Bank of America 2014 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

62 Bank of America 2014

beginning on January 1, 2016, the Basel Committee will reconsider

and recalibrate the bucket thresholds. The Basel Committee and

FSB expect banks to change their behavior in response to the

incentives of the GSIB framework, as well as other aspects of

Basel 3 and jurisdiction-specific regulations.

In November 2014, the Basel Committee published an updated

list of GSIBs and their respective loss absorbency buckets. As of

December 31, 2014, we estimated our surcharge at 1.5 percent

based on the Basel 3 information and considering the FSB’s report,

“2014 update of list of global systemically important banks

(GSIBs).” Our surcharge could change each year based on our

actions and those of our peers, as the scoring methods utilize

data from the Corporation in combination with the industry. If our

score were to increase, we could be subject to a higher GSIB

surcharge.

In December 2014, a U.S. banking regulator proposed a

regulation that would implement GSIB surcharge requirements for

the largest U.S. BHCs. Under the proposal, assignment to loss

absorbency buckets would be determined by the higher score as

calculated according to two methods. Method 1 is substantially

similar to the Basel Committee’s methodology, whereas Method

2 replaces the substitutability/financial institution infrastructure

indicator with a measure of short-term wholesale funding and then

multiplies the overall score by two. The Federal Reserve estimates

that Method 2 will yield a higher surcharge, currently ranging from

1.0 percent to 4.5 percent.

Under the proposed U.S. rules, the GSIB surcharge requirement

will begin to phase in effective January 2016, with full

implementation in January 2019. Data from the original five

indicators, measured as of December 31, 2014, combined with

short-term wholesale funding data covering the third quarter of

2015, is proposed to be used to determine the GSIB surcharge

that will be effective for us in 2016.

Broker-dealer Regulatory Capital and Securities

Regulation

The Corporation’s principal U.S. broker-dealer subsidiaries are

Merrill Lynch, Pierce, Fenner & Smith (MLPF&S) and Merrill Lynch

Professional Clearing Corp (MLPCC). MLPCC is a fully-guaranteed

subsidiary of MLPF&S and provides clearing and settlement

services. Both entities are subject to the net capital requirements

of SEC Rule 15c3-1. Both entities are also registered as futures

commission merchants and are subject to the Commodity Futures

Trading Commission Regulation 1.17.

MLPF&S has elected to compute the minimum capital

requirement in accordance with the Alternative Net Capital

Requirement as permitted by SEC Rule 15c3-1. At December 31,

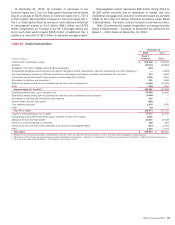

2014, MLPF&S’s regulatory net capital as defined by Rule 15c3-1

was $9.7 billion and exceeded the minimum requirement of $1.3

billion by $8.4 billion. MLPCC’s net capital of $3.4 billion exceeded

the minimum requirement of $508 million by $2.9 billion.

In accordance with the Alternative Net Capital Requirements,

MLPF&S is required to maintain tentative net capital in excess of

$1.0 billion, net capital in excess of $500 million and notify the

SEC in the event its tentative net capital is less than $5.0 billion.

At December 31, 2014, MLPF&S had tentative net capital and net

capital in excess of the minimum and notification requirements.

Merrill Lynch International (MLI), a U.K. investment firm, is

regulated by the Prudential Regulation Authority and the Financial

Conduct Authority, and is subject to certain regulatory capital

requirements. At December 31, 2014, MLI’s capital resources

were $32.3 billion which exceeded the minimum requirement of

$17.9 billion.

Common Stock Dividends

For a summary of our declared quarterly cash dividends on

common stock during 2014 and through February 25, 2015, see

Note 13 – Shareholders’ Equity to the Consolidated Financial

Statements.

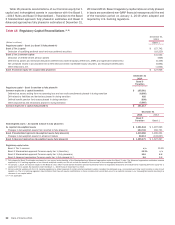

Liquidity Risk

Funding and Liquidity Risk Management

We define liquidity risk as the potential inability to meet our

contractual and contingent financial obligations, on- or off-balance

sheet, as they come due. Our primary liquidity objective is to

provide adequate funding for our businesses throughout market

cycles, including periods of financial stress. To achieve that

objective, we analyze and monitor our liquidity risk, maintain excess

liquidity and access diverse funding sources including our stable

deposit base. We define excess liquidity as readily available

assets, limited to cash and high-quality, liquid, unencumbered

securities that we can use to meet our funding requirements as

those obligations arise.

Global funding and primary liquidity risk management activities

are centralized within Corporate Treasury. We believe that a

centralized approach to funding and liquidity risk management

enhances our ability to monitor liquidity requirements, maximizes

access to funding sources, minimizes borrowing costs and

facilitates timely responses to liquidity events.

The Board approves the Corporation’s liquidity policy and the

ERC approves the contingency funding plan, including establishing

liquidity risk tolerance levels. The MRC monitors our liquidity

position and reviews the impact of strategic decisions on our

liquidity. The MRC is responsible for overseeing liquidity risks and

maintaining exposures within the established tolerance levels.

MRC reviews and monitors our liquidity position, cash flow

forecasts, stress testing scenarios and results, and implements

our liquidity limits and guidelines. For additional information, see

Managing Risk on page 52. Under this governance framework, we

have developed certain funding and liquidity risk management

practices which include: maintaining excess liquidity at the parent

company and selected subsidiaries, including our bank

subsidiaries and other regulated entities; determining what

amounts of excess liquidity are appropriate for these entities

based on analysis of debt maturities and other potential cash

outflows, including those that we may experience during stressed

market conditions; diversifying funding sources, considering our

asset profile and legal entity structure; and performing contingency

planning.

Global Excess Liquidity Sources and Other

Unencumbered Assets

We maintain excess liquidity available to Bank of America

Corporation, or the parent company and selected subsidiaries in

the form of cash and high-quality, liquid, unencumbered securities.

These assets, which we call our Global Excess Liquidity Sources,

serve as our primary means of liquidity risk mitigation. Our cash

is primarily on deposit with the Federal Reserve and, to a lesser

extent, central banks outside of the U.S. We limit the composition

of high-quality, liquid, unencumbered securities to U.S. government

securities, U.S. agency securities, U.S. agency MBS and a select