

the renegotiated consumer credit card, small business credit card

and unsecured consumer TDR portfolios is based on the present

value of projected cash flows discounted using the average

portfolio contractual interest rate, excluding promotionally priced

loans, in effect prior to restructuring. For purposes of computing

this specific loss component of the allowance, larger impaired

loans are evaluated individually and smaller impaired loans are

evaluated as a pool using historical experience for the respective

product types and risk ratings of the loans.