Bank of America 2014 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

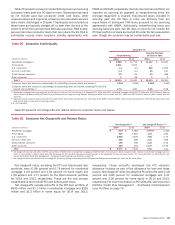

72 Bank of America 2014

Net charge-offs decreased $1.2 billion to a net recovery of

$114 million in 2014, or (0.08) percent of total average residential

mortgage loans, compared to net charge-offs of $1.1 billion, or

0.74 percent, in 2013. This decrease in net charge-offs was

primarily driven by favorable portfolio trends and decreased write-

downs on loans greater than 180 days past due, which were written

down to the estimated fair value of the collateral, less costs to

sell, due in part to improvement in home prices and the U.S.

economy. In addition, net charge-offs declined due to the impact

of recoveries of $407 million related to nonperforming loan sales

in 2014.

Residential mortgage loans with a greater than 90 percent but

less than or equal to 100 percent refreshed loan-to-value (LTV)

represented six percent and eight percent of the residential

mortgage portfolio at December 31, 2014 and 2013. Loans with

a refreshed LTV greater than 100 percent represented seven

percent and 11 percent of the residential mortgage loan portfolio

at December 31, 2014 and 2013. Of the loans with a refreshed

LTV greater than 100 percent, 96 percent and 95 percent were

performing at December 31, 2014 and 2013. Loans with a

refreshed LTV greater than 100 percent reflect loans where the

outstanding carrying value of the loan is greater than the most

recent valuation of the property securing the loan. The majority of

these loans have a refreshed LTV greater than 100 percent

primarily due to home price deterioration since 2006, somewhat

mitigated by subsequent appreciation. Loans to borrowers with

refreshed FICO scores below 620 represented eight percent and

11 percent of the residential mortgage portfolio at December 31,

2014 and 2013.

Of the $136.1 billion in total residential mortgage loans

outstanding at December 31, 2014, as shown in Table 29, 39

percent were originated as interest-only loans. The outstanding

balance of interest-only residential mortgage loans that have

entered the amortization period was $12.5 billion, or 23 percent

at December 31, 2014. Residential mortgage loans that have

entered the amortization period generally have experienced a

higher rate of early stage delinquencies and nonperforming status

compared to the residential mortgage portfolio as a whole. At

December 31, 2014, $256 million, or two percent of outstanding

interest-only residential mortgages that had entered the

amortization period were accruing past due 30 days or more

compared to $1.9 billion, or one percent for the entire residential

mortgage portfolio. In addition, at December 31, 2014, $862

million, or seven percent of outstanding interest-only residential

mortgages that had entered the amortization period were

nonperforming, of which $441 million were contractually current,

compared to $6.9 billion, or five percent for the entire residential

mortgage portfolio, of which $1.8 billion were contractually current.

Loans in our interest-only residential mortgage portfolio have an

interest-only period of three to ten years and more than 90 percent

of these loans that have yet to enter the amortization period will

not be required to make a fully-amortizing payment until 2016 or

later.

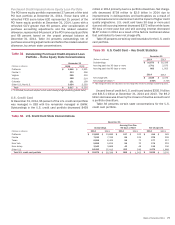

Table 29 presents outstandings, nonperforming loans and net

charge-offs by certain state concentrations for the residential

mortgage portfolio. The Los Angeles-Long Beach-Santa Ana

Metropolitan Statistical Area (MSA) within California represented

13 percent of outstandings at both December 31, 2014 and 2013.

In 2014, loans within this MSA contributed net recoveries of $81

million within the residential mortgage portfolio. In 2013, loans

within this MSA contributed three percent of net charge-offs within

the residential mortgage portfolio. In the New York area, the New

York-Northern New Jersey-Long Island MSA made up 11 percent

and 10 percent of outstandings at December 31, 2014 and 2013.

In 2014, loans within this MSA contributed net charge-offs of $27

million within the residential mortgage portfolio. In 2013, loans

within this MSA contributed 11 percent of net charge-offs within

the residential mortgage portfolio.

Table 29 Residential Mortgage State Concentrations

December 31

Outstandings (1) Nonperforming (1) Net Charge-offs (2)

(Dollars in millions) 2014 2013 2014 2013 2014 2013

California $ 45,496 $ 47,885 $ 1,459 $ 3,396 $(280)$ 148

New York (3) 11,826 11,787 477 789 15 59

Florida (3) 10,116 10,777 858 1,359 (43) 117

Texas 6,635 6,766 269 407 125

Virginia 4,402 4,774 244 369 431

Other U.S./Non-U.S. 57,600 60,158 3,582 5,392 189 704

Residential mortgage loans (4) $ 136,075 $142,147 $ 6,889 $ 11,712 $(114)$ 1,084

Fully-insured loan portfolio 64,970 87,247

Purchased credit-impaired residential mortgage loan portfolio 15,152 18,672

Total residential mortgage loan portfolio $ 216,197 $248,066

(1) Outstandings and nonperforming amounts exclude loans accounted for under the fair value option. There were $1.9 billion and $2.0 billion of residential mortgage loans accounted for under the fair

value option at December 31, 2014 and 2013. For more information on the fair value option, see Consumer Portfolio Credit Risk Management – Consumer Loans Accounted for Under the Fair Value

Option on page 79 and Note 21 – Fair Value Option to the Consolidated Financial Statements.

(2) Net charge-offs exclude $545 million of write-offs in the residential mortgage PCI loan portfolio in 2014 compared to $1.1 billion in 2013. These write-offs decreased the PCI valuation allowance

included as part of the allowance for loan and lease losses. For more information on PCI write-offs, see Consumer Portfolio Credit Risk Management – Purchased Credit-impaired Loan Portfolio on

page 75.

(3) In these states, foreclosure requires a court order following a legal proceeding (judicial states).

(4) Amount excludes the PCI residential mortgage and fully-insured loan portfolios.